By Marty Hartigan, Steve Shepley, Alan Brady – Deloitte

Learnings from the last decade of M&A activity within the Aerospace & Defense (A&D) industry offer three keys to consider for future effectiveness:

- Manage the demands of integration by limiting your total number of acquisitions.

- Make M&A central to your company’s growth strategy by implementing meaningful acquisitions.

- Target companies whose business models enhance your company’s market power.

Aerospace and defense (A&D) industry executives take note:

The next Merger & Acquisition (M&A) boom has begun; companies that identify the right acquisition targets and capture their full strategic value might be positioned for future competitive advantage.

Introduction: The A&D M&A boom

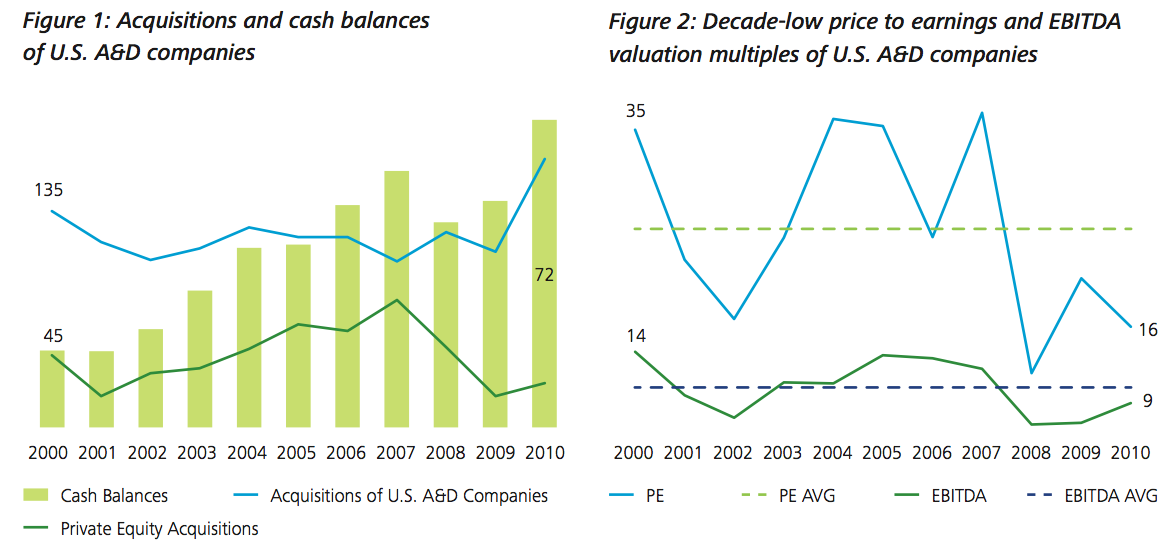

A variety of factors — including both macroeconomic indicators and the industry’s historical development — suggest that the recent uptick in M&A activity is the beginning of a boom for the industry. Three macroeconomic factors indicate that further consolidation might be imminent: pent-up demand, available capital (especially in the form of large cash balances), and valuations at historic lows. A&D is similar to other industries in that both strategic and financial buyers have cash to spend. Figure 1 illustrates the industry’s cash buildup and acquisition activity over the last 10 years.

This figure illustrates two important macroeconomic factors:

Pent-up demand

The A&D industry has traditionally seen dramatic increases in M&A activity following periods of decline, such as 2007–2008. 2010 saw the beginnings of an uptick in M&A activity, even with many acquirers (particularly private equity firms) sitting on the sidelines due to economic uncertainty.

Available capital

As a response to the general economic uncertainty, many A&D companies have been stockpiling cash. Current total cash balances of the United States’ (U.S.) A&D companies exceed an estimated $70 billion, one of the highest levels in the past decade, suggesting that there is capital available to deploy in acquisitions.

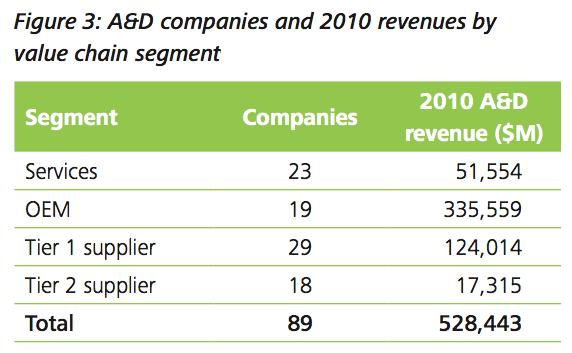

With strong demand and liquidity, one other structural ingredient that could lead to boom in M&A activity is favorable valuations. As Figure 2 shows, whether measured by price to earnings or EBITDA multiples, valuations of A&D firms appear to be at historic lows.

Further consolidation may be on the horizon, but Deloitte anticipates that the next several years’ consolidation will look different than in the past. The era of mega-mergers of large defense contractors is likely behind us, in part due to increased U.S. and European Union (EU) antitrust scrutiny. However, there remain hundreds of suppliers to these large defense contractors that could gain scale and cost efficiencies by merging.

The A&D industry’s available capital could allow for acquisitions of companies that possess “new reality” technologies, such as cyber security, precision engagement, data fusion, etc., to help grow revenue and increase operational scale to capture cost efficiencies. In this next cycle, we may see private equity competing for many of the same assets as strategic buyers after largely staying on the sidelines for the past few years.

The industry also may see additional consolidation in several specific supplier segments, including aero-structures, electronic components, engine components, electrical power supply, systems monitoring, etc., where the markets are crowded and increasingly commoditized. Finally, service providers focused not only on the “new reality” areas mentioned above but also logistical and energy-related services are expected to be particularly active.

Ultimately, it seems that the applicable question is when the boom in M&A activity will hit top speed. Time may be running out for some industry leaders to prepare their companies to take full advantage of potential opportunities.

Fact set: A&D M&A history and financial performance

In April 2011, Deloitte launched a study of the relationship between A&D companies’ M&A strategy and their financial performance, specifically shareholder return. We sought to identify the characteristics of M&A strategy that some high-performing companies shared but that low-performing companies lacked. Although effectiveness in M&A is one of several factors that can drive shareholder return — along with major program or new business wins, program backlog and affordability, growth in new markets, improved sourcing and management of working capital, engineering effectiveness, and many others — our findings show a clear correlation between the two.

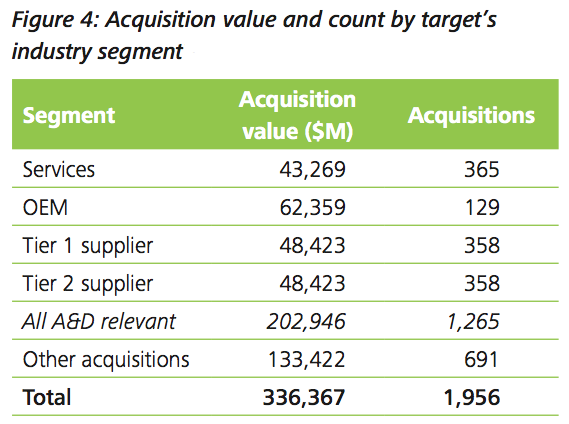

To address this topic, we analyzed A&D M&A transactions. Specifically, we, collected details of each merger or acquisition made by major public A&D companies; for example, each transaction’s closing date, value (where disclosed), and the industry segments of both targets and acquirers. We collected 10 years of this detailed M&A history (a total of 1,955 transactions), plus the financial results and shareholder returns of 89 public A&D companies across the globe. Figure 3 shows how these companies and their revenues break down across the A&D value chain segments.

Across the industry as a whole, there has been a great deal of M&A activity in the past 10 years. Eighty-four of the 89 companies made at least one acquisition over the period. Collectively, these 89 companies made 1,955 acquisitions for a combined value of $336 billion.9 Removing acquisitions made by A&D companies outside the industry leaves 1,265 acquisitions, at a total value of $203 billion. Figure 4 illustrates how the number and value of these acquisitions is distributed across the target’s industry segment.

To measure acquirers’ relative economic performance, we compared total shareholder returns (TSR) to sector returns. Our analysis showed that, over the last decade, A&D companies significantly outperformed the broader market due to strong defense spending, new products and upgrades, and international growth, among other factors. As a result, the sector generated a TSR of 7.4 percent, compared to 0.9 percent for the S&P 500. Using a sector index as the benchmark allows us to measure the relative performance of the 89 public A&D companies, which generally face the same general market conditions and challenges. Based on this comparison, companies fall into one of two categories: those that out-performed the sector benchmark and those that under-performed.

Findings: Three keys to M&A effectiveness

The Deloitte study explored whether a company’s level of acquisitiveness influences its likelihood of outperforming the sector. We categorized companies as either acquisitive or non-acquisitive based on both the number and financial scale of their acquisitions. Our analysis showed that, whether companies were acquisitive or not, they have virtually the same likelihood of outperforming the sector index: 66 percent of acquisitive companies outperformed it, as compared to 68 percent of non-acquisitive companies. Also, the geography of the acquirer or target did not have a significant effect on economic performance, despite the prevalence of cross-border deals in recent years. However, the way that companies executed their M&A strategy did correlate with meaningfully different rates of effectiveness.

Based on our analysis and our experience with clients, we identified three characteristics that companies which outperformed the sector generally shared and that underperformers did not. First, they managed the risk and strain of integration by limiting their total number of acquisitions. Second, they made M&A a core part of their growth strategy — and demonstrated its importance by making meaningful acquisitions. Third, they were disciplined about buying entities whose business models they could leverage to increase their market power. The remainder of this paper explores these characteristics in detail.

1. Most top-performing companies manage the demands of integration by limiting acquisitions.

Typically, there are a handful of reasons A&D companies buy one another. In our experience, the most common reasons include acquiring a product or proprietary technology, gaining access to new customers and markets, acquiring new manufacturing capabilities, rationalizing production capacity, or diversifying into new business models such as aftermarket services. Yet, selecting an appropriate target is just the first of many steps needed to capture the full value of an acquisition.

Research into M&A transactions across industries has found that the most transactions (as high as 70 percent) fail to create value. One possible reason is that companies often do not aggressively prepare and implement post-merger integration plans. Even for A&D companies that are experienced acquirers, post-merger integrations are difficult and often incomplete. Beyond the integration challenges all acquirers face, A&D firms typically face several additional challenges:

Concern that overhead harmonization hurts competitiveness

Acquired targets are often operated as a standalone business, even though the original intent was to integrate them to avoid combining overhead pools of the acquirer and target. This issue is most pronounced when a smaller target is burdened with an acquirer’s high overhead rates.

Belief that the target’s intrinsic value is sensitive to integration activities

- Acquirers may be concerned that a target’s value is dependent on a few key pockets of talent (often in engineering), leading acquirers to abandon plans to rationalize headcount, sites, and facilities if those plans are unpopular with key target team members.

- A long history of cost-plus contracting has created a culture where acquirers are typically averse to the aggressive cost-cutting that is a part of integration activities; moreover, even management teams that are willing to cut costs may lack the level of visibility required for pinpoint cuts.

Lack of post-merger integration specialization

- A&D companies rarely have dedicated departments with trained, experienced staff needed to handle complex integration activities or make hard decisions.

- Integration teams are often part-time or ad hoc and may not have bandwidth to execute all the critical integration activities alongside their primary roles.

- When performed, integrations tend to focus on ticking-off organizational “lines and boxes” rather than defining integration initiatives, setting synergy targets, and aggressively managing to those targets.

Deloitte’s data show that high acquisition counts can lead to poor financial performance. Again, the 89 companies in our sample collectively executed 1,956 acquisitions in A&D and other markets — an average of nearly 22 each. Some companies in the sample exceeded that average dramatically, making as many as 87 acquisitions. If the thought of negotiating, closing, and integrating half a dozen acquisitions each year sounds dizzying, it is for good reason. Over the past decade, the financially effective A&D companies were those that made fewer acquisitions. Moderately acquisitive companies (those that made 20 or fewer acquisitions — or roughly two acquisitions per year) were significantly more likely to outperform the sector than more acquisitive companies. Figure 5 shows how financial performance tends to diminish as companies become more and more acquisitive.

As the number of acquisitions rises, the acquirers’ sector outperformance rate falls. The sector outperformance rate was 75 percent for those companies that made fewer than 20 acquisitions but that figure falls as companies make more acquisitions. For companies that made 21-40 acquisitions, the success rate falls to 58 percent; above 41 acquisitions it plummets to 40 percent.

While high acquisition counts can be problematic for A&D companies, many of their peers in other industries have created acquisition models built for volume, particularly in the technology and pharmaceutical industries. Cisco, the network equipment manufacturer, is an example of a mass integrator: within 15 years Cisco has effectively integrated 160 acquisitions. Cisco achieved that effectiveness through a combination of tactical and strategic efforts. Tactically, Cisco has established repeatable integration processes and set an aggressive 100-day goal for full integration of a target’s technology and commercial functions.

Strategically, Cisco has clearly articulated M&A’s role in its growth strategy as a time-to-market accelerator and new product idea-generator. The combination of a well-tuned, repeatable process and clear strategic intent allows Cisco to pursue M&A opportunities without outstripping its ability to execute.

As technology replaces product at the heart of A&D acquisitions, industry executives will be challenged to develop similar repeatable processes designed to accelerate integrations and improve their chances of effectiveness.

2. Most top-performing companies make M&A central to their growth strategy.

As Cisco’s example shows, articulating a company’s strategic intent in M&A is helpful for guiding target screening and integration. However, truly committing to M&A as a critical element of growth requires more; it requires significant capital investment.

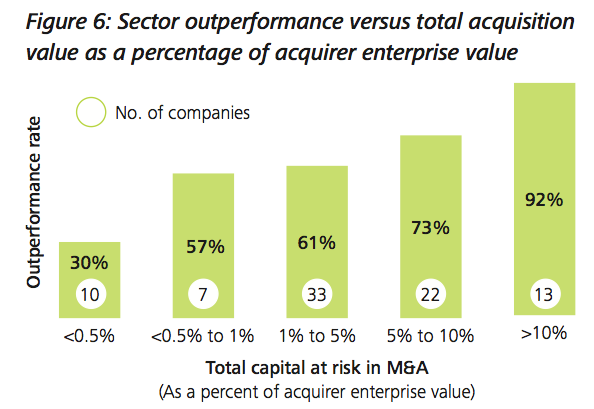

To measure each company’s capital investments in M&A, we analyzed its acquisitions over the past decade, comparing acquisition value to the acquirer’s enterprise value at the time of acquisition. The ratio of the two is a relative measure of the company’s total capital at risk in M&A. The larger the ratio, the more the company is investing in M&A. Interestingly, the more that A&D companies invest in M&A, the higher their likelihood of outperforming the sector, as seen in Figure 6.

With such a strong correlation between capital at risk and the likelihood of achieving objectives, it is worth discussing a potential bias in the results. Like other studies of risk and return over long time periods, a survivor’s bias tends to favor aggressive strategies by implicitly omitting companies that took big risks that did not pay off, and that subsequently failed or were bought by stronger competitors. However, another factor provides a better explanation to understanding this relationship: the acquisition size and what it suggests about a company’s approach to M&A.

Companies that put more of their capital at risk in M&A typically make larger acquisitions, and larger acquisitions have a few distinct advantages. In our experience, larger targets are often vetted more extensively, and their integrations are approached more programmatically. Most companies typically invest more resources in due diligence and integration planning when making a large investment that is likely to garner shareholder attention. But perhaps the most significant advantage of large transactions is that in order to justify the acquisition premium, investors demand that acquirer management teams convincingly communicate to investors the value created by the combined entity and a practical plan to capture it. The time and effort dedicated to answer investors’ questions is likely to pay off in more effective post-merger integrations.

3. Most top-performing companies acquire entities whose business models they can leverage to increase their market power.

Most companies can improve their chances of post- merger integration effectiveness by targeting companies with business models that are compatible with their own. Often, the most compatible model is an identical one, but there are cross-segment combinations where the acquirer’s and the target’s business models are quite complementary.

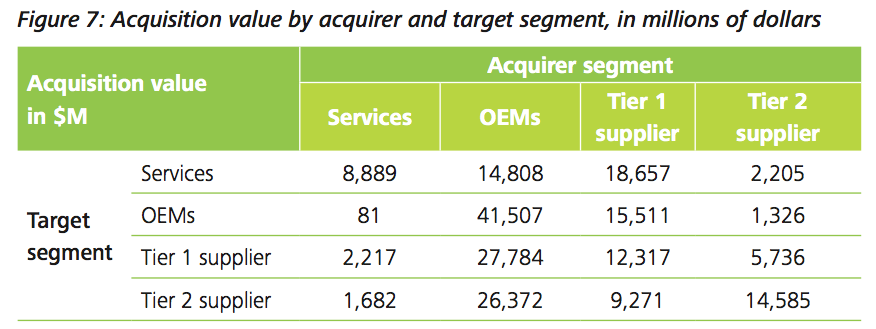

As discussed earlier, A&D acquirers and targets typically fall into one of four broad industry and value chain segments: Tier 2 suppliers, Tier 1 suppliers, Original Equipment Manufacturers (OEMs), and Services. We compared these categorizations to determine where the majority of the M&A activity in past decade has taken place; particularly, which companies made acquisitions in which segments. The relative concentration of acquisition values appears in Figure 7.

This matrix shows where acquirers are making investments through M&A:

- Services companies predominantly acquire other services companies.

- OEMs, as a segment, are the most acquisitive segment, comprising over 50 percent of M&A activity.

- Both OEMs and Tier 1 suppliers are using M&A to expand their position in the value chain, moving into both upstream and downstream segments.

- Tier 2 suppliers predominantly buy other Tier 1 and Tier 2 suppliers.

These high-level figures include all the companies in the sample, irrespective of their TSR performance over the period. However, when we analyze the remaining segments based on their financial performance, another picture emerges wherein OEMs, Tier 1, and Tier 2 suppliers each provide different insights into business model compatibility.

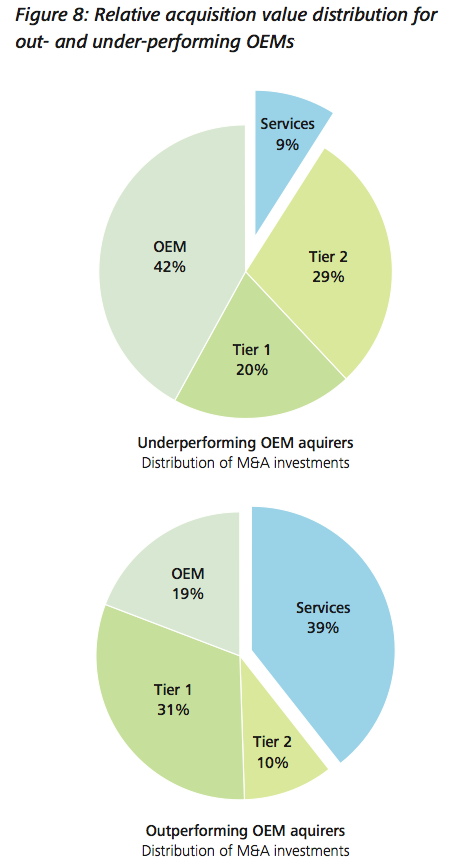

OEMs

OEMs that acquired services companies fared better than others As depicted in Figure 8, the most dramatic difference between the M&A investments of under- and out-performing OEMs is their degree of investment in services companies. Out-performers invested 40 percent of their investments in services companies, roughly four times as much as the segment’s under-performers. This is a strong example of complementary business models across industry segments. Maintenance, Repair, and Overhaul (MRO) services companies, as an example, give OEMs the opportunity to capture customer usage data, which OEMs can, in turn, use to better plan their operations and potentially reduce sustainment costs. Many OEMs have made expansion into aftermarket, IT, and mission system- related services a strategic imperative, and acquisitions can help to accelerate OEMs’ entry into those spaces.

Acquisitions of other OEMs, or horizontal moves, appear to be decidedly less effective strategies. Given the level of consolidation among the major primes during the 1980s and 1990s, this is unsurprising: much of the potential value in operating and cost synergies had already been captured.

These factors combine to put OEM acquirers in an unusual position: they are among the only industry entities whose leading prospects in M&A lie outside their segment. Tier 1 suppliers, on the other hand, provide a different perspective on business model compatibility.

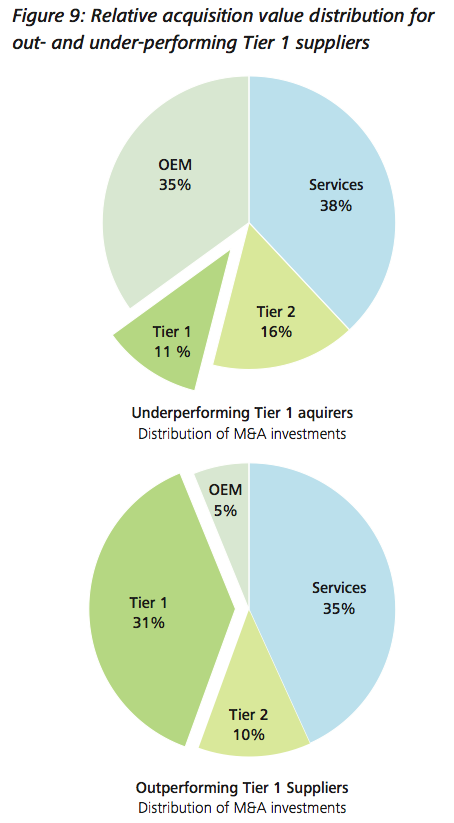

Tier 1 suppliers

Tier 1 suppliers that acquired OEMs struggled, while horizontal acquirers fared better

As seen in Figure 9, The most significant differences between the M&A investments of Tier 1 supplier under- and outperformers is that the more effective companies focused more of their investments on other Tier 1 suppliers. Acquiring other companies within the same industry segment is essentially horizontal consolidation. The activities of OEMs in the 1980s and 1990s demonstrated how consolidation in the A&D industry could lead to scale economies and improved negotiating positions with suppliers and channel partners.

Many Tier 1 suppliers have learned this lesson from their customers, the OEMs. As their customers’ negotiating power has improved, perceptive Tier 1 suppliers have begun imitating them and consolidating as well. Others are learning the hard way, with increasing customer concentration and margin pressure.

Already, Tier 2 suppliers have begun responding in kind. The consolidation trend continues to move down the value chain.

Tier 2 suppliers

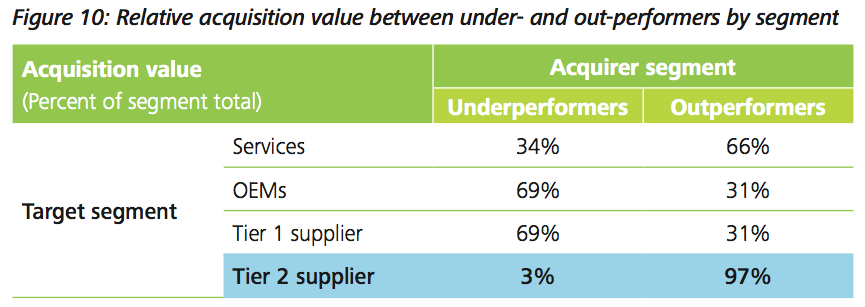

Acquisitive Tier 2 suppliers fared better than others

For Tier 2 suppliers, the most dramatic difference between under- and out-performers is not where they invested, but how much they invested. Of the $23.9 billion invested by Tier 2 acquirers, $23.1 billion was invested by segment out-performers; in other words, the financially effective Tier 2s are the more acquisitive companies (Figure 10). A significant share of Tier 2’s acquisition value was invested in services firms. This is another example of complementary business models across segments: MRO services companies can give acquirers the ability to compete on spare parts distribution and component overhaul services due to FAA rules on Parts Manufacturer Approval (PMA) and expanded repair.

Ultimately, these findings help to support the assertions about the most active segments for M&A activity in the coming years: consolidation within Tier 1 and 2 suppliers, and services companies as an increasingly attractive target for OEMs. To translate those assertions into their underlying business logic — targeting companies whose business models acquirers can leverage to increase their market power — is what can help industry leaders make more effective choices in developing their own M&A strategies.

Getting started: Consider acting on the three keys to M&A effectiveness

A&D executives typically face a complex challenge when developing an effective and executable M&A strategy. Doing so requires careful consideration of several factors: business model compatibility between the acquirer and the target, evolving customer requirements, and changes in the regulatory environment — all before dealing with the economics and integration of any single acquisition. Nevertheless, the boom in industry M&A is beginning and acquirers should prepare to take full advantage of the resulting opportunities.

This is where Deloitte professionals can add value. We have extensive industry experience with aircraft manufacturers, suppliers, operators, and services companies. We also have helped our clients execute effectively across the full M&A life cycle: strategy development, target screening, due diligence (including accounting, tax, and employee benefits diligence), tax structuring and valuation as well as integration planning. We bring client-tested approaches and methodologies that incorporate effective industry practices and deliver real value — all to help you achieve meaningful results.

Stay up to date with M&A news!

Subscribe to our newsletter