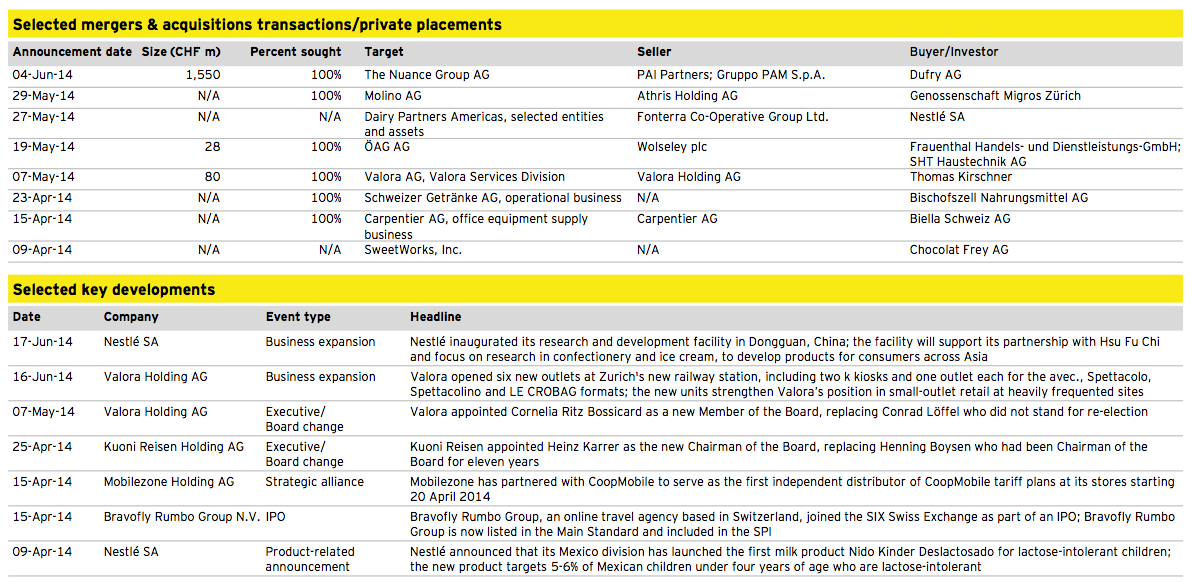

After a year of subdued performance in 2013, the Swiss M&A market recorded an exceptional first half year 2014. A particular highlight was that disclosed deal volume reached a new record in Q2 2014 with the highest volume since the Swiss M&A Quarterly was introduced in 2008. This was mainly attributable to several large announced M&A transactions.

Furthermore, as M&A market conditions in Switzerland remained favorable, the number of M&A transactions with Swiss involvement continued to increase in the second quarter of 2014, confirming the expected upward trend in M&A activity. Looking forward, there are multiple indications that the positive development will continue in the second half of this year.

Swiss M&A market Q2 2014 and outlook 2014

M&A market Q2 2014

► After two consecutive quarters with a declining number of deals, the Swiss M&A market recorded 154 transactions in Q2 2014, translating into an increase of 21% compared to Q1 2014 and 10% against Q2 last year, respectively.

► In addition, M&A transactions with Swiss involvement reached a record deal volume of CHF 82.1b in Q2 2014 compared to CHF 20.0b in the previous quarter. Thus, Q2 2014 volume totaled nearly four times the deal volume of 2013 and represents the highest volume ever recorded since inception of the Swiss M&A Quarterly in 2008.

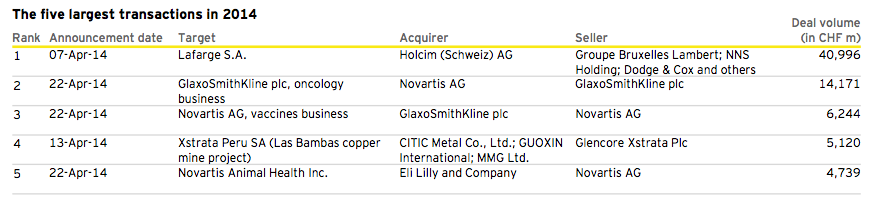

► Deal volume was mainly driven by several mega deals. Notably, all of the five largest transactions in the first half of this year were recorded in the second quarter of 2014 and accounted for ~87% of the total transaction volume in this quarter.

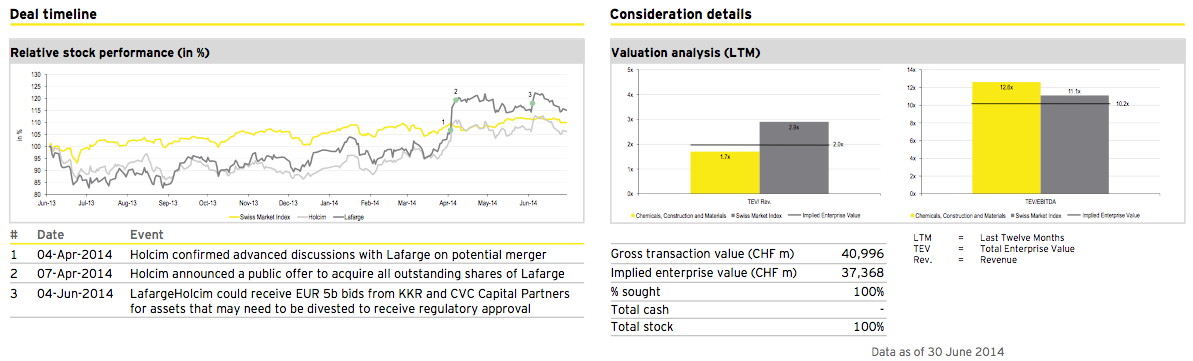

► The largest deal was the merger between Lafarge and Holcim for ~CHF 41.0b. In addition, Novartis was involved in three of the top five deals, totaling a transaction volume of ~CHF 25.2b.

► In line with the increased M&A activity, the SMI gained 11.3% over the last twelve months, rising 3.1 percentage points in the trailing 12-month period ended 31 March 2014.

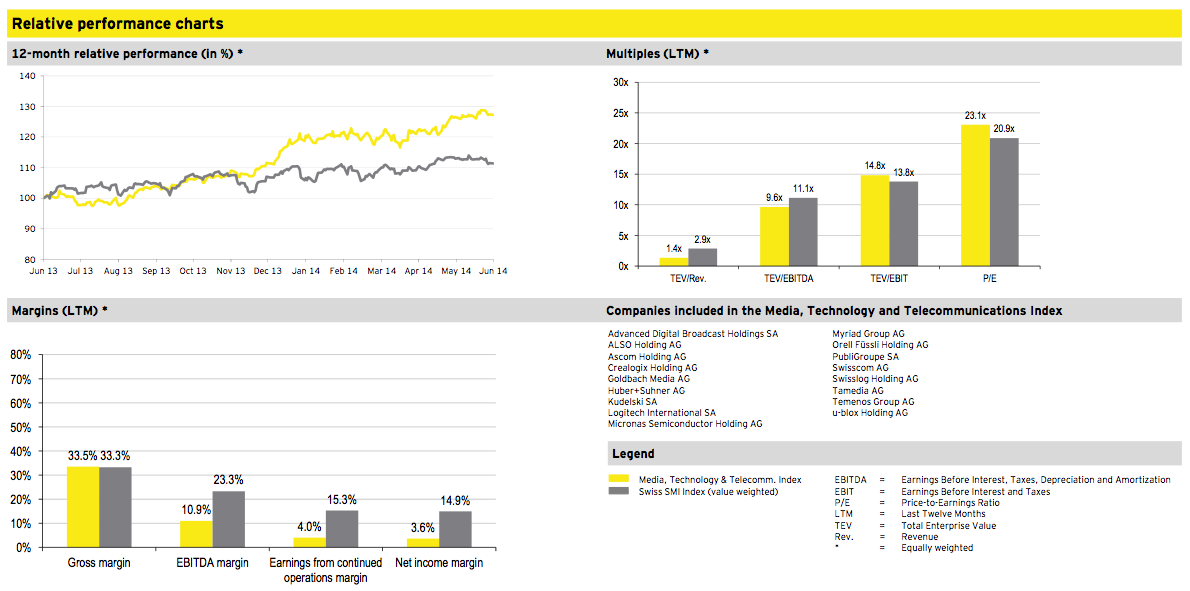

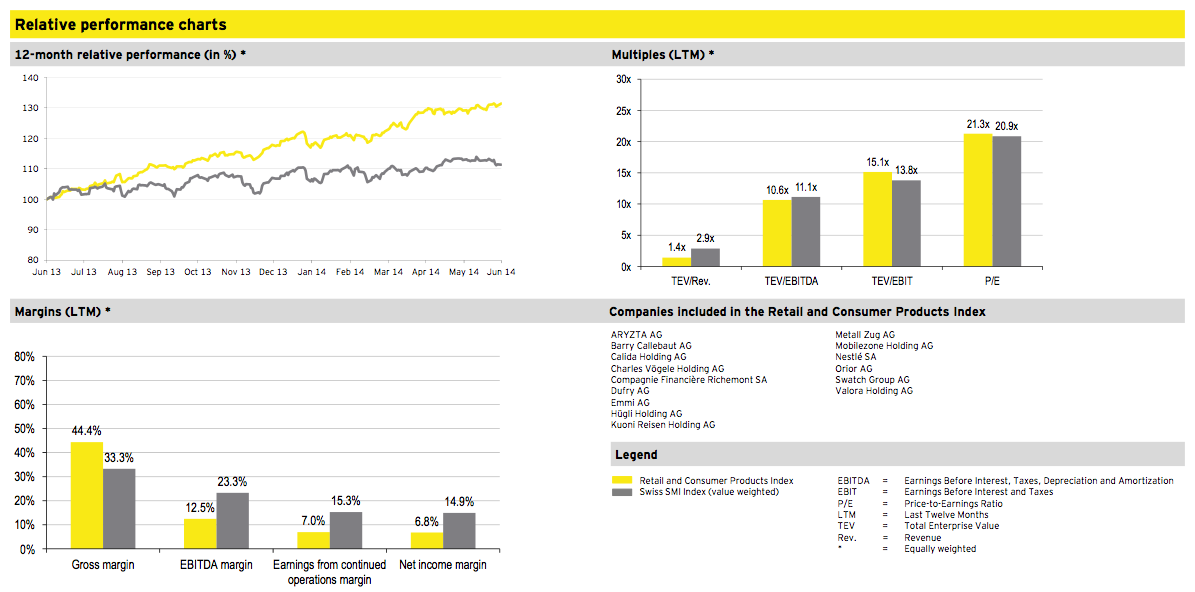

► Similarly to the previous quarter, nearly all of the equally weighted industry sectors outperformed the value weighted overall stock market index during the last twelve months. The Media, Technology and Telecommunication displayed the strongest industry performance with an improvement of 27.2% or approximately 2.4 times the SMI performance.

Transactions by industry

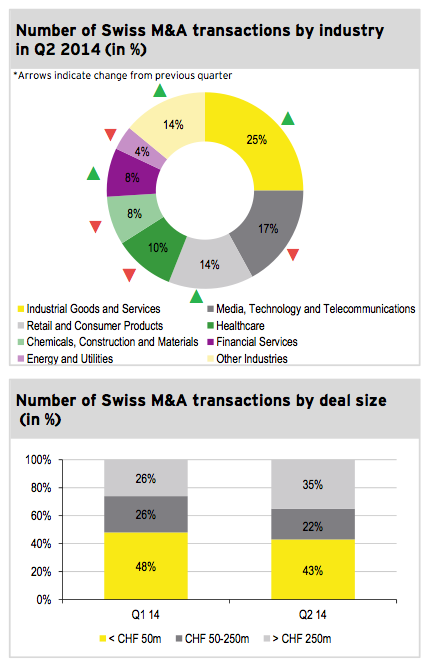

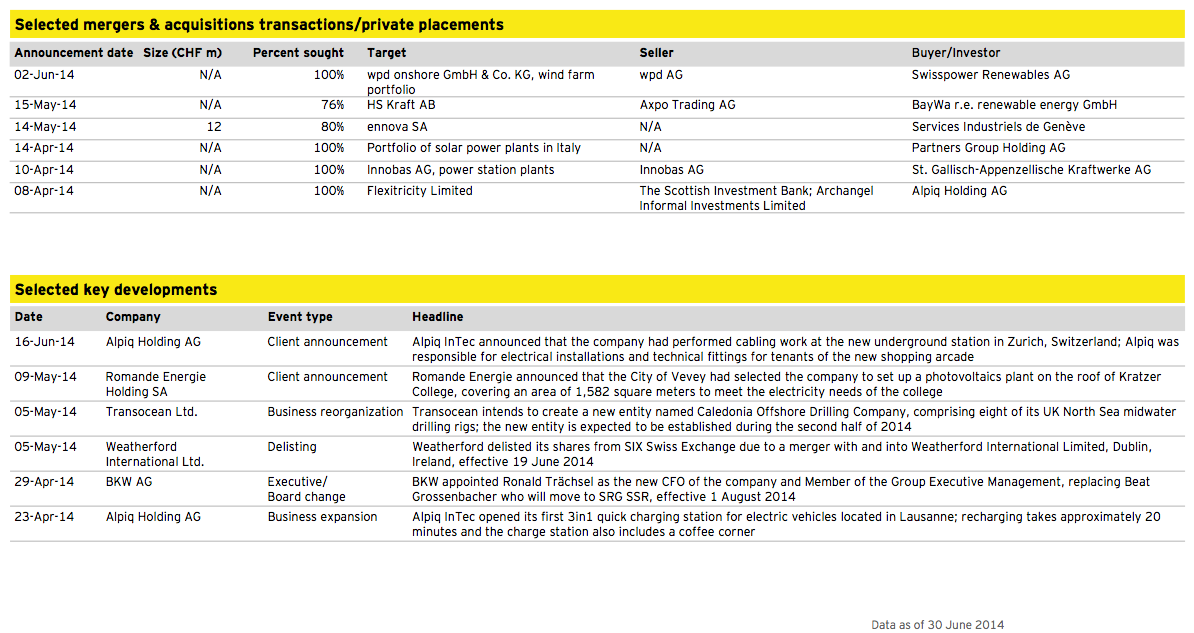

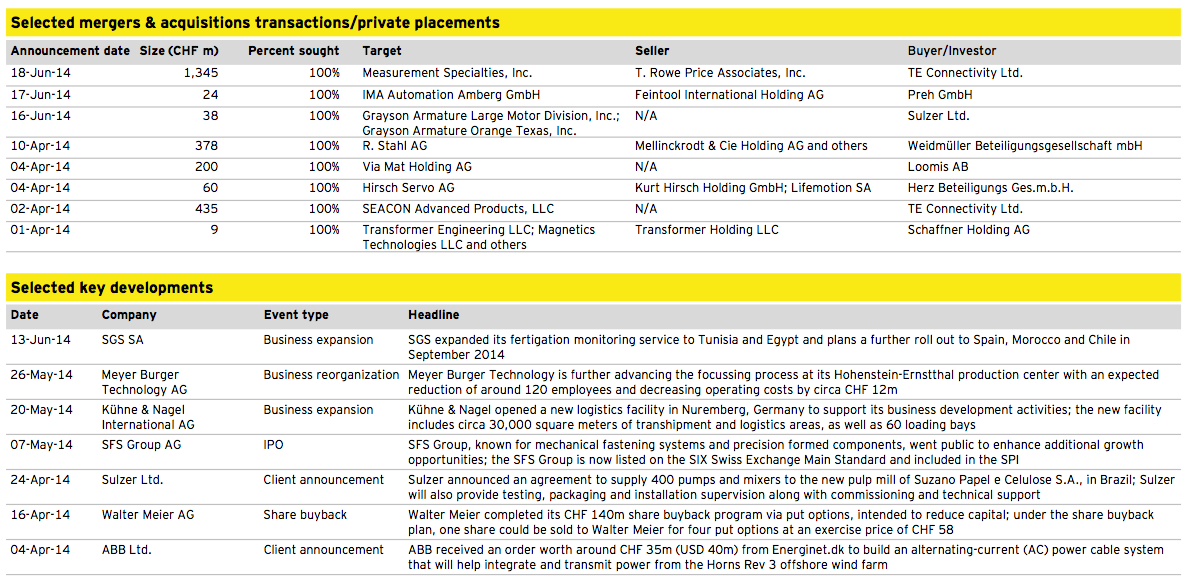

► For the third consecutive quarter, Industrial Goods and Services was the most active industry in Switzerland, contributing 38 transactions or 25% to the 154 announced Swiss M&A deals. The largest deal with disclosed deal volume stemming from the Industrial Goods and Services sector was the acquisition of US-based Measurement Specialties by Swiss-based TE Connectivity for ~CHF 1.3b.

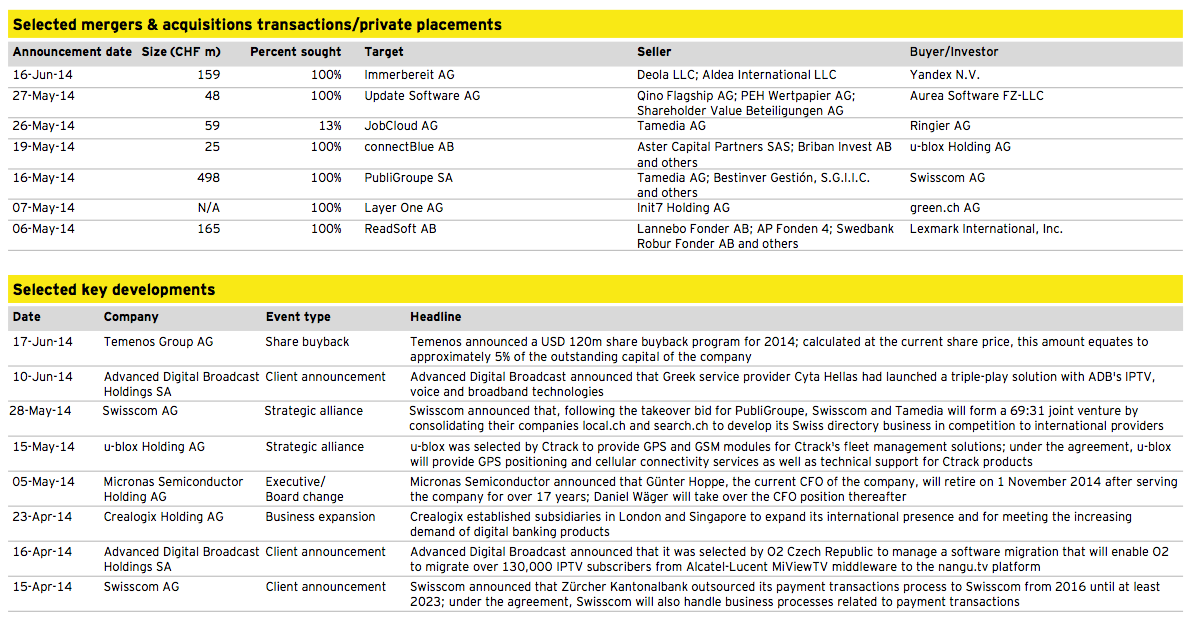

► Even though Media, Technology and Telecommunications accounted for 26 transactions and was the second most active industry in M&A, the sector recorded the largest decrease in deal activity with a decline of 4 percentage points compared to Q1 2014. On the other side, Retail and Consumer Products experienced the largest gain, with an increase of 6 percentage points compared to Q1 2014.

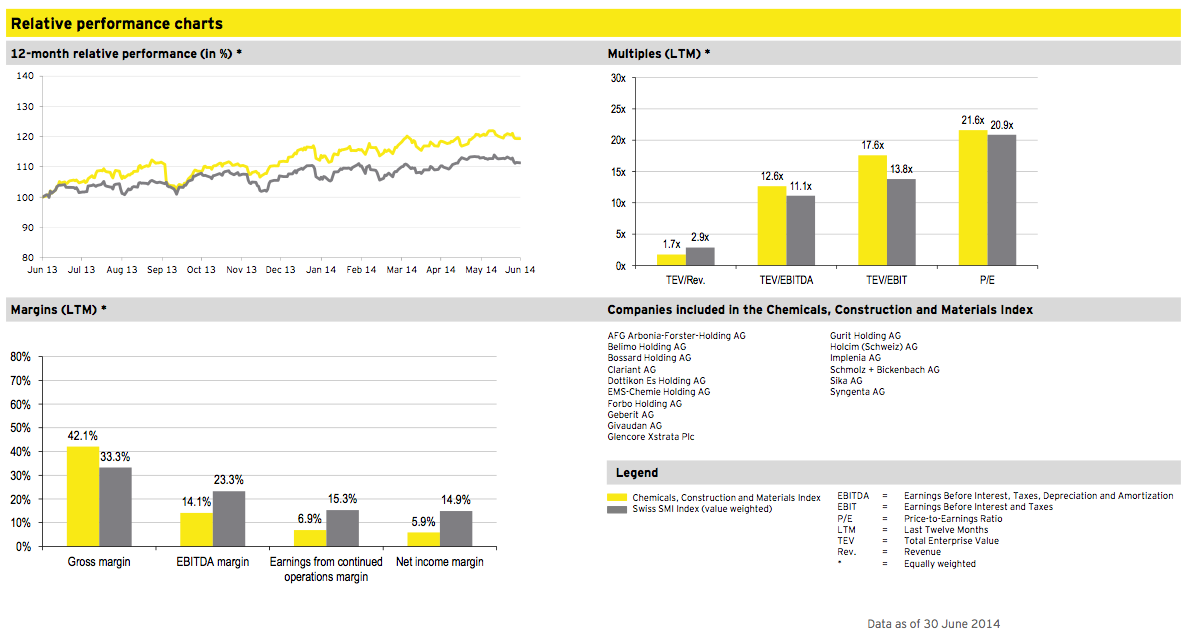

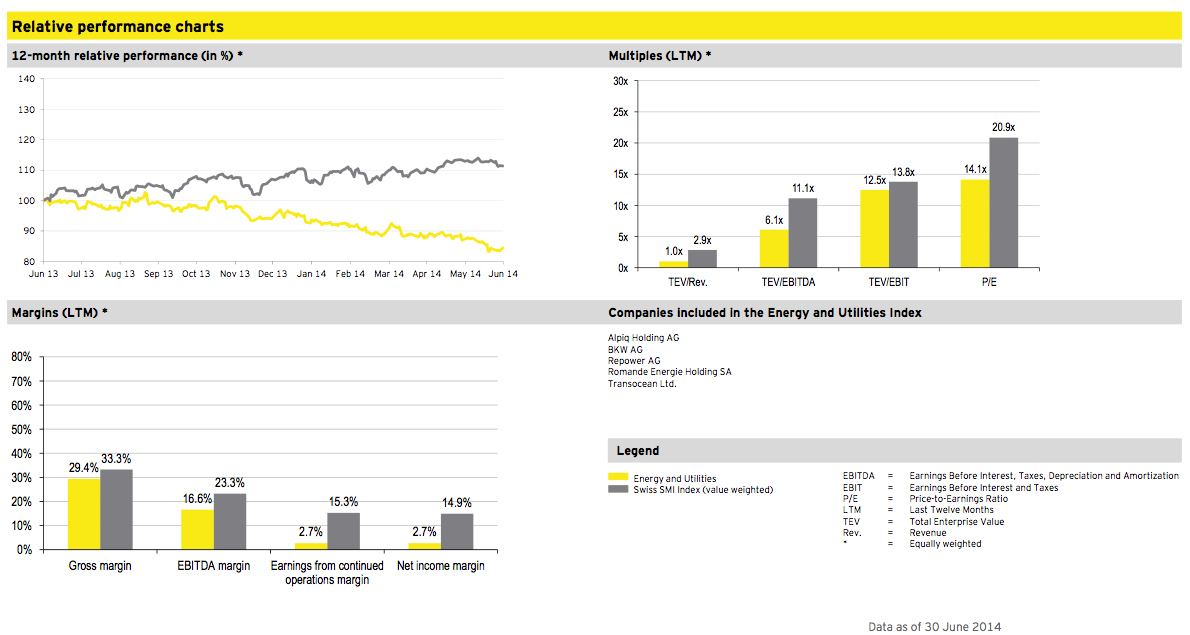

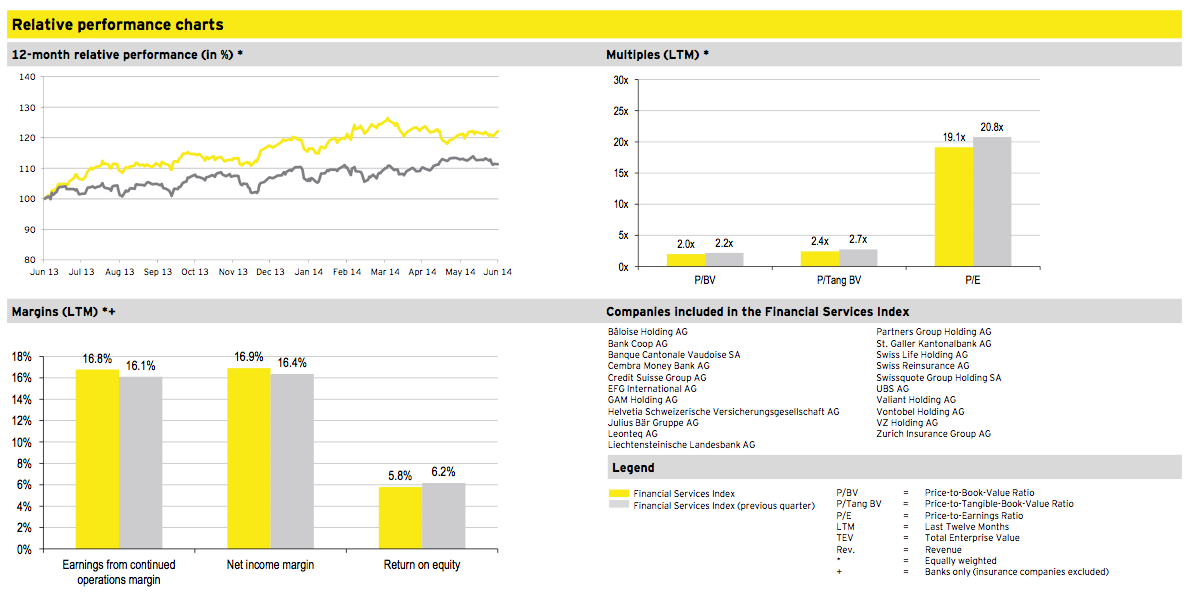

► The remaining sectors, Healthcare, Financial Services together with Chemicals, Construction and Materials were evenly distributed with market shares of between 8-10%, while Energy and Utilities saw the lowest number of transactions, accounting for just 4%.

Transactions by size

► The second quarter of 2014 was underpinned by a further increase in large transactions with deal size above CHF 250m. In total 17 Swiss M&A transactions or 35% of all announced deals were valued above CHF 250m, reflecting the highest contribution from this category in the last two years.

► In addition, apart from the two sectors Financial Services and Energy and Utilities, high-value transactions were observed across all industries depicted in the M&A Quarterly Switzerland.

► As in the first quarter of 2014, the share of Swiss deals with small transaction values below CHF 50m showed a decrease (from 48% to 43%), as did the mid-market deals between CHF 50-250m (from 26% to 22%).

► Deal size was disclosed in ~32% of all announced transactions in the second quarter of 2014.

Outlook 2014

► The latest economic forecast released by the Swiss State Secretariat of Economic Affairs (SECO) in June 2014 projects a reduction in GDP growth for 2014 from 2.2% (as published in March 2014) to 2.0%.

► The less optimistic outlook is mainly caused by a delayed increase in export growth, which in turn is based on expectations of a decelerating recovery of the world economy and the ongoing relative strength of the Swiss Franc.

► For 2015, SECO expects the economy to expand further, resulting in a GDP growth forecast of 2.6% (previously 2.7%).

► The latest edition of EY’s CFO Capital Confidence Barometer revealed that a majority of the responding CFOs (59%) assumes that the market for M&A deals will improve over the next twelve months. Although the majority of respondents is optimistic regarding M&A market activity, the sentiment among CFOs was less positive than in the previous survey conducted in October 2013 (67%).

► In addition, 28% of the responding CFOs expect their company to conduct an acquisition in the next twelve months, virtually the same percentage as recorded in the October 2013 edition.

► Overall, the outlook on Swiss M&A activity remains bright due to an unchanged favorable market environment encompassing positive growth prospects for the Swiss economy, a further recovery of the world economy, high optimism among executives, strong balance sheets including large cash reserves as well as low financing costs. Moreover, the current low interest rate environment makes it difficult for corporations to invest cash reserves at a reasonable rate of return or benefit from repayments of debt. Therefore, executing M&A transactions is an option that enables companies to generate shareholder value in the existing environment.

Private equity statistics: Germany, Switzerland and Austria

Private equity Q2 2014

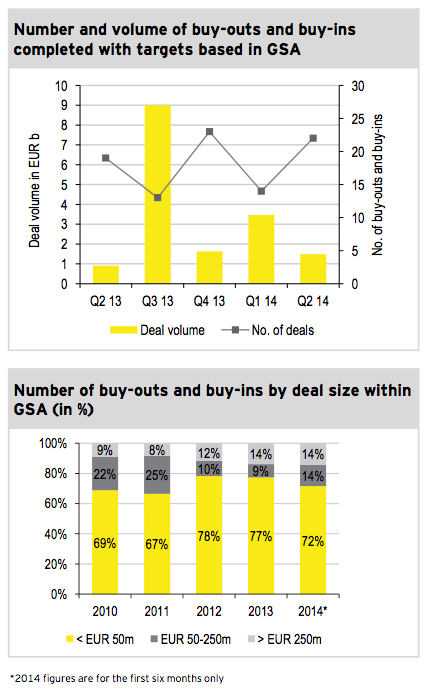

► In Q2 2014, 22 private equity (PE) deals were completed in Germany, Switzerland and Austria (GSA). This reflects an increase of eight deals compared to Q1 2014 and three deals compared to the same quarter of the previous year.

► This quarter’s 22 PE deals added up to a total volume of EUR 1.5b, indicating a decrease of 57% in deal volume compared to Q1 2014. In contrast, deal volume increased by 64% compared to the same quarter of the previous year.

► The increasing number of deals and decreasing deal volume meant that compared to the previous quarter, average deal size declined from EUR 247m in Q1 2014 to EUR 68m in Q2 2014. This is mainly attributable to a lack of large PE deals being completed. In Q1 2014, the largest deal was Hellmann & Friedmann’s acquisition of Scout 24 valued at EUR 2.0b, which also represents the amount by which overall deal volume decreased between Q1 and Q2 2014.

► In GSA, the largest PE deal completed in Q2 2014 was the exit of UK-based PE house Bridgepoint in German-based CABB GmbH for about EUR 800m or 54% of the deal volume recorded in Q2 2014. CABB GmbH, a global supplier of fine and specialty chemicals, was sold to UK-based PE firm Permira.

► In Q2 2014, the number of completed PE deals in GSA accounted for 14% of all deals in Europe. In terms of deal volume, transactions in GSA represented 13% of the European deal volume.

► While mid- and large-sized transactions combined made up half of all transactions in Q1 2014, the distribution of deals by size moved towards the long-term average over the course of Q2 2014, with the majority of deals being valued below EUR 50m. Nevertheless, the share of deals larger than EUR 50m is still higher in the current calendar year than it was in 2012 and 2013.

Energy and Utilities

Financial Services

Healthcare

Industrial Goods and Services

Media, Technology and Telecommunications

Retail and Consumer Products

Deal of the quarter

Transaction overview

Deal summary

On 7 April 2014, Holcim Ltd. and Lafarge S.A. announced plans to merge the two companies. The transaction is structured as a public exchange offer, initiated by Holcim with an exchange ratio of one Holcim share for one Lafarge share. The combined company, LafargeHolcim, will be based in Switzerland and listed on the SIX Swiss Exchange in Zurich and Euronext in Paris. The combined sales of the two entities amount to ~CHF 39b and EBITDA to ~CHF 8b. The transaction is expected to be closed in the first half of 2015, subject to regulatory approval which is expected to require divestments of 10% to 15% of the global EBITDA.

Based in France, Lafarge operates in the production and sale of building materials. The company employs 64,000 people in 62 countries and reported sales of ~EUR 15b in 2013.

Deal rationale

► LafargeHolcim is expected to have an enhanced presence in the global building materials sector, positioned in 90 countries around the world with balanced exposure to both developed and high growth markets.

► With an enlarged range of products and services, the combined company should be better placed to respond to the changing demands of the building materials industry and the challenges of increasing urbanization.

► Synergies are expected to total more than CHF 1.7b (EUR 1.4b) on a full run rate basis phased in over three years, with one third in year one, including scale and cross utilization of innovative products and solutions, financial savings and capital expenditure optimization.

Stay up to date with M&A news!

Subscribe to our newsletter