Americas Region. Americas Financial Advisory. August 2016

By Deloitte

Executive summary

Majority of M&A deals in Latin America during 2016 have been intra-regional. Industries such as financial services, consumer business, and energy and resources attracted many large investments in the region. Improving US markets may boost M&A in the region as it was the second largest investor during 2015-2016. However, weak oil and commodity prices may act as deterrents to M&A activity in the region.

M&A trends in Latin America

• Many of the Latin American countries are dependent on oil and other natural resources (iron ore and copper are two of the top exports for Brazil and Chile, and oil accounts for a large portion of Mexico’s and Colombia’s exports). Therefore, weak oil and commodity market have affected M&A activity in the region. Additionally, deal activities remain subdued due to weak economic growth in the region.

• M&A value dropped in 2015-2016 compared to 2014. However, the number of deals remained more or less the same indicating that there were many small value deals.

• As economic stability in the US improved in the first half of 2016, it is expected that this may result in more investments into the Latin American region.

Industries

• Tighter regulations in the region coupled with the role of technology in the financial services sector contributed to high M&A activity in the Financial Services Industry (FSI). FSI also recorded a high level of activity in cross-industry M&A deals.

• The middle class has grown rapidly in Latin America, driven in part by the commodity boom. The increase in buying power and discretionary spending helps drive M&A activity in consumer facing industries such as Consumer Business (CB), and Technology, Media, and Telecommunications (TMT).

Geographies

• The majority of M&A activity in the region is intra-regional, with bigger economies, such as Brazil and Mexico, being top investors in the region.

• North America (especially the United States) and Europe (countries such as Spain, the UK, and France) have led cross-border M&A activity in Latin America as companies from these mature economies look to invest in developing markets.

Challenges

• Despite improvements over the past decade, some of the major challenges in doing business in Latin America continue to include obtaining financing, tax law transparency, and enforcing contracts.

• In 2015, falling oil and metals prices, currency depreciation, and weak macroeconomic conditions impacted M&A activities in the region.

• Limited access to the financial system, overdependence on commodities, insufficient infrastructure, outdated customs procedures, corruption, non-tariff barriers, and inadequate intellectual property rights protection can also deter investors in certain Latin American countries and markets.

2015-2016 M&A snapshot

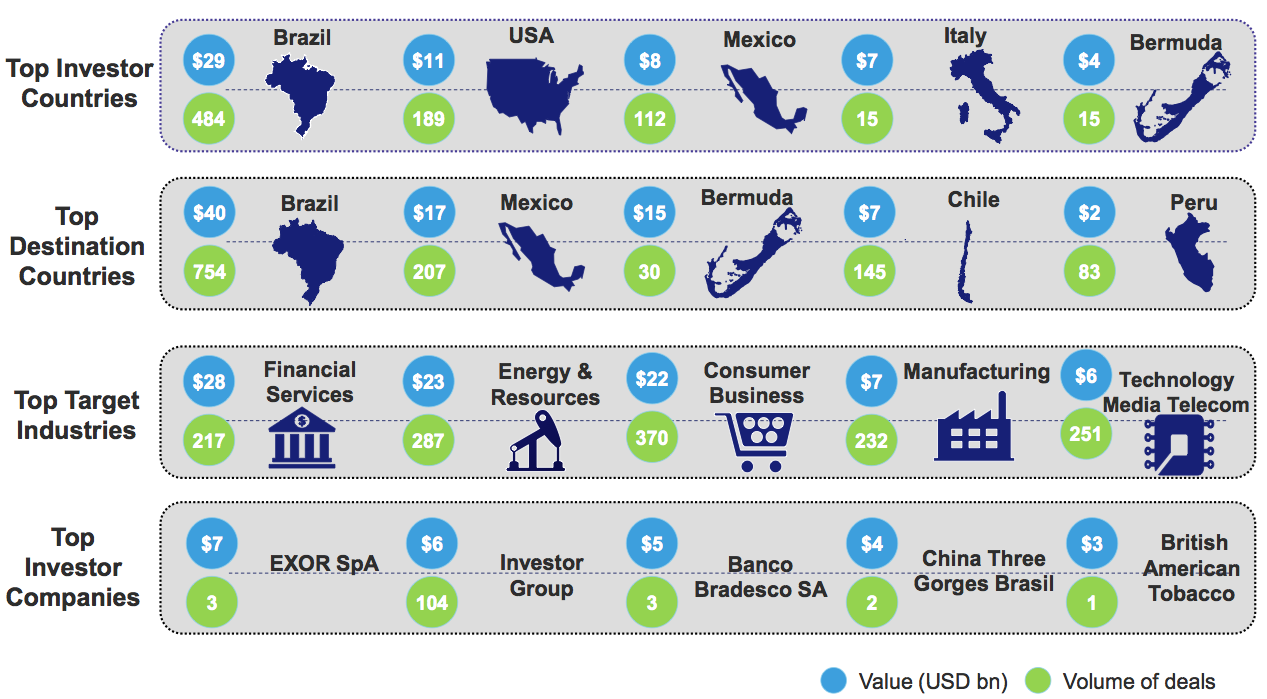

Latin America M&A deal in-flow totaled 1,621 deals worth USD 95.7 billion between January 1, 2015 – April 25, 2016

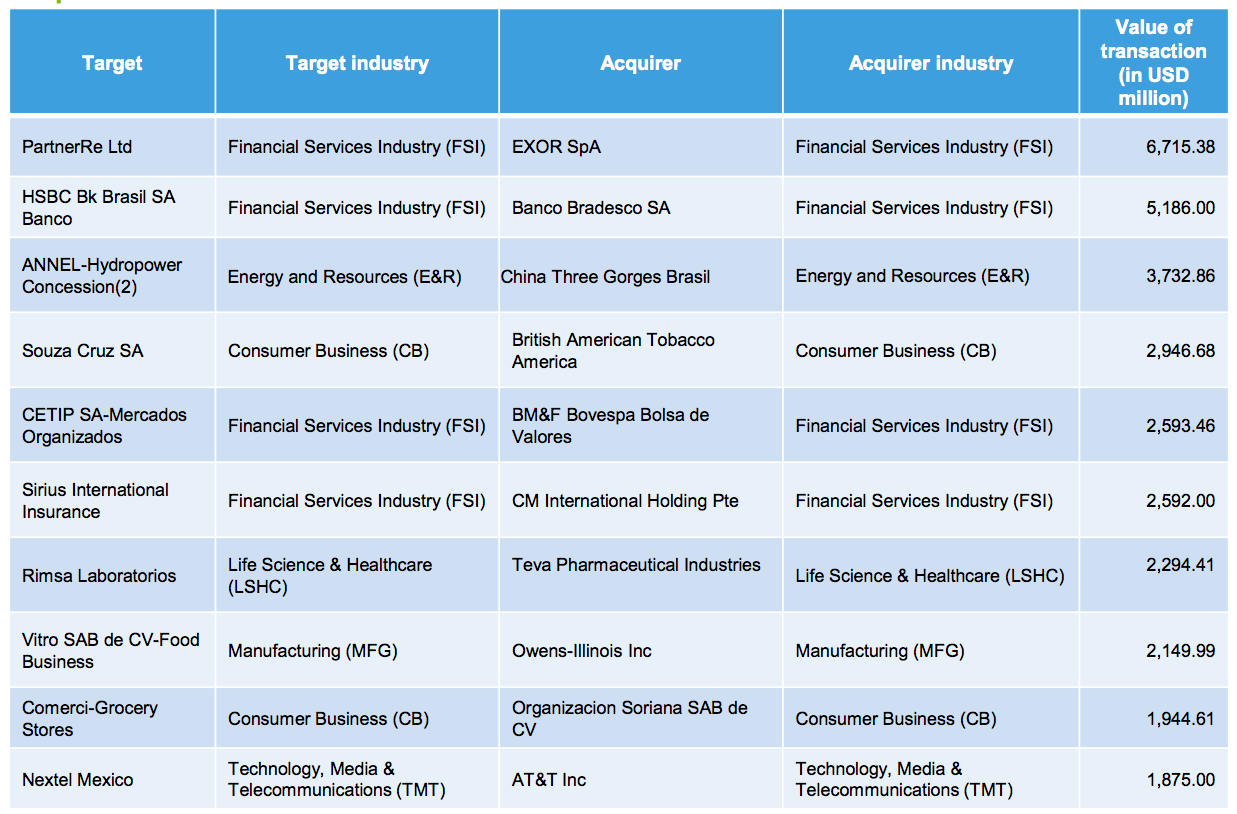

Top deals in 2015-2016

Macroeconomic indicators

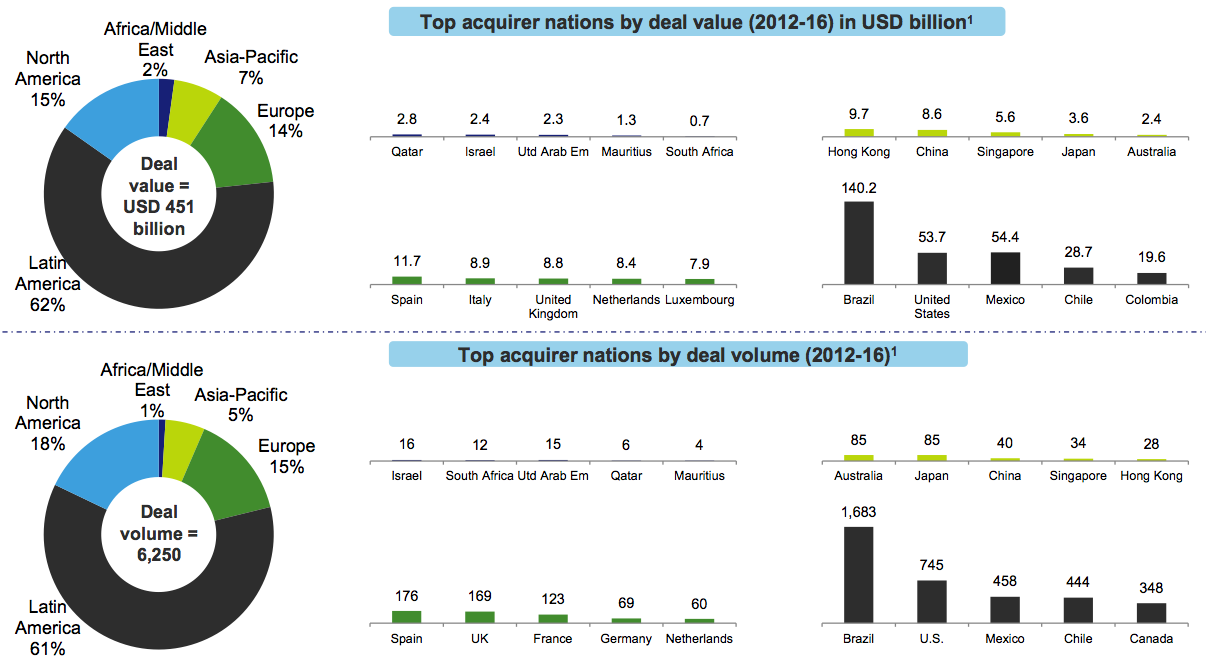

Geographical M&A activity

Intra-regional deals drove most M&A activity in the region: North America and Europe lead in inter-regional deals

Brazil’s political instability and weak macroeconomic fundamentals hampered investment activity in 2015 and 2016

Brazil’s increasing domestic demand, growth potential, and attractive asset prices resulting from currency depreciation contributed to M&A activities. However, a projected decline in GDP growth rate, perceived increased corruption, and political instability will likely dampen future investments.

M&A favorable factors

• The emerging middle class, propelled by increased income and the availability of credit, could boost aggregate demand, in turn driving M&A growth in consumer facing industries.

• Exchange rate between USD and BRL has fallen significantly in the last five years. (from 0.56 in 2012 to 0.25 in 2016 against 1 USD). This can help make Brazilian assets and companies more attractive for foreign investors.

• The Brazilian Central Bank is expected to reduce Selic policy interest rate to 12.5% from 14.15% by end-2017. Favorable credit terms could trigger intra-Brazilian deals.

• Government policy changes to attract foreign capital in Brazil-based health care providers and the upcoming Olympics in August 2016 could act as a positive catalyst for investments.

M&A unfavorable factors

• Corruption issues, such as the situation in the oil and gas sector, may not only impact investments in the sector, but could also impact infrastructure given the fall- out from the involvement of major construction companies.

• Political instability could also act as a deterrent for M&A activity as an interim government was constituted in May 2016.

• The Economist Intelligence Unit (EIU) also predicts that GDP is expected to fall by 3.7% in 2016 and revive slowly in 2017-2020.

• Many components of the services sector (which accounts for over 70 percent of GDP) may not recover in the medium term, as they can be impaired by low productivity, a tight labor market, and skill shortages.

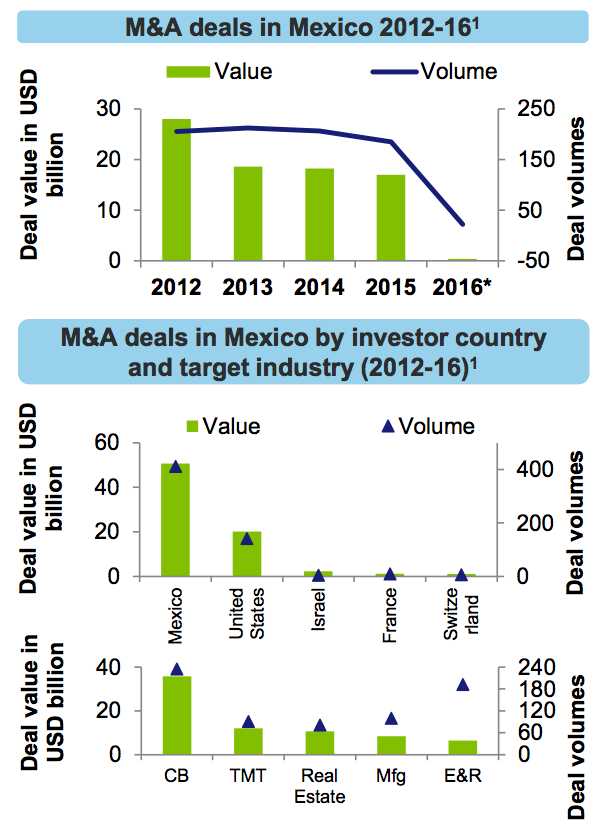

Mexico’s political reforms continue to attract investors

Mexico’s large domestic market, privileged access to the US, and reforms across sectors, such as telecom and energy, may help support M&A activity. However, a weakening consumer confidence, corruption scandals, crime rates, and low oil prices could offset positive impacts.

M&A favorable factors

• The Mexican government’s initiatives to limit monopoly in the telecommunications and broadcasting industries have helped foreign investors to enter the market. Mexico could also benefit from a relatively stable macroeconomic and monetary policy environment, ample international reserves, and a two-year IMF flexible credit line of USD70 billion. Reforms in the energy sector in Mexico opened the door to foreign participation in the country’s energy industry and may contribute to renewed growth in foreign investment in this sector.

• Mexico could continue to benefit from the dynamism of its export-based manufacturing sector, which has profited from a fairly weak peso, above-average productivity growth, and a shrinking gap in average wages compared with China. This may increase M&A activity. A recovering US economy could also help Mexico as US is a specific market for the country.

M&A unfavorable factors

• Slow GDP growth compared to the last decade and a less competitive market may dampen investor confidence. EIU expects that the economy may likely grow at 2.4% in 2016, followed by over 3% growth in 2017-2020.

• Weak governance can act as a deterrent for M&A activities in the region

• Weak structures of regulatory bodies to implement the policy changes related to tax and compliance areas could potentially dampen investor sentiments as approvals could be delayed. Political instability due to heightened crime rates, increased drug related violence, and high-profile corruption scandals may deter foreign players from investing in the country as such incidents can increase risk.

• Low oil prices weaken the fiscal outlook, considering that around USD23.4 billion of the government income/revenue comes predominantly from crude oil exports. This could hamper M&A activity within Mexico.

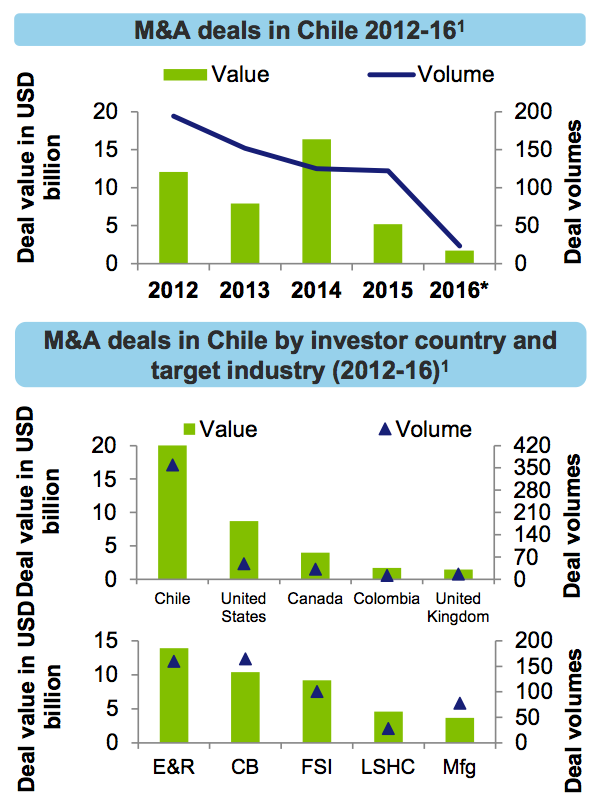

In Chile, the commodity sector dominated investments due to the natural abundance of minerals

Resource abundance coupled with government initiatives may boost M&A activities in the E&R sector. However, declining copper prices and reduced domestic investments may hamper M&A activity.

M&A favorable factors

• Chile’s investment climate is projected to remain the most attractive in Latin America in 2015-19 according to EIU Business Environment Rankings.

• Investments in the country may be boosted by its long-standing market economy, open investment regime, fiscal position, established capital markets, and large network of free-trade agreements.

• A strong E&R sector in Chile could increase M&A activity in the region

• International interest in Latin America’s commodity and natural resource assets is growing every year. The Comisión Nacional del Cobre (the state copper commission) projects that mining investment may exceed USD105 billion in 2014 – 23.

• The government’s initiative to draw 20% of energy requirements from renewable resources by 2025 could also drive investments.

M&A unfavorable factors

• The EIU predicts that GDP will grow only by 2.1% in 2016 followed by 3.2% growth in 2017-2020. Currency devaluation and policy reforms are the major reasons for the slow growth rates.

• Falling prices of copper have affected Chilean growth prospects. The price of copper—the country’s leading export commodity contributing more than 50% of Chile’s exports—began falling before that of other raw materials, which affected Chile particularly.

• Impending presidential elections in 2017 may shake-up the political scenario of Chile as it could cause a delay in clearances and approvals.

• The government’s move to raise corporate tax from 20% in 2014 to 27% by 2018 may dampen investor activity.

Colombia may attract investments due to an abundance of oil combined with falling oil prices

Falling oil prices could boost M&A activity, as oil and gas companies may turn to M&A to reshape the competitive landscape to their advantage. In addition, increasing consumer demand, and government initiatives further help open the economy for inbound capital flows.

M&A favorable factors

• The EIU forecasts that the Colombian economy is expected to grow at a rate of 3.8% between 2017-20 on account of forecasted improvement in oil prices, increased private consumption, and currency appreciation.

• The EIU also predicts that current-account deficit may narrow in 2016, at 5.6% of GDP. It could shrink further, to 3.1% of GDP on average in 2018-20, as oil prices rise. It is expected that foreign direct investment may likely cover the deficit in the outlook period.

• Colombia’s growing network of Free Trade Agreements (FTAs), specifically with the US and the European Union, could help bolster trade flows.

• M&A activity can be boosted by changes in the business environment including: falling labor costs and improvements in the quality of the labor force, macroeconomic policies aimed at keeping inflation and the external and fiscal deficits on track, and strong financial sector regulations.

M&A unfavorable factors

• The economy is heavily dependent on oil exports, and the steep fall in oil prices affects the trade balance of the country. Oil companies’ financials could be weakened due to high leverage and low interest coverage, which could reduce capital in flows. Export income fell by 26.7% in February 2016 from the same period last year owing to oil revenue contraction by 54.4%.

• Unsuccessful negotiations with Fuerzas Armadas Revolucionarias de Colombia (FARC) group may result in political unrest in the region. This could hamper foreign investments.

• The hike in the interest base rate by 25bps in November 2015 as inflation spiked to 5.9% could constrain credit. Monetary tightening could also hamper investment activity.

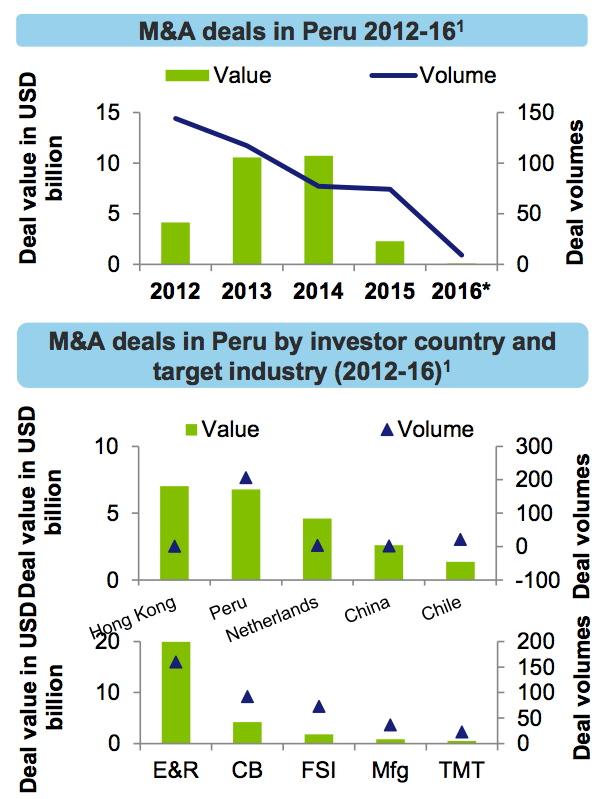

Peru’s heavy dependence on the weak Chinese market reduced capital inflows

Increased government efforts to attract investment and abundant natural resources could increase M&A activities. However, a poor institutional environment, dependence on China for exports, and declining commodity prices could limit Peru’s growth prospects.

M&A favorable factors

• The EIU forecasts that GDP will grow by 3.5% in 2016 and 4.2% in 2017-20 driven by the infrastructure pipeline and rising mining output. Peru’s economy is projected to be driven in by increasing private consumption and investment growth, ambitious infrastructure projects, low inflation, rising metals output, prudent fiscal policies, low debt and a manageable current-account deficit. This may be encouraging for investors aiming to invest in Peru.

• Peru’s investment-grade credit rating and the availability of investment protection resulting from a wide network of Free Trade Agreements (FTAs) may help maintain foreign investor confidence. The EIU expects that Foreign Direct Investments inflows to continue to rise to 4.3% of GDP by 2020.

M&A unfavorable factors

• Decline in prices of commodities such as copper and gold in the international market may continue to hamper Peru’s exports and the country’s trade balance. Declining exports to China (Peru’s major export market) due to a weak Chinese economy could affect capital inflows.

• A poor institutional environment, widespread income and regional inequalities, and rigid labor market may limit growth in the country.

• The second round of Presidential elections occurred in June 2016 and Pedro Pablo Kuczynski of the centre-right Peruanos por el Kambio will take office as president on July 28th. He will face governing challenges owing to his small congressional bench (just 18 of 130 seats), and obstruction from the fujimorista Fuerza Popular, which holds an outright majority.

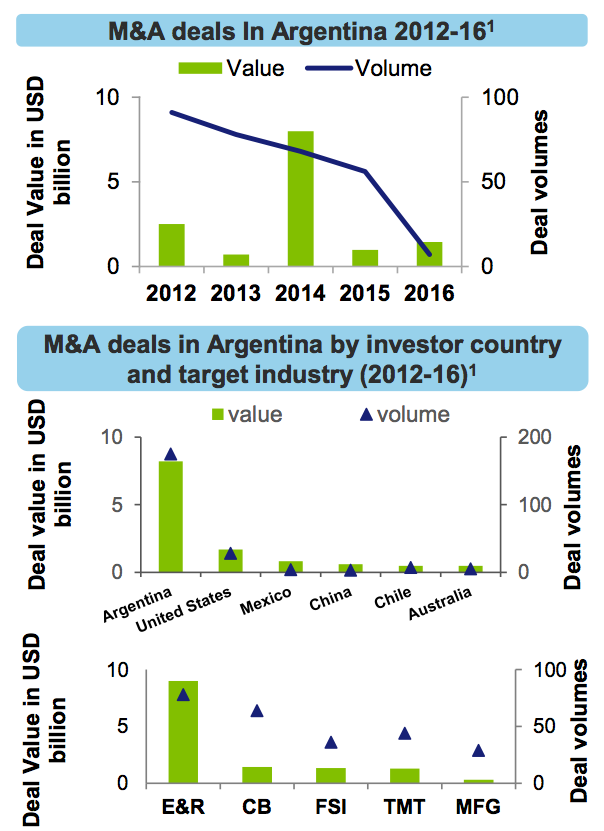

Argentina’s pro-business government policies could attract large investments

Abundant natural resources and optimism in the newly elected government may further increase M&A activities in the country. However, inflationary pressures could decrease the momentum.

M&A favorable factors

• Abundant natural resources may act as a positive catalyst in attracting investments:

• Argentina has vast reserves of natural resources that could contribute to interest in investments in the mining, agriculture, and consumer business sectors.

• Argentina is among the top five shale oil and gas reserves across the globe making it a top destination for potential energy investments.

• The new government was sworn into power in December 2015. The government‘s actions and public communications appear to indicate a pro-business focus which may help increase credibility and optimism among investor circles:

• The government lifted certain capital and trade restrictions, such as eliminating export taxes on a range of agricultural products. Further, the new government indicated it may raise the low energy tariffs that made oil production potentially less profitable and hindered investments.

• The government removed foreign-exchange controls allowing the currency to devalue by around 50 percent in mid-December 2015. This may encourage foreign investors to acquire assets at more favorable rates.

• Debt settlement with holdouts have resulted in an improvement of the country’s credit rating. This may positively impact Argentina’s access to credit and boost M&A as well as large infrastructure projects.

M&A unfavorable factors

• Higher inflationary pressures could result in monetary tightening that could potentially lead to limited credit availability resulting in low growth and reduced M&A activity.

M&A activity across industries

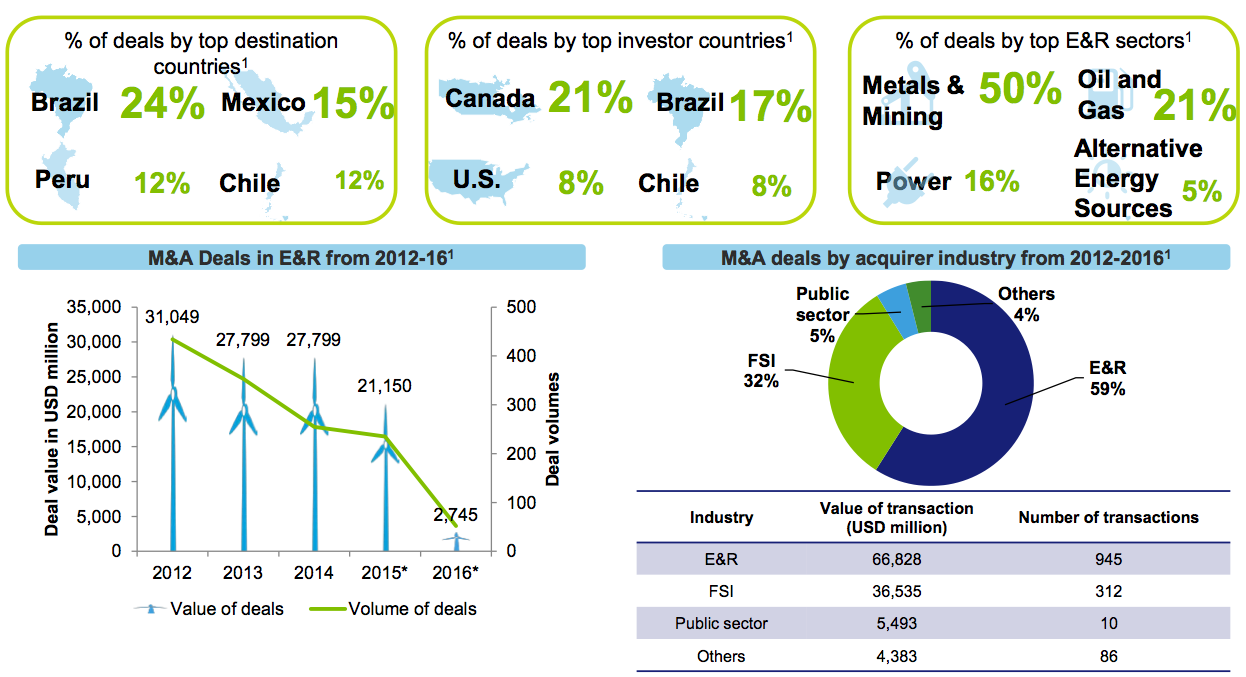

Weak macroeconomic factors pulled down Energy & Resources (E&R) M&A activity

The abundance of natural resources in Latin America helped drive M&A in E&R. Many Latin American miners benefited from the consolidation in the mining industry over the last decade. However, falling oil prices and a weak commodity market weakened M&A activity in 2015.

Consumer Business (CB) deals were dominated by the food & beverage (F&B) sector

F&B sector has the maximum volume of M&A deals in the CB industry. A growing middle class with a larger disposable income helped contribute to consumerism in the larger economies such as Brazil and Mexico. However, Brazil’s negative GDP growth rate may act as a deterrent in 2016.

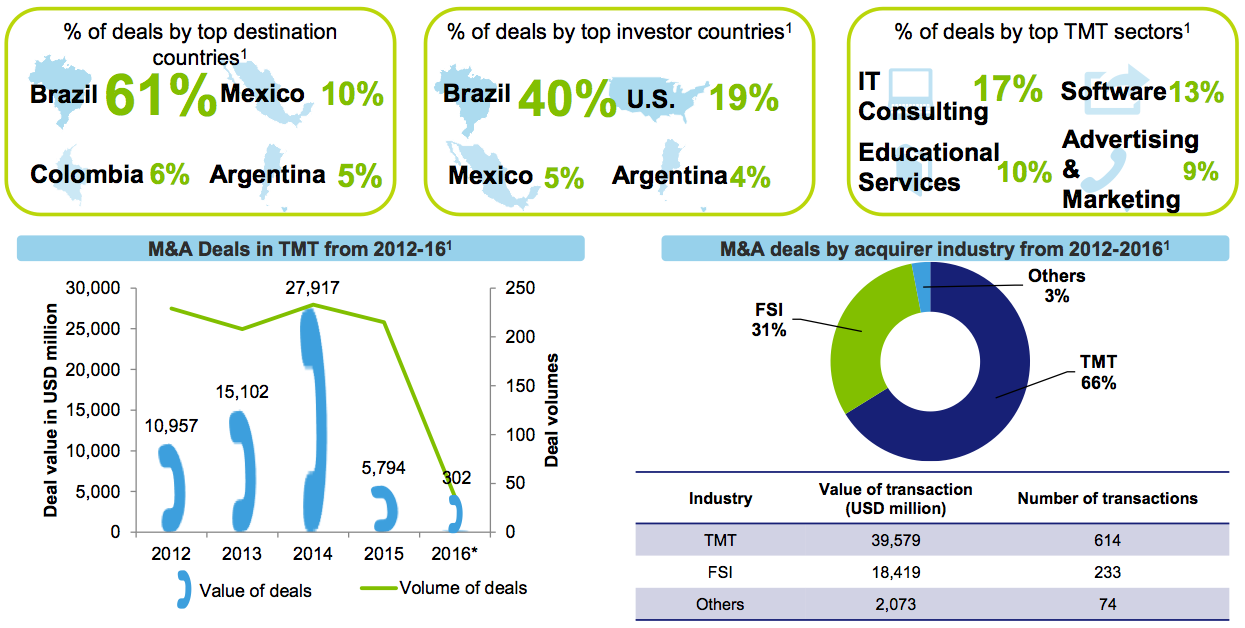

Intra-region deals bolstered most M&A activity Telecommunications, Media, Technology (TMT) industry

The recent telecommunications reforms in Mexico and the growing trend of convergence of TMT services helped contribute to an increase in foreign direct investment and M&A activity. However, economic stagnation in the region may likely weaken the momentum of M&A activity in 2016.

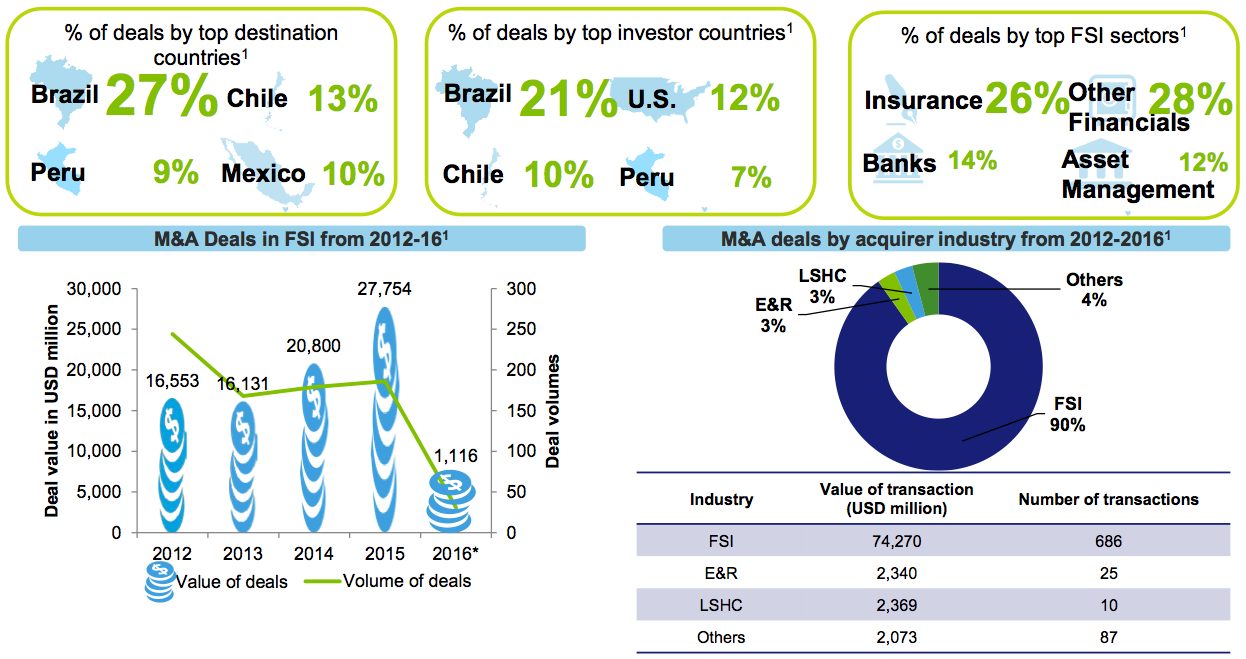

Financial services industry (FSI) recorded consistent growth in M&A deals during 2014-2016

While expansion plans of foreign banks were common prior to the global financial downturn, investment activity slowed down post crisis. Although other industries witnessed slowdown in M&A activity in 2015, Financial Technology (FinTech) deals helped propel FSI M&A activities in 2015.

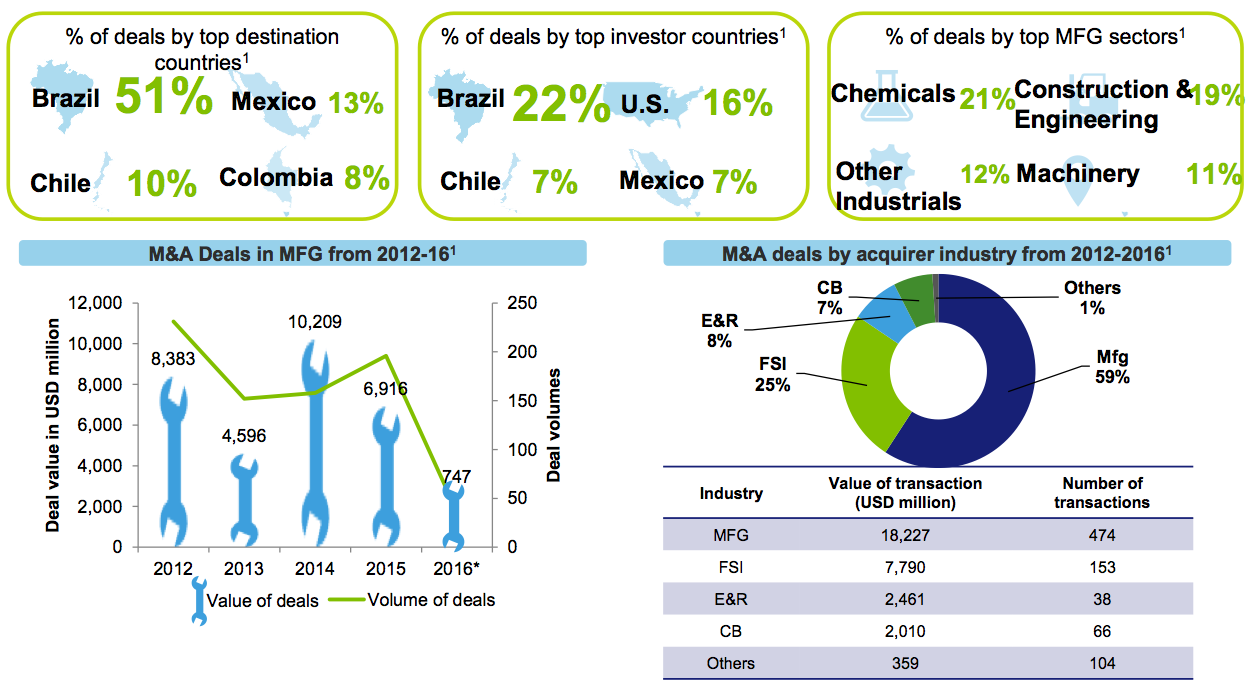

Higher capital inflows owing to weaker currency may boost Manufacturing (MFG) sector investments

Brazil and Mexico continue to be the top destination countries in manufacturing M&A activities. Favorable asset prices owing to currency fluctuations may help attract more foreign investors into the industry.

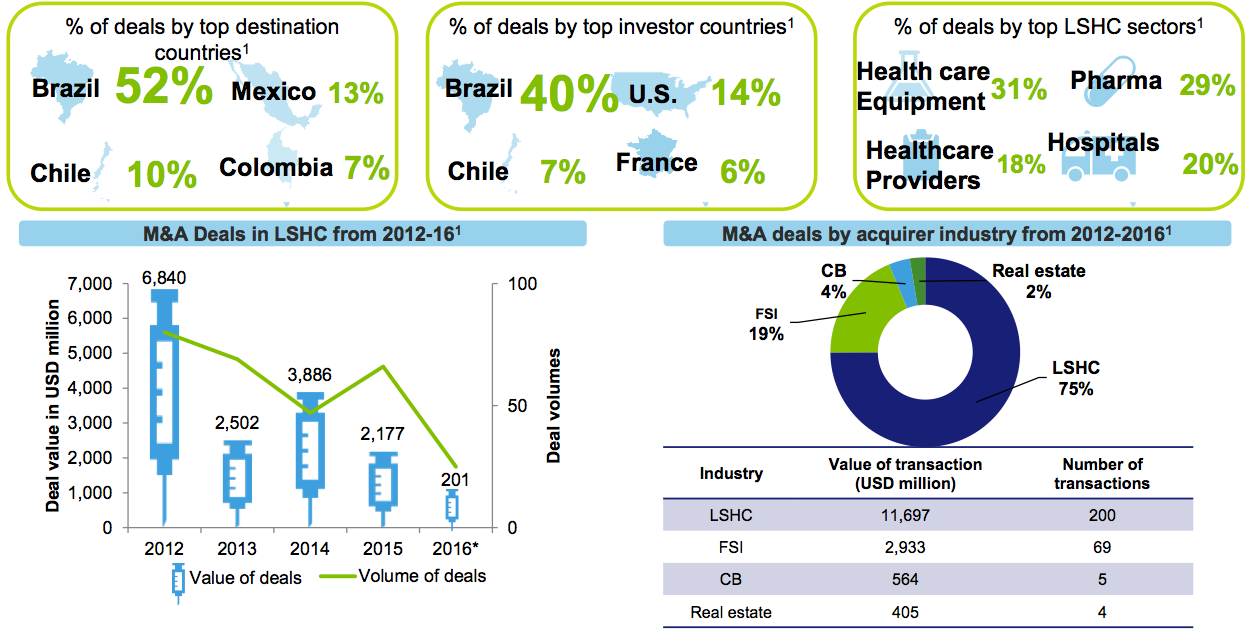

Brazil remains the top source and destination for M&A activity in the Life Sciences Healthcare (LSHC) sector

The large population base in Brazil combined with higher healthcare demand helped attract the LSHC sector to Brazil. Though the consolidation in the LSHC sector has slowed down since 2012, a rise in healthcare spending by the growing middle class may attract more international players to Latin America.

(1. Thomson Reuters. (2016). M&A Overview. Retrieved May 20, 2016, from Thomson ONE database.)

Stay up to date with M&A news!

Subscribe to our newsletter