Introduction

Since the 2014 edition of this publication, the People’s Republic of China’s (PRC) tax provisions relevant to mergers and acquisitions (M&A) have changed significantly. China is at the forefront of implementing the Organisation for Economic Co-operation and Development (OECD) Base Erosion and Profit Shifting (BEPS) program and issued the Chinese language versions of the BEPS deliverables. The State Administration of Taxation (SAT) also issued the public discussion draft on special tax adjustments (not finalized at the time of writing) regarding general anti-avoidance rules (GAAR) and transfer pricing.

At the same time, the Chinese tax administration system is transitioning from a pre-approval system to a post-transaction filing administration. Against this backdrop, the SAT issued a series of new regulations in 2014 and 2015 in respect of offshore indirect disposals of Chinese taxable assets, treaty relief claims, corporate reorganizations and value added tax (VAT) reform. New developments regarding the land appreciation tax (LAT) have been observed regarding onshore indirect disposals of properties.

This report highlights these recent developments and then addresses the three fundamental decisions faced by a prospective purchaser undertaking M&A transactions in the PRC:

- What should be acquired: the target’s shares or its assets?

- What will be the acquisition vehicle?

- How should the acquisition vehicle be financed?

Recent developments

Offshore indirect disposals

China’s existing indirect offshore disposal reporting and taxation rules were completely revamped, with SAT Announcement [2015] No. 7 (Announcement 7) supplanting the earlier Guoshuihan [2009] No. 698 (Circular 698).

The indirect offshore disposal rules seek to ensure that Chinese tax cannot be avoided through the interposition of an offshore intermediary holding entity that holds the Chinese assets. Under these rules, if an indirect offshore disposal of Chinese taxable property (discussed further below) by a non-PRC tax-resident enterprise (TRE) is regarded as being undertaken without reasonable business purposes with the aim to avoid PRC corporate income taxes (CIT), the transaction would be re-characterized as a direct transfer of Chinese taxable property and subject to PRC withholding tax (WHT) at the rate of 10 percent under the PRC GAAR. However, the tax basis for calculating taxable gains for indirect transfers has been unclear, and the practice varies between different locations and tax authorities.

Compared with Circular 698, Announcement 7 expands the scope of the transactions covered, enhances the enforcement mechanism and sets a more specific framework for dealing with so-called tax arrangements with the introduction of a safe harbor and a black list. The major aspects of the rules under Announcement 7 are as follows:

- A much broader range of ‘Chinese taxable property’ is potentially subject to indirect transfer case assessment. Whereas Circular 698 solely caught transfers of offshore holding companies that ultimately own shares of Chinese companies, Announcement 7 also encompasses foreign companies holding Chinese immovable properties and assets belonging to Chinese permanent establishments (PE) of foreign companies. The types of offshore transactions that can trigger the rules are also expanded from simple offshore equity transfers to also cover transfers of partnership interests/convertible bonds, as well as restructurings and potentially share redemptions.

- A withholding mechanism is introduced, coupled with a new approach to reporting transactions. Previously, Circular 698 made the seller responsible for reporting transactions and for paying any additional tax that the tax authorities regarded as due. Announcement 7 requires the buyer to act as the withholding agent and apply 10 percent WHT to the purported transfer gain. The withholding agent faces stringent penalties for failure to pay tax within the allotted timeframe if the seller also fails to pay its taxes. However, the buyer can mitigate potential penalties by making a timely reporting of the transaction. Note that the seller, as the taxpayer, is still on the hook for tax not withheld by the buyer.

- Extensive new guidance was introduced on whether a transaction lacks ‘reasonable business purposes’ and thus should be subject to tax under the PRC GAAR. This includes a ‘7 factors test’, which holistically considers:

- whether the offshore company’s principal value or source of income is derived from China

- the functionality and duration of existence of the offshore holding company and ‘substitutability’ of the offshore transaction with an onshore direct disposal of the Chinese taxable assets

- the overseas taxation position of the offshore transfer, including the application of double tax treaties.

A parallel ‘automatic deeming’ test was introduced, which applies to treat an indirect transfer transaction as lacking reasonable business purpose if, among other black-list factors, more than 75 percent of the value and more than 90 percent of the income or assets of the offshore holding company are derived from or attributable to China. New safe harbor rules to deem a transaction as having ‘reasonable business purposes’ or otherwise not taxable and cover:

- foreign enterprises buying and selling securities on the public market

- cases where a tax treaty would apply to cover a transaction recharacterized as a direct disposal

- intragroup reorganizations within a corporate group that meet certain conditions.

In practice, Announcement 7 creates many challenges in its application to indirect transfer transactions due to difficulties aligning buyer and seller positions on the reporting and taxability of an indirect transfer M&A transaction. The seller and buyer sometimes find it difficult to agree on whether the PRC tax authorities would consider an indirect transfer transaction as lacking reasonable business purposes and at risk of being subject to tax, particularly where there is certain substance offshore. Given the potential stiff penalties that could apply, particularly for buyers as the withholding agents, and given the potential mitigation of penalties through timely voluntary reporting, disputes can arise between transacting parties over whether transactions should be reported at all and whether, and how much, tax needs to be paid or withheld. Historically, escrow and indemnity arrangements have been used in practice. Now, buyers increasingly tend to require sellers to timely report the transaction to the tax authorities and settle the relevant tax liability as a condition for closing the deal.

Since its issuance, Announcement 7 has been supplemented by Shuizonghan [2015] No. 68 (Circular 68), which provides further implementation guidance and an improved reporting mechanism. The circular clarifies Announcement 7’s measures regarding formal receipts for taxpayer reporting (giving assurance in relation to the penalty mitigation measures), single reporting for transferred Chinese assets in multiple tax districts and GAAR procedures (including SAT review and appeal procedures). However, there is still a need for a clarified refund process, confirmation on the applicability of safe harbors, and timeframes for the conclusion of GAAR investigations.

Also, as noted in the 2014 edition of this publication, in relation to offshore indirect disposals, the Vodafone–China Mobile case, first published in April 2011, highlighted that the gain on the sale of an offshore company may be regarded simply as PRC-sourced, giving the right to the PRC tax authorities to tax the resulting gain on the basis of the offshore company’s deemed PRC tax residence under PRC domestic tax laws (broadly based on place of effective management). The approach was applied in a Circular 698 reporting case in the Heilongjiang province of China in 2012. This indicates the PRC tax authorities may have stepped up their efforts to look at the registered and unregistered tax resident status of foreign incorporated enterprises controlled by PRC residents in order to tax gains from the disposal of Chinese equities offshore by foreign investors, including those in the M&A space.

This additional exposure needs to be monitored and factored into M&A transactions where foreign investors make offshore indirect acquisitions and disposals of Chinese investments. Negotiations may be further complicated where investors seek to obtain warranties and indemnities that the deal target is not effectively managed from the PRC.

VAT/LAT on onshore indirect disposals of properties

Technically speaking, pursuant to the PRC LAT regulations, a transfer of an equity interest in PRC tax-resident enterprises should not give rise to LAT as any underlying properties are not directly transferred. However, the tax authorities may seek to impose LAT on the transfer of an equity interest in a PRC company that directly holds real estate if the transfer consideration is equivalent to the value of the real estate and/or the primary purpose of the equity transfer is to transfer the land use right and property (rather than the company). There have been some enforcement cases where transfers of equity interests in PRC property holding companies were re-characterized as direct transfers of PRC properties for LAT purposes and thus LAT was imposed on the sale of equity interests in the PRC holding company as if the underlying property had been disposed of.

Further, a recent local tax circular issued by the Hunan tax authority, i.e., Xiang Di Shui Cai Xing Bian Han [2015] No.3, clarifies that the ‘transfer of properties in the name of transfer of equity’ should be subject to LAT, based on the grounds that the transfer of PRC company shares, which in substance represents a transfer of the underlying PRC properties, should be subject to LAT.

At the moment, only transactions that are deemed as ‘disguised’ property transfers would be subject to LAT, which would be assessed on a case-by-case basis. In making the assessments, the PRC tax authorities would look at certain criteria to decide whether the nature of the transaction is in substance a property transfer transaction. These criteria include:

- whether the share transfer consideration was equal to, or close to the valuation of the PRC properties

- the duration of the holding period

- the transaction agreements.

The look-through of an equity transfer to impose LAT is not explicitly supported by existing LAT law (which, unlike the CIT Law, does not have an anti-avoidance provision). Hence, these look-through cases are still rare in practice, but investors should closely monitor future developments as this approach could significantly affect investment returns.

The position under China’s new VAT rules which have been in effect since 1 May 2016 is similar. That is, the transfer of unlisted equity interests is not subject to VAT. However, the transfer of real estate assets is generally subject to 11 percent VAT (though in some cases may attract a reduced rate of 5 percent VAT, where certain grandfathering arrangements apply). The new VAT rules contain an anti-avoidance provision and it cannot be ruled out that the tax authorities may take a look-through approach similar to the above on LAT and impose VAT on disguised transfers of properties via equity transfers.

Treaty relief claims

In 2009, the PRC tax authorities took measures to monitor and resist granting tax treaty relief to perceived treaty shopping through the use of tax treaties to gain tax advantages. Guoshuifa [2009] No. 124 (Circular 124, issued in 2009, which is now superseded by another tax circular; see below) introduced procedural requirements under which tax authority pre-approval may be required before tax treaty relief can be applied.This made it easier for the tax authorities to identify cases where the taxpayer is relying on treaty protection. Guoshuihan [2009] No. 601 (Circular 601), also issued in 2009, sets out the factors that the Chinese tax authorities take into account in deciding whether a treaty’s beneficial ownership requirements are satisfied.

To provide further clarity, the SAT issued SAT Announcement [2012] No. 30 (Announcement 30) in June 2012, and Shuizonghan [2013] No. 165 (Circular 165 ) in April 2013, to provide guidance on the interpretation of the negative factors under Circular 601 for determining beneficial ownership for purposes of tax treaty relief claims. In order to be considered the beneficial owner under Circular 601 and Announcement 30, the income recipient should not constitute a shell or conduit company and should not exhibit a number of negative factors that indicate the company is not the beneficial owner.

Under Circular 601, a company not only must control the disposition of the income and the underlying property but also “generally should conduct substantial business operations” to be considered as satisfying the beneficial ownership requirements. The many enforcement cases observed previously also indicate that the PRC tax authorities are focused on the business substance (e.g. hiring of staff, lease of premises, and conducting other activities) of the foreign company applying for treaty benefits. This has led many commentators to conclude that the Chinese beneficial ownership concept functions as a hybrid of the international concept of beneficial ownership and anti-abuse rules aimed at preventing treaty shopping.

Further, while the capital gains tax clauses in China’s tax treaties do not contain beneficial ownership requirements, the PRC tax authorities have repeatedly denied treaty relief for capital gains on the grounds of substance and the list of negative factors in Circular 601.

In 2015, the SAT issued SAT Announcement [2015] No. 60 (Announcement 60), which replaced Circular 124 and revamped the tax treaty relief system. The new tax treaty relief system under Announcement 60, which took effect from 1 November 2015, abolishes the tax treaty relief pre-approval system under Circular 124. Instead, the taxpayer self-determines whether tax treaty relief applies and informs the withholding agent (or the tax authority directly where no withholding agent is involved) that it will be using the tax treaty relief. To encourage the withholding agent to process the relief without taking on excessive risk and uncertainty, the detailed tax treaty relief forms, completed by the taxpayer, include a section requiring information that the withholding agent will check before using the tax treaty rate and a separate, more detailed section that the tax authorities may refer to in carrying out their follow-up procedures. The withholding agent’s section includes, along with basic details on how the taxpayer satisfies the terms of the tax treaty, a beneficial ownership test defined under Circular 601, which is a control test along the lines of that applied in other countries.

Following the release of Announcement 60, on 29 October 2015, the SAT further issued Shuizongfa [2015] No. 128 (Circular 128) to clarify the follow-up procedures as emphasized in Announcement 60. Circular 128 stipulates that the PRC tax authorities would audit at least 30 percent of the tax treaty relief claim cases on dividends, interest, royalties and capital gain within 3 months after the end of each quarter and perform special audits to assess the risks of tax treaty abuse in various aspects. If the tax authorities discover on examination that tax treaty relief should not have applied and tax was underpaid, the tax authorities would instruct the taxpayer to pay the underpaid tax within a limited time period. If the payment is not made on time, then the tax authorities can pursue other Chinese sourced income of the non-resident or take stronger enforcement action under the PRC Tax Collection and Administration Law. The tax authorities may also launch anti-avoidance proceedings, either under the relevant anti-abuse articles of tax treaties or under the domestic GAAR.

Depending on its implementation in practice, the new tax treaty relief system under Announcement 60 could open more efficient access to tax treaty relief and aid the conduct of M&A and restructuring transactions. However, taxpayers have a greater burden to ensure that self-assessment is grounded in prudence and that the relevant conditions, including those under Circular 601, are satisfied.

Circular 601 remains a hot button issue for foreign investors into China, including those in the M&A space. Its provisions created a need for groups to examine their existing or proposed holding company structures, consider their robustness and take remedial action where appropriate. Significant uncertainties also arise in this area, in particular regarding whether the claimant can support its treaty relief claim by referring to the substance in group companies in the same jurisdiction or in another jurisdiction with equivalent treaty provisions. Announcement 30 partly addressed this issue by introducing a safe harbor for certain listed company structures. However, the issue remains unclear for non-listed structures.

Reorganization relief

In 2014 and 2015, a number of key improvements to the Chinese tax restructuring reliefs were made to the special tax treatment (STT) that results in tax deferral treatment for corporate restructurings. The changes lower the eligibility threshold and introducing new ways to access STT.

Caishui [2009] No. 59 (Circular 59), the principal tax regulation on restructuring relief issued in 2009, sets out the circumstances in which companies undergoing restructuring can elect for STT. Absent the application of STT, the general tax treatment (GTT) requires recognition of gains/losses arising from the restructuring. The STT conditions include two tests:

- a ‘purpose test’ akin to the PRC GAAR (i.e. the transaction must be conducted for reasonable commercial purposes and not for tax purposes)

- a ‘continuing business test’ (i.e. there is no change to the original operating activities within a prescribed period after the restructuring).

The conditions also set two threshold tests that aim to ensure the continuity of ownership and the continued integrity of the business following the restructuring. Under these tests:

- consideration must comprise 85 percent of equity

- 75 percent of the equity or assets of the target must be acquired by the transferee.

Although Circular 59 was intended to provide favorable tax treatment to restructuring transactions, STT had not been widely used due to the high thresholds. Caishui [2014] No. 109 (Circular 109) lowers the 75 percent asset/equity acquisition threshold to 50 percent. This facilitates the conduct of many more takeovers/restructurings in a tax-neutral manner. Circular 109 also introduced a new condition for STT that removes the 75 percent ownership test. The new condition permits elective non-recognition of income on transfer of assets/equity between two Chinese TREs that are in a ‘100 percent holding relationship’, provided no accounting gains/losses are recognized. Both the purpose test and the continuing business test from Circular 59 hold, and the tax basis of transferred assets for future disposal is their original tax basis. The supplementary SAT Announcement [2015] No. 40 (Announcement 40) clarifies certain terms used in Circular 109 and spells out in detail the situations to which the relief applies.

Given that China does not, unlike many other countries, have comprehensive group relief or tax consolidation rules, the introduction of this intragroup transfer relief is a real breakthrough in Chinese tax law. Notably, however, the relief does not cover transfers of Chinese assets by non-TREs (whether between two non-TREs or between a non-TRE and a TRE). Taxpayers also need to be aware of the emphasis being placed by tax authorities on the purpose test, particularly as the intragroup transfer relief opens the door to tax loss planning strategies that previously were not possible under Chinese tax law.

SAT Announcement [2015] No. 48 (Announcement 48) also abolishes the tax authority pre-approvals previously needed for STT to be applied, moving instead to more detailed STT filing at the time of the annual CIT filing.The transition from tax authority pre-approval to taxpayer self-determination on the applicability of STT (and on tax treaty relief claims as discussed earlier) is in line with the broader shift in Chinese tax administration away from pre-approvals. However, while the abolition of pre-approvals potentially expedites transactions, it also places a greater burden on taxpayer risk management procedures and systems to ensure that treatments adopted are justified and adequately supported with documentation.

VAT reform

China’s transition from business tax (BT) to VAT has been a major tax reform initiative, which was designed to facilitate the growth and development of the services sector and to relieve the indirect tax impact in many business-to-business transactions. Since 2012, the VAT reforms have been gradually expanded to sectors which were historically under the BT regime, with the process reaching its finalization on 1 May 2016.

From 1 May 2016, all transactions involving goods or services are now potentially within scope of VAT, and BT is no longer in operation. The following sectors transitioned from BT to VAT from 1 May 2016: real estate and construction, financial services, and lifestyle services (which is a general category capturing all other services).

In the context of M&A transactions, the new VAT rules have a significant impact on how transactions take place, whether by way of asset or business transfer or equity. Furthermore, given the significant changes in VAT rates for some industries (compared with the previous BT rates), the ability to recover VAT under contracts which may be acquired or assumed as part of any M&A transactions is a significant area of focus. The funding of transactions also needs to take into account the VAT implications, given that China’s VAT system applies 6 percent VAT to financial services, including interest income.

Asset purchase or share purchase

In addition to tax considerations, the execution of an acquisition in the form of either an asset purchase or a share purchase in the PRC is subject to regulatory requirements and other commercial considerations.

Some of the tax considerations relevant to asset and share purchases are discussed below.

Purchase of assets

A purchase of assets usually results in an increase in the cost base of those assets for capital gains tax purposes, although this increase is likely to be taxable to the seller. Similarly, where depreciable assets are purchased at a value greater than their tax-depreciated value, the value of these assets is refreshed for purposes of the purchaser’s tax depreciation claim but may lead to a clawback of tax depreciation for the seller. Where assets are purchased, it may also be possible to recognize intangible assets for tax amortization purposes. Asset purchases are likely to give rise to relatively higher transaction tax costs than share purchases, which are generally taxable to the seller company (except for stamp duty which is borne by both the buyer and seller). Further, for asset purchases, historical tax and other liabilities generally remain with the seller company and are not transferred with the assets. As clarified in this chapter’s section on choice of acquisition funding, it may be more straightforward, from a regulatory perspective, for a foreign invested enterprise to obtain bank financing for an asset acquisition than for a share acquisition.

The seller may have a different base cost for their shares in the company as compared to the base cost of the company’s assets and undertaking. This, as well as a potential second charge to tax where the assets are sold and the company is liquidated or distributes the sales proceeds, may determine whether the seller prefers a share or asset sale.

Caishui [2014] No. 116 (Circular 116) allows for deferral of tax on gains deemed to arise on a contribution of assets by a TRE into another TRE in return for equity in the latter. The taxable gain can be recognized over a period up to 5 years, allowing for the payment of tax in instalments. This relief, potentially also extending to the contribution of assets by minority investors into a TRE, sits alongside and complements the intra-100 percent group transfer relief under Circulars 59 and 109 (which are discussed in the recent developments section. According to SAT Announcement [2015] No. 33 (Announcement 33), where applicable, taxpayers can elect to apply either the relief under Circular 116 or the intra-100 percent group transfer relief under Circulars 59 and 109.

Further, SAT Announcement [2011] No. 13 (Announcement 13), issued in February 2011, and SAT Announcement [2011] No. 51 (Announcement 51), issued in September 2011, respectively provided a VAT and BT exclusion for the transfer of all or part of a business pursuant to a restructuring. However, certain limitations in the practical applicability of the relief still exist.

Purchase price

For tax purposes, it is necessary to apportion the total consideration among the assets acquired. It is generally advisable for the purchase agreement to specify the allocation, which is normally acceptable for tax purposes provided it is commercially justifiable. It is generally preferable to allocate the consideration, to the extent it can be commercially justified, against tax-depreciable assets (including intangibles) and minimize the amount attributed to non-depreciable goodwill. This may also be advisable given that, at least under old PRC generally accepted accounting principles (GAAP), goodwill must be amortized for accounting purposes, limiting the profits available for distribution.

Goodwill

Under CIT law, expenditures incurred in acquiring goodwill cannot be deducted until the complete disposal or liquidation of the enterprise.

Amortization is allowed under the CIT law for other intangible assets held by the taxpayer for the production of goods, provision of services, leasing or operations and management, including patents, trademarks, copyrights, land-use rights, and proprietary technologies, etc. Intangible assets can be amortized over no less than 10 years using the straight-line method.

Depreciation

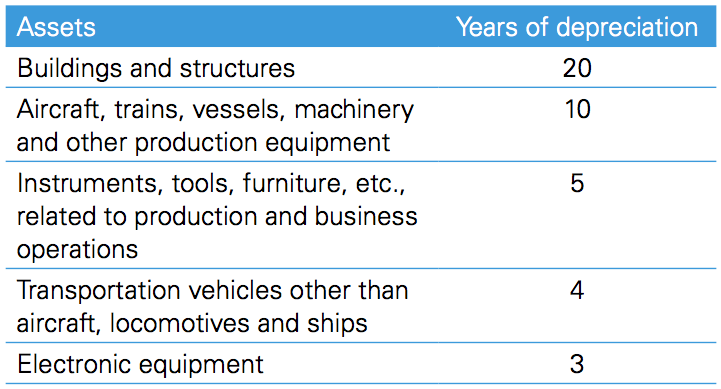

Depreciation on fixed assets is generally computed on a straight-line basis. Fixed assets refer to non-monetary assets held for more than 12 months for the production of goods, provision of services, leasing or operations and management, including buildings, structures, machinery, mechanical apparatus, means of transportation and other equipment, appliances and tools related to production and business operations.

The residual value of particular fixed assets (i.e. the part of the asset value that is not tax-depreciable) is to be reasonably determined based on the nature and use of the assets. Once determined, the residual value cannot be changed. The minimum depreciation periods for relevant asset types are as follows:

Any excessive accounting depreciation over the tax depreciation calculated based on the above minimum depreciation period should be added back to taxable income for CIT purposes.

Certain fixed assets are not tax-depreciable, including:

- fixed assets, other than buildings and structures, that are not in use

- fixed assets leased from other parties under operating or finance leases

- fixed assets that are fully depreciated but still in use

- fixed assets that are not related to business operations

- separately appraised pieces of land that are booked as fixed assets

- other non-depreciable fixed assets.

Tax attributes

Generally, tax attributes (including tax losses and tax holidays) are not transferred on an asset acquisition. They generally remain with the enterprise until extinguished.

Value added tax

With effect from 1 May 2016, VAT has fully replaced BT, such that any transactions involving the sale of goods or provision of services is potentially within scope of VAT. The applicable rates at which VAT is levied include 3 percent, 6 percent, 11 percent, 13 percent and 17 percent. Generally the sale of importation of goods, or the lease of goods is subject to 17 percent VAT, transportation, certain telecommunication services as well as sales and lease of real estate are subject to 11 percent VAT, while most other services are subject to 6 percent VAT.

Certain business reorganizations, including certain transfers of a business where all assets are disposed of, employees transferred and liabilities assumed, are currently outside the scope of VAT, provided certain conditions are met.

However, the scope of the concession is more limited in China compared with equivalent concessions for the sale of a going concern in other countries. A sale of assets, in itself, may not be regarded as a transfer of a business and should not benefit from the concession. Announcement 13, issued in February 2011, clarified that a VAT exclusion may be available for the transfer of part of a business, though in practice it can be difficult to access. Given that in China there is generally no ability for a purchaser to obtain a refund of excess VAT credits (instead, excess credits may be carried forward, potentially for an indefinite period), the cashflow implications can be significant and long-lasting.

Transfer taxes

Stamp duty is levied on instruments transferring ownership of assets in the PRC. Depending on the type of assets, the transferor and the transferee are each responsible for paying stamp duty of 0.03 to 0.05 percent of transfer consideration for the assets in relation to their own copies of the transfer agreement (i.e. a total of 0.06 percent to 0.10 percent stamp duty payable). Where the assets transferred include immovable property, deed tax, land appreciation tax and VAT and local surcharges may also need to be considered.

Purchase of shares

The purchase of a target company’s shares does not result in an increase in the base cost of that company’s underlying assets; there is no deduction for the difference between underlying net asset values and consideration. There is no capital gains participation exemption in PRC tax law, so a PRC seller is subject to PRC CIT or WHT on the sale of shares, unless the consideration primarily consists of shares in the buyer and reorganization relief (discussed in the section on equity later in this report) can be obtained.

Tax indemnities and warranties

In a share acquisition, the purchaser assumes ownership of the target company together with all of its related liabilities, including contingent liabilities. Therefore, the purchaser normally needs more extensive indemnities and warranties than in the case of an asset acquisition. An alternative approach is for the seller’s business to be hived down into a newly formed subsidiary so the purchaser can acquire a clean company. However, for tax purposes, unless tax relief applies, this may crystallize any gains inherent in the underlying assets and may also crystallize a tax charge in the subsidiary to which the assets were transferred when acquired by the purchaser.

As noted earlier in the recent developments section, a pressing new issue that must be dealt with through warranties and indemnities concerns the impact on purchasers of shares in offshore holding companies where the seller has not complied with the Announcement 7 (previously Circular 698) reporting/tax filing requirements. Purchasers are subject to WHT obligations in the case of an Announcement 7 enforcement and could be subject to potential penalty where the seller fails to report the transaction and pay the taxes. Purchasers may ask the seller to warrant, and provide evidence, that they have made the reporting or indemnify them for tax/penalty ultimately arising.

To identify such tax issues, it is customary for the purchaser to initiate a due diligence exercise, which normally incorporates a review of the target’s tax affairs.

Tax losses

Under the CIT law, generally, a share transfer resulting in a change of the legal ownership of a PRC target company does not affect the PRC tax status of the PRC target company, including tax losses. However, since the introduction of the GAAR, the buyer and seller should ensure that there is a reasonable commercial rationale for the underlying transaction and that the use of the tax losses of the target is not considered to be the primary purpose of the transaction, thus triggering the GAAR’s application.

Provided that the GAAR does not apply, any tax losses of a PRC target company can continue to be carried forward to be offset against its future profits for up to 5 years from the year in which the loss was incurred after the transaction. PRC currently has no group consolidation regulations for grouping of tax losses.

There is a limitation on the use of tax losses through mergers.

Crystallization of tax charges

The PRC does not yet impose tax rules to deem a disposal of underlying assets under a normal share transfer, but the purchaser should pay attention to the inherent tax liabilities of the target company on acquisition and the application of GAAR. As PRC tax law does not provide for loss- or VAT-grouping, there is no ‘degrouping’ charge to tax (although care must be taken on changes of ownership where assets/shareholdings have recently been transferred within the group and the reorganization relief has been claimed). However, the tax authorities may seek to impose BT/LAT on a ‘disguised’ property transfer under the cover of an equity transfer, although the imposition of LAT and BT based on the look-through of the equity transfer is not explicitly supported by existing LAT or BT laws, as discussed in the recent development section.

Pre-sale dividend

In certain circumstances, the seller may prefer to realize part of the value of the target company as income by means of a pre-sale dividend. The rationale here is that the dividend may be subject to a lower effective rate of dividend WHT than capital gains, subject to the availability of tax treaty relief requiring satisfaction of the ‘beneficial ownership’ requirements, among others. Hence, any dividends paid out of retained earnings prior to a share sale reduce the proceeds of sale and thus the gain arising on the sale, leading to lower WHT leakage overall. The position is not straightforward, however, and each case must be examined on its facts.

Transfer taxes

The transferor and transferee are each responsible for the payment of stamp duty of 0.05 percent of the transfer consideration for the shares in a PRC company in relation to their own copies of the transfer agreement (i.e. a total of 0.10 percent stamp duty payable).

Tax filing requirements for STT on special corporate reorganizations

The STT on special corporate reorganizations is elective. To enjoy the tax deferral under a corporate reorganization, companies must submit, along with their annual CIT filings, relevant documentation to substantiate their reorganizations’ qualifications for the STT. Failure to do so results in the denial of the tax-deferred treatment.

Tax clearance

Currently, the PRC tax authorities do not have any system in place for providing sellers of shares in an offshore holding company, where the sellers have made their Announcement 7 (previously Circular 698) reporting, with a written clearance to the effect that the arrangement will not be attacked under the GAAR. Consequently, as noted above, purchasers should seek to protect themselves through appropriate warranties and indemnities.

Choice of acquisition vehicle

The main forms of business enterprise available to foreign investors in China are discussed below.

Foreign parent company

The foreign purchaser may choose to make the acquisition itself, perhaps to shelter its own taxable profits with the financing costs. However, the PRC charges WHT at 10 percent on dividends, interest, royalties and capital gains arising to non-resident enterprises. So, if relevant, the purchaser may prefer an intermediate company resident in a more favorable treaty territory (WHT can be reduced under a treaty to as low as 5 percent on dividends, 7 percent on interest, 6 percent on royalties and 0 percent on capital gains). Alternatively, other structures or loan instruments that reduce or eliminate WHT may be considered.

Non-resident intermediate holding company

If the foreign country taxes capital gains and dividends received from overseas, an intermediate holding company resident in another territory could be used to defer this tax and perhaps take advantage of a more favorable tax treaty with the PRC. However, as outlined earlier in the report’s recent developments section, the purchaser should be aware of the rigorous enforcement of the anti-treaty shopping provisions by the Chinese tax authorities — especially against the backdrop of the OECD BEPS Action Plan, which may restrict the purchaser’s ability to structure a deal in a way designed solely to obtain such tax benefits.

Further, Circular 601, in setting out the Chinese interpretation of beneficial ownership for tax treaty relief, effectively combined a beneficial ownership test (which in most countries is a test of ‘control’ over income and the assets from which it derives) with an economic substance-focused treaty-shopping test. Application of the treaty-shopping test as an element of the beneficial ownership test, rather than as an application of the PRC GAAR, prevented taxpayers from arguing their ‘reasonable business purposes’ in using an overseas holding, financing or intangible property leasing company, as the GAAR procedures would allow them to do. The public discussion draft on ‘special tax adjustments’ (not yet finalized at the time of writing) reiterated that the PRC tax authorities are empowered to initiate general anti-avoidance investigations and apply the GAAR on treaty shopping. Hence, the development of the BEPS implementation in China and the issuance of the trial the GAAR rules should continue to be observed under the new tax treaty relief system.

Announcement 7 must also be borne in mind if an offshore indirect disposal is contemplated. However, even in the absence of treaty relief, the 10 percent WHT compares favorably with the 25 percent tax that would be imposed if the acquisition were held through a locally incorporated vehicle.

Further, as explained in the later section on debt financing, debt pushdown at the PRC level may be difficult, and the PRC corporate law requirement to build up a capital reserve that may not be distributed until liquidation might also favor the use of a foreign acquisition vehicle (however, see the comments on PRC partnerships later). Where the group acquired has underlying foreign subsidiaries, the complexities and vagaries of the (little-used) PRC foreign tax crediting provisions must also be taken into account.

Wholly foreign-owned enterprise

- A wholly foreign-owned enterprise may be set up as a limited liability company by one or more foreign enterprises or individuals.

- Profits and losses must be distributed according to the ratio of each shareholder’s capital contribution. Earnings are taxed at the enterprise level at the standard 25 percent rate and WHT applies at standard rate of 10 percent on dividends.

- Asset acquisitions may be relatively easier to fund than share acquisitions from a regulatory viewpoint (see the section on choice of acquisition funding later in this report).

- Must reserve profits in a non-distributable capital reserve of up to 50 percent of amount of registered capital.

- May be converted to a joint stock company (company limited by shares) for the purposes of listing on the stock market.

Joint venture

- Joint ventures can be formed by one or more PRC enterprises together with one or more foreign enterprises or individuals either as an equity joint venture or cooperative joint venture.

- An equity joint venture may be established as a limited liability company. The foreign partners must own at least 25 percent of the equity interest.

- Profits and losses of the equity joint venture must be distributed according to the ratio of each partner’s capital contribution, and the tax and corporate law treatment is the same as for wholly foreign-owned enterprises, as described earlier.

- A cooperative joint venture may be established as either a separate legal person with limited liability or as a non-legal person.

- Profits and losses may be distributed according to the ratio agreed by the joint venture agreement and can be varied over the contract term.

- Where the joint venture is a separate legal person, the earnings are taxed at the enterprise level at the standard 25 percent rate; otherwise, the earnings are taxed at the investor level.

- WHT applies at a standard rate of 10 percent on dividends paid by the legal person cooperative joint venture. Distributions by the non-legal person variant may not bear WHT, but the joint venture partner may be exposed to PRC PE risk. The structure bears similarities to the partnership form (which is increasingly preferred).

Chinese holding company

- Must have a minimum registered capital of 30 million US dollars (USD), which can be used to provide equity to the Chinese holding company’s (CHC) subsidiaries or to make third-party acquisitions.

- A CHC can finance the purchase of a Chinese subsidiary from another group company through a mixture of equity and shareholder debt, in line with the ‘debt quota’.

- Permitted to obtain registered capital/loans from abroad to finance equity acquisitions (but cannot borrow domestically to finance equity acquisitions).

- Same tax treatment as wholly foreign-owned enterprises (10 percent WHT, 25 percent CIT on profits and gains) and same corporate law restrictions.

- Dividends paid to a CHC from its Chinese subsidiaries are not subject to WHT or to any tax in the CHC as the recipient.

- A CHC can reinvest the dividends it receives directly without being deemed to pay a dividend.

Chinese partnership

- Foreign partners are allowed to invest in Chinese limited partnerships as of March 2010.

- Profits and losses are distributed in accordance with partnership agreement.

- Unlike a corporate entity, there is no capital reserve requirement.

- Taxed on a look-through basis, although there is some uncertainty regarding the taxation of foreign partners.

- For an active business, the foreign partner should be taxed at 25 percent as having a PE in the PRC, which in effect potentially eliminates the double taxation that arises with regard to dividend WHT in a corporate context.

- Where a partnership receives passive income, it is unclear whether a foreign partner is treated as receiving that income (with potential treaty relief) or as having a PE in the PRC.

- Uncertainty regarding treatment of tax losses and stamp duty.

Choice of acquisition funding

Generally, an acquiring company may fund an acquisition with equity or a combination of debt and equity. Interest paid or accrued on debt used to acquire business assets may be allowed as a deduction to the payer. Historically, under the State Administration of Foreign Exchange (SAFE) Circular 142, if a PRC-established entity is used as the acquisition vehicle, the entity may not be allowed to borrow monies or obtain registered capital from abroad to fund an equity acquisition in China. This prohibition has been removed by SAFE Circular 19, which is issued in 2015, albeit practice in this regard may still need to be observed. Borrowing locally for acquisition is normally not possible due to the general People’s Bank of China (PBOC) prohibition on lending to fund equity acquisitions (and the limited interest of local banks in using the legal exceptions that do exist to lend to foreign invested enterprises — FIE). However, a CHC may be in a position to borrow/obtain registered capital from abroad to fund an equity acquisition.

Debt

Per Ministry of Commerce (MOFCOM) rules, funding an acquisition with foreign debt is subject to the limitation of the investee company’s registered capital to total investment ratio. The registered capital of an FIE is the sum of the amount of equity that is contributed by the investors in the enterprise. The total investment of an FIE is the sum of its registered capital and the maximum amount of a foreign loan that an enterprise is permitted to borrow.

The minimum ratios of registered capital to total investment are generally as follows:

Loans from a foreign lender to a Chinese borrower must be registered with the local branch of SAFE. Where an acquisition is funded by foreign debt, the FIE must register the foreign debt within 15 days of signing of the loan agreement. Without the proper registration, the FIE is not legally permitted to remit principal and interest payments outside China.

Any related-party loans also need to comply with the arm’s length principle under the PRC transfer pricing rules.

Deductibility of interest

Under the CIT law, non-capitalized interest expenses incurred by an enterprise in the course of its business operations are generally deductible for CIT purposes, provided the applicable interest rate does not exceed applicable commercial lending rates.

The CIT law also contains thin capitalization rules that are generally triggered, for non-financial institutions, when a resident enterprise borrows money from a related party that results in a debt-to-equity ratio exceeding the 2:1 ratio stipulated by the CIT law. Interest incurred on the excess portion is not deductible for CIT purposes. The arm’s length principle must be observed in all circumstances.

Where a CHC has been used as the acquisition vehicle, it should have sufficient taxable income (from an active business or from capital gains; dividends from subsidiaries are exempt) against which to apply the interest deduction, as tax losses (created through interest deductions or otherwise) expire after 5 years. Alternative approaches to utilizing the losses are not available as loss grouping is not provided for under the PRC law. Thus, CHCs generally are not able to merge with their subsidiaries (precluding debt pushdown), and problems may arise for a non-CHC in obtaining a tax-free vertical merger.

Withholding tax on debt and methods to reduce or eliminate it

Payments of interest by a PRC company to a non-resident without an establishment or place of business in the PRC are subject to WHT at 10 percent. The rate may be reduced under a tax treaty. Under the VAT reforms which have been implemented for the financial services industry with effect from 1 May 2016, VAT at 6 percent is levied on interest income earned by non-residents from a PRC company and, according to the rules, the VAT charged will not be creditable to the PRC company.

Under Announcement 60, a taxpayer or its withholding agent is required to submit the relevant documents to the PRC tax authorities when making the tax filing for accessing treaty benefits (e.g. reduced interest WHT rate). As discussed above, while no pre-approval is required for enjoying the treaty benefits, the tax authorities may conduct post-filing examinations. Where it is discovered that tax treaty relief should not have applied and tax has been underpaid, the tax authorities will seek to recover the taxes underpaid and may launch anti-avoidance proceedings.

Checklist for debt funding

- Consider whether application of SAFE and PBOC rules precludes debt financing for foreign investment in the circumstances and in the industry.

- The use of third-party bank debt may mitigate thin capitalization and transfer pricing issues.

- Consider what level of funding would enable tax relief for interest payments to be effective.

- It is possible that a tax deduction may be available at higher rate than the applicable tax on interest income in the recipient‘s jurisdiction.

- WHT of 10 percent applies to interest payments to non-PRC entities unless a lower rate applies under the relevant tax treaty.

Equity

A purchaser may use equity to fund its acquisition, possibly by issuing shares to the seller, and may wish to capitalize the target post-acquisition. However, reduction of share capital/share buy-back in a PRC company may be difficult, and the capital reserve rules may cause some of the profits of the enterprise to become trapped.The use of equity may be more appropriate than debt in certain circumstances, in light of the foreign debt restrictions highlighted above and the fact that, where company is already thinly capitalized, it may be disadvantageous to increase borrowings further.

Provided that the necessary criteria are satisfied, Circular 59 provides a tax-neutral framework for structuring acquisitions under which the transacting parties may elect temporarily to defer recognizing the taxable gain or loss arising on the transactions (a qualifying special corporate reorganization).

One of the major criteria for qualifying as a special corporate reorganization is that at least 85 percent of the transaction consideration should be equity consideration (i.e. stock-for-stock or stock-for-assets). Other relevant criteria include:

- The transaction is motivated by reasonable commercial needs, and its major purpose is not achieving tax avoidance, reduction, exemption or deferral.

- The ratio of assets/equity that are disposed, merged or split-off meets the prescribed threshold ratio for share transfers, that is, at least 75 percent of the target’s shareholding needs to be transferred.

- The operation of the reorganized assets will not change materially within a consecutive 12-month period after the reorganization.

- Original shareholders receiving consideration in the form of shares should not transfer such shareholding within a 12-month period after the reorganization.

For qualifying special corporate reorganizations, the tax deferral is achieved through the carryover to the transferee of tax bases in the acquired shares or assets but only to the extent of that part of the purchase consideration comprising shares. Gains or losses attributable to non-share consideration, such as cash, deposits and inventories, are recognized at the time of the transaction.

As discussed in the recent developments section. Circular 109 lowers the 75 percent asset/equity acquisition threshold to 50 percent under Circular 59. This facilitates the conduct of many more takeovers/restructurings in a tax-neutral manner. In addition to the ratio relief, Circular 109 introduced a new condition for STT that removes the 75 percent ownership test under Circular 59. The new condition permits elective non-recognition of income on transfer of assets/equity between two Chinese TREs that are in a ‘100 percent holding relationship’, provided no accounting gains/losses are recognized. Both the purpose test and the continuing business test in Circular 59 hold, and the tax basis of transferred assets for future disposal is their original tax basis.

Certain cross-border reorganizations need to meet conditions in addition to those described earlier to qualify for the special corporate reorganization, including a 100 percent shareholding relationship between the transferor and transferee when inserting an offshore intermediate holding company.

SAT Announcement [2013] No. 72 (Announcement 72) addresses situations where a cross-border reorganization involves the transfer of the PRC enterprise from an offshore transferor that does not have a favorable dividend WHT rate to an offshore transferee that has a favorable dividend WHT rate with China. Announcement 72 clarifies that the retained earnings of the PRC enterprise accumulated before the transfer are not entitled to any reduction in the dividend WHT rate even if the dividend is distributed after the equity transfer reorganization. This measure is designed to prevent any enjoyment of dividend WHT advantages for profits derived before a qualifying reorganization.

Share capital reductions are possible but difficult. As PRC corporate law only provides for one type of share capital, it is not possible to use instruments such as redeemable preference shares. Where a capital reduction was to be achieved and was to be financed with debt, in principle, it is possible to obtain a tax deduction for the interest.

Hybrids

Consideration may be given to hybrid financing, that is, using instruments treated as equity for accounts purposes in the hands of one party and as debt (giving rise to tax-deductible interest) in the other. In light of the BEPS Action Plan on hybrid mismatch arrangements, this may become more difficult in the future. There are currently no specific rules or regulations that distinguish between complex equity and debt interest for tax purposes under PRC tax regulations. Generally, the definitions of share capital and dividends for tax purposes follow their corporate law definition, although re-characterization using the GAAR in avoidance cases is conceivable. In practice, hybrids are difficult to implement in the PRC, particularly in a cross-border context. China’s restrictive legal framework does not provide for the creation of innovative financial instruments that straddle the line between debt and equity.

Other considerations

Company law

The PRC company law prescribes how the PRC companies may be formed, operated, reorganized and dissolved.

One important feature of the law concerns the ability to pay dividends. A PRC company is only allowed to distribute dividends to its shareholders after it has satisfied the following requirements:

- The registered capital has been fully paid-up in accordance with the articles of association.

- The company has made profits under PRC GAAP (i.e. after using the accumulated tax losses from prior years, if any).

- CIT has been paid by the company, or the company is in a tax exemption period.

- The statutory after-tax reserve funds (e.g. general reserve fund, enterprise development fund and staff benefit and welfare fund) have been provided.

For corporate groups, this means the reserves retained by each company, rather than group reserves at the consolidated level. Regardless of whether acquisition or merger accounting is adopted in the group accounts, the ability to distribute the pre-acquisition profits of the acquired company may be restricted, depending on the profit position of each company.

Where M&A transactions are undertaken, the MOFCOM rules in Provisions on the Acquisition of Domestic Enterprises by Foreign Investors (revised), issued in 2009, should be considered. Also bear in mind the national security review regulations issued by MOFCOM in March 2011 and affecting foreign investment in sectors deemed important to national security. The consent of other authorities, such as State Administrations of Industry and Commerce, and specific sector regulators, such as the China Securities Regulatory Commission, may also be needed.

Group relief/consolidation

There are currently no group relief or tax-consolidation regulations in the PRC.

Transfer pricing

Where an intercompany transaction occurs between the purchaser and the target following an acquisition, failure to conform to the arm’s length principle might give rise to transfer pricing issues in the PRC. Under the PRC transfer pricing rules, the PRC tax authorities are empowered to make tax adjustments within 10 years of the year during which the transactions took place and recover any underpaid PRC taxes. These regulations are increasingly rigorously enforced.

Dual residency

There are currently no dual residency regulations in the PRC.

Foreign investments of a local target company

The PRC CFC legislation is designed to prevent PRC companies from accumulating profits offshore in low-tax countries. Under the CFC rule, where a PRC resident enterprise by itself, or together with individual PRC residents, controls an enterprise that is established in a foreign country or region where the effective tax burden is lower than 50 percent of the standard CIT rate of 25 percent (i.e. 12.5 percent) and the foreign enterprise does not distribute its profits or reduces the distribution of its profits for reasons other than reasonable operational needs, the portion of the profits attributable to the PRC resident enterprise has to be included in its taxable income for the current period. Where exemption conditions under the rules are met, the CFC rules do not apply.

Comparison of asset and share purchases

Advantages of asset purchases

- Purchase price may be depreciated or amortized for tax purposes and buyer gains a step-up in the tax basis of assets.

- Purchaser usually does not inherit previous liabilities of the company.

- No acquisition of a historical tax liability on retained earnings.

- Possible for the purchaser to acquire part of a business only.

- Deduction for trading stock acquired.

- Profitable operations can be absorbed by a loss-making company if the loss-making company is used as the acquirer.

- May be easier to obtain financing from a regulatory perspective.

Disadvantages of asset purchases

- Purchaser needs to renegotiate the supply, employment and technology agreements.

- Government licenses pertaining to the vendor are not transferable.

- May be unattractive to the vendor (high transfer tax costs to the vendor if the value of the assets has appreciated substantially), increasing the price.

- It may be time-consuming and costly to transfer assets.

- Accounting profits and thus the ability to distribute profits of the acquired business may be affected by the creation of acquisition goodwill.

- Benefit of any losses incurred by the target company remains with the vendor.

Advantages of share purchases

- Purchaser may benefit from existing government licenses, supply contracts and technology contracts held by the target company.

- The transaction may be easier and take less time to complete.

- Typically less transactional tax arises.

- Lower outlay (purchase of net assets only).

Disadvantages of share purchases

- Purchaser is liable for any claims or previous liabilities of the target company.

- More difficult regulatory environment for financing equity acquisitions.

- No deduction for purchase price and no step-up in cost base of underlying assets of the company.

- Latent tax exposures for purchaser (unrealized gains on assets).

Stay up to date with M&A news!

Subscribe to our newsletter