By Neal Ransome – PricewaterhouseCoopers

M&A remains robust

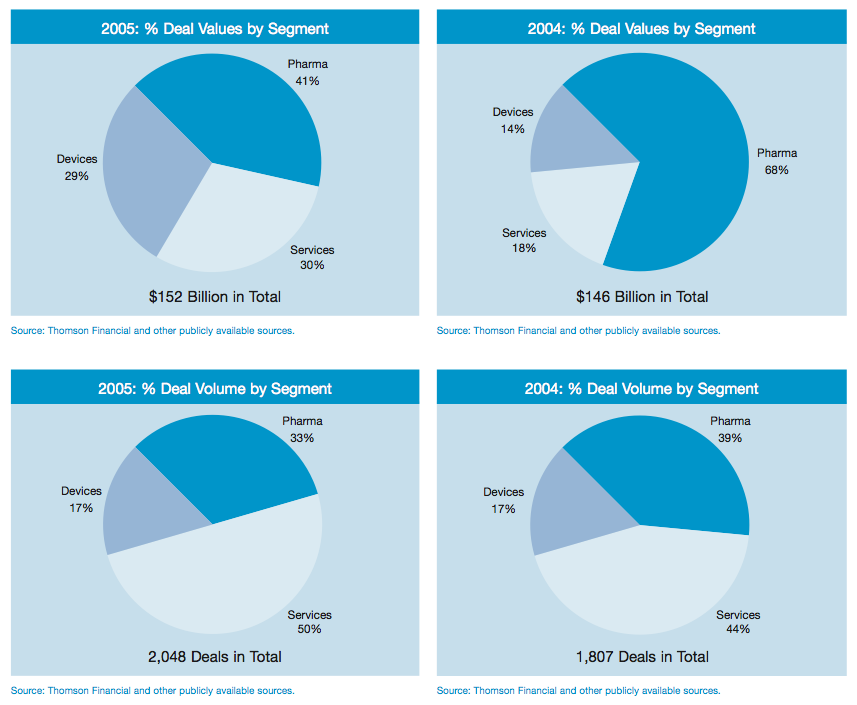

M&A activity in the pharmaceutical and healthcare sector remained buoyant during 2005 with the completion of 2,048 transactions totalling $152bn.

This tally – which encompasses deals worldwide in the pharmaceuticals, medical devices and healthcare services segments – compares with 1,807 transactions worth a combined $146bn in 2004.

The top-end of the market was particularly active with 28 deals valued at $1bn-plus. This compares with 25 in 2004 and just ten in 2003.

Pharmaceuticals

Participants in the pharmaceuticals segment engaged in a hectic round of corporate activity in 2005. The year got off to a lively start with three of the six largest deals announced in the first quarter. This brought the aggregate value of pharmaceuticals deals for the first three months of 2005 to $17.6bn – ten times the value that had been achieved by the end of March 2004.

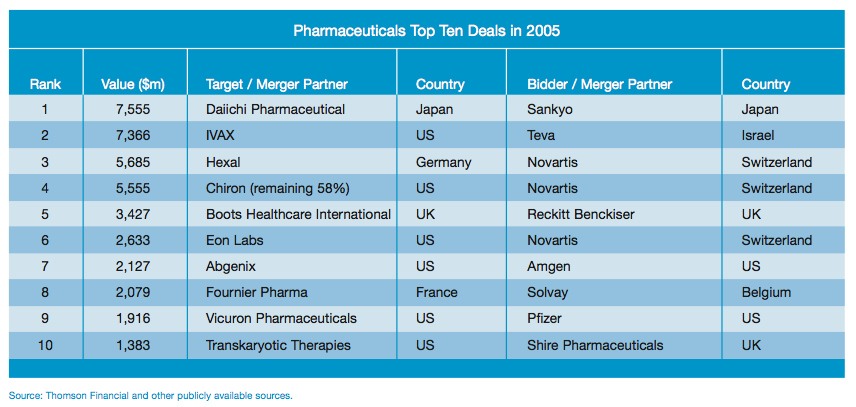

Overall, 684 pharmaceuticals deals worth an aggregate $61bn were completed in 2005. This compares with 703 totalling $100bn in 2004 (including the $60bn Sanofi/Aventis mega-merger).

Three of the largest pharmaceuticals deals last year were in the generics sub-sector – Teva/IVAX, Novartis/Hexal and Novartis/Eon Labs. Two top ten transactions were plain vanilla pharmaceutical combinations – Daiichi/Sankyo and Solvay/Fournier; while two involved pharmaceutical giants buying-up biotechs – Novartis/Chiron and Pfizer/Vicuron Pharmaceutical.

Last year also saw two major biotech-biotech acquisitions – Amgen/Abgenix and Shire/TKT; with one big, brand-driven OTC deal – Reckitt Benckiser/Boots Healthcare International – completing the picture.

Generics come under pressure

The generics sub-segment was highly active last year. Landmark deals included the $7.4bn acquisition by Israel’s Teva Pharmaceutical Industries of IVAX Corporation in the US alongside Novartis’ acquisitions of Eon Labs in the US and Hexal in Germany.

Eon Labs and Hexal, together worth some $8.3bn, are being integrated into Novartis’ Sandoz subsidiary. Outside the top ten, other significant generics deals included the acquisitions by Iceland’s Actavis of the human generics business of Alpharma and Amide Pharmaceutical in the US, for $810m and $600m respectively.

While Novartis’ acquisitions propelled it into the number 1 slot supplanting Teva as the world’s largest generics player, Teva’s subsequent purchase of IVAX enabled it to regain its pre-eminent position. Teva now has a bigger number of scripts written in the US than any other company.

Such leapfrogging is evidence of the increasing competition in the sector which last year saw an average price fall of 3% for generic prescription drugs against a 10% rise for brand name drugs. With ageing populations, governments are increasingly looking to cut drug expenditure. This is leading to growing pricing pressures on manufacturers and decreasing margins.

Size, and hence scope for economies of scale, is therefore becoming ever more important. All the announcements of major generics deals in 2005 included an assessment of the cost savings that could be achieved.

The global goal

Another key feature of the generics sector is the desire for global reach. Historically, many of the larger players have only been regional contenders. A prime attribute of several major deals in 2005 was that they extended the acquiror’s international coverage.

Teva’s acquisition of IVAX, for example, was fuelled partly by the two companies’ complementary geographic locations. Teva is strong primarily in the US and Western Europe, whereas IVAX’s main focus is Latin America, Central and Eastern Europe.

Outlook

We anticipate further consolidation within the generics sector.

In particular, several large generic companies remain primarily US-centric. We expect at least one of these to take steps to extend beyond the US.

We also anticipate that some of the emerging generic companies will continue to grow by acquisition. Actavis is an exciting example of a company that has recently grown rapidly by acquisition. Indeed 2006 has already seen further consolidation of the sector with Actavis being particularly active. Following on from its 2005 acquisitions it has acquired the Romanian Sindan and made a bid for Croatian Pliva.

Lastly, watch out for bids and deals initiated by some of the larger Indian generics companies as they begin to leverage off their low cost manufacturing bases.

Dr Reddy’s has already started this trend in 2006 with one of the biggest overseas acquisitions by an Indian pharma company. The $572m acquisition of German generics company Betapharm provides Dr Reddy’s with an increased presence in the world’s second largest generics market as well as a platform to sell existing Dr Reddy’s products into the European market. Betapharm has no manufacturing base and Dr Reddy’s will manufacture in India and utilise Betapharm’s existing supply chain.

Europe’s middle market

A continuing M&A theme is the likelihood of further consolidation within Europe’s middle market. A good example of this trend last year was the $2bn acquisition by Belgium’s Solvay of France’s Fournier Pharmaceuticals.

The deal gives Solvay ownership of Fournier’s market-leading fenofibrate product Lipanthyl, making the cardio-metabolic area Solvay’s largest franchise.

More recently, the announcement of Bayer’s $19.7bn acquisition of Schering gives a boost to Bayer’s pharmaceutical business and the combined business will be the world’s biggest seller of contraceptives; it also reasserts the importance of Germany as a pharmaceutical industry base.

Japan squares up to the competition

Following on from a highly active 2004 – which saw Yamanouchi and Fujisawa Pharmaceutical combine to form Astellas Pharma – Japan produced the biggest deal within the pharmaceutical segment last year with the $7.6bn merger of Sankyo and Daiichi Pharmaceutical.

The resultant Daiichi-Sankyo is now Japan’s second largest pharmaceutical company, after Takeda.

On top of the pressures facing the global pharmaceutical industry as a whole – such as rising R&D costs and the generics threat, the formation of Daiichi-Sankyo is a response to continuing competition in Japan from western drug companies. They are increasingly looking to sell directly into the Japanese market instead of via licensing agreements with domestic players.

US is top target

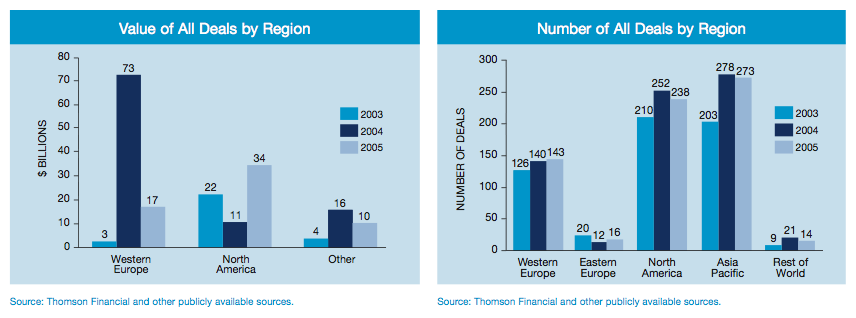

Within the pharmaceutical sector M&A volumes remained high in all markets last year. Deal values grew significantly in North America to $34bn from just $11bn in 2004, including seven $1bn-plus pharma deals totalling $23bn.

At the top end of the scale, the US was a net seller last year. Six of the top ten pharmaceutical targets were US-based whereas only two involved US bidders. This contrasts with the previous year when five of the top ten deals were led by North American acquirors and only three had US targets.

Western Europe also saw relatively high volumes of M&A activity with deals totalling $17bn overall (2004 – $13bn, excluding the $60bn Sanofi-Aventis combination). The two largest deals in western Europe last year were Novartis/Hexal and Reckitt Benckiser/Boots Healthcare.

Biotechnology

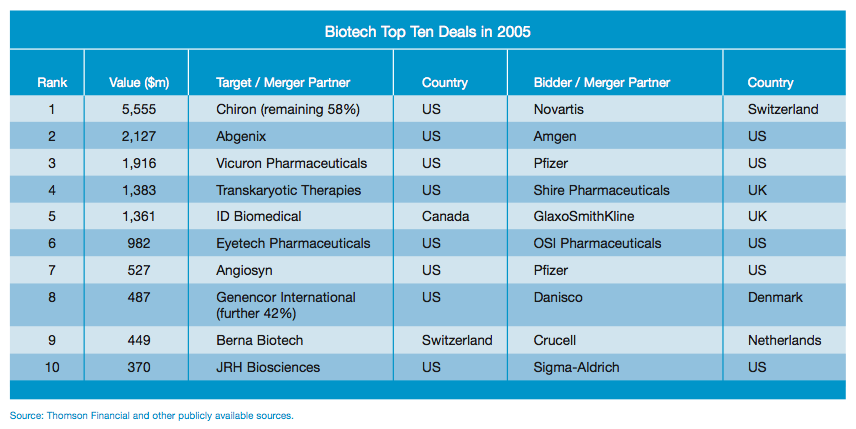

Biotechnology deals were generally larger in 2005 than in the previous year. Hence, the total value of the top ten deals in 2005 reached $15bn compared to just $7bn in 2004.

North America continued to dominate the segment with nine of the ten largest biotech deals involving North American targets. Due partly to the relative maturity and large size of US biotechs, leading pharmaceutical companies are now more frequently seeking to stake a claim on the industry through outright ownership rather than partnerships.

The biggest biotech deal in 2005 was the $5.6bn takeover by Switzerland’s Novartis of an outstanding 58% stake in Chiron in the US. Chiron ranks fifth in the global vaccines market, but suffered manufacturing problems at two of its European plants in 2004.

Novartis’ decision to take full control of Chiron should enable it to protect its original investment by resolving production issues and gain it a major foothold in the increasingly important vaccines market. Fuelled by factors such as concerns over a possible avian ‘flu pandemic, the vaccines market was undoubtedly the biotech ‘hot-spot’ in 2005.

Two other major deals in the biotech top ten last year involved vaccines companies. GlaxoSmithKline acquired the Canadian vaccine company ID Biomedical for $1.4bn. ID Biomedical is a leading manufacturer of ‘flu vaccines and is developing a number of vaccines for other illnesses such as pneumonia.

In addition, the Swiss vaccine company Berna Biotech was acquired by the Dutch company Crucell for $449m (after Novartis opted not to launch a bid). Berna, which develops travel vaccines for conditions such as Hepatitis B, complements Crucell’s activities in tropical diseases.

Eye diseases also attracted a disproportionate amount of M&A activity. OSI Pharmaceuticals acquired Eyetech Pharmaceuticals for $982m. Eyetech’s flagship product is Macugen, a treatment for age-related macular degeneration. The deal created a third leg for OSI in eye disease alongside its existing expertise in oncology and diabetes.

A second major deal in the eye disease therapeutic area was Pfizer’s $527m acquisition of Angiosyn in the US. Angiosyn is developing an angiostatic agent to treat ophthalmic diseases.

Big pharma catches the biotech bug

In last year’s Insights we commented on the high number of deals in the biotech top ten led by ‘big biotechs’. We noted that many of the big pharmaceutical companies remained wary of making outright biotech acquisitions, preferring to enter into licensing deals or strategic alliances.

This year, however, it is noticeable that a number of the largest biotech acquisitions have been made by the largest pharmaceutical giants, notably Pfizer, GlaxoSmithkline and Novartis.

Big pharmaceutical R&D ‘pipelines’ are, generally, at a low ebb – in 2005 the number of drugs obtaining FDA approval was 40% below the equivalent figure for 2004. There is no doubt that shortages in this pipeline are prompting some of the big players to construct deals with biotech companies which deliver them total control.

A number of deals announced last year followed on from earlier joint ventures between acquiror and target. Both the $2.1bn acquisition by biotech giant Amgen of the antibody research group Abgenix and Pfizer’s $1.9bn takeover of Vicuron Pharmaceuticals, which is focused on developing anti-infection drugs, were founded upon earlier drug development collaborations. Such collaborations enable companies to establish whether they represent a good match before taking the ultimate step of outright acquisition.

Bio-pharmaceutical rationale

Further acquisitions of biotech players by big pharmaceutical companies are likely to be predicated on the synergies which can spring from the technical expertise of the biotechs combined with the sales and marketing capabilities of the pharmaceutical giants.

If productivity in new drug development continues to decline, coupled with increasing sales and marketing costs, continued pressure on public health budgets and strong competition from generics manufacturers, then we can expect to see further consolidation in the big pharma sector.

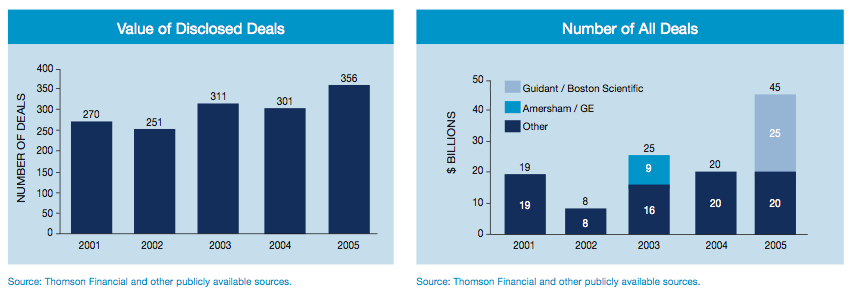

Medical Devices

The biggest M&A story in the medical device sector in 2005, and indeed in 2004, was the battle for control of US-based Guidant.

Johnson & Johnson announced a planned takeover of Guidant in late 2004 (as included in our analysis for 2004). However, Boston Scientific made a $25bn counter-bid. We have adjusted our 2004 figures accordingly and included the Boston Scientific offer in the 2005 statistics.

The Guidant deal dwarfs all other deals in the medical devices sector. Excluding this deal, the value of deals in the sector in both 2004 and 2005 was stable at $20bn.

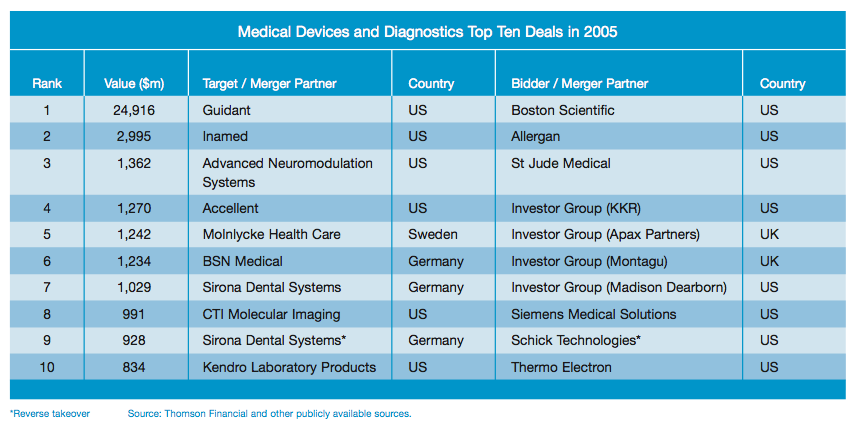

Guidant aside, the largest M&A transaction in the segment in 2005 was Allergan’s $3bn acquisition of Inamed. This, too, was contested hotly with Inamed initially the subject of a $2.5bn offer from Medicis Pharmaceutical.

The strategic logic of the Allergan/Inamed combination is compelling. Allergan produces Botox while Inamed manufactures products such as breast implants and devices to treat obesity. The acquisition represents Allergan’s first move into the medical devices sector.

Private equity prescription

We predicted in last year’s Insights that there would be increased private equity (PE) interest in the medical devices sector and this has indeed proved to be the case.

In 2005 four of the top ten deals in the sector were led by PE firms. Two of these involved European woundcare companies, namely the acquisitions of Sweden’s Molnlycke Health Care by Apax Capital Partners and of BSN Medical in Germany by Montagu Private Equity. Woundcare represents an attractive sector for PE investors not least because it is a non-invasive part of the medical devices sector. We expect to see further PE activity in this area during 2006.

Another medical devices sub-sector which has recently attracted a high degree of PE interest is dental equipment. One company, Germany’s Sirona Dental Systems, features twice in our list of the ten largest medical devices deals of 2005. Sirona has had three consecutive PE owners in recent years – Permira, EQT and, as a result of a further buyout in 2005, Madison Dearborn Partners. Soon after its latest MBO Sirona acquired Schick Technologies, a US-quoted designer of digital radiographic imaging systems for the dental sector. This $1.9bn reverse takeover gave Sirona’s backers 67% of the enlarged group.

As we progress into 2006 medical devices continues to be an active sector for PE, as evidenced by EQT and Investor AB’s recently announced $5bn bid for the Swedish company Gambro. Gambro is a market leading company in the areas of dialysis, intensive care, blood bank technology and therapeutics.

Fund Raising

The climate for IPOs in 2005 was similar to that experienced in 2004. Although the market was technically ‘open’ for new entrants, the process of actually getting new companies onto the world’s public markets remained tough.

Pharmaceutical and healthcare IPOs raised $6bn in 2005 compared with $7bn the previous year. It seems that many potential investors remain cautious having seen the substantial losses made on several previous biotech floats, particularly in the genomics area, after the IPO boom of 2000.

In addition, given the strong appetite for acquisitions on the part of the big pharmaceutical companies, the owners of many privately-owned biotech companies are favouring trade sales over IPOs as their preferred form of exit.

Public markets – mixed message

As in 2004, the success of last year’s stockmarket debutantes was mixed.

A number of companies were forced to list at the bottom end of their value ranges and several had to pull their floats altogether. At the end of the year a significant proportion of new entrants were trading below their listing prices.

Significant pharmaceutical and healthcare IPOs in 2005 included the Italian eyewear company Safilo; the French pharmaceuticals business IPSEN; and Spain’s leading cosmetic surgery company Corporación Dermoestética. For the first time for several years there were more IPOs in the sector in Europe (22) than in the US (17).

The market for follow-on finance remained strong, with quoted companies in the sector raising a further $20bn compared with $17.5bn in 2004.

Private Equity – drawn to devices

PE interest in the pharmaceutical and healthcare industry remained constant last year with $11bn of new money invested compared with $12bn in 2004.

As indicated previously, many of the largest PE deals were in the medical devices sector. These included KKR’s $1.3bn acquisition of Accellent, Apax’s acquisition of Molnlycke Health Care, Montagu Private Equity’s acquisition of BSN Medical and Madison Dearborn’s investment in Sirona.

In the biotechnology sector, PE funding is increasingly being supplemented by the proceeds of partnering arrangements with the big pharmaceutical companies. Industry sources estimate that in 2005 approximately $17bn was committed to biotech companies under such corporate venturing schemes.

Outlook for 2006

We expect the public markets to remain active in 2006. However, we anticipate that the proportion of emerging biotech companies that make it to the public markets will be exceeded by the proportion acquired by bigger companies before they float.

The weight of money flowing into PE funds continues to grow, and inevitably this will mean a continued increase in the proportion of deals done by PE houses. Over time this will drive up the prices paid for deals in those areas of the overall pharmaceutical and healthcare market which are attractive to PE (such as healthcare services and medical devices), encouraging other investors to focus on areas such as pure pharma which carry greater R&D risk.

Stay up to date with M&A news!

Subscribe to our newsletter