By Pip McCrostie – Ernst & Young

Our 11th Capital Confidence Barometer predicts healthy growth for M&A globally, which should take the market back to levels last seen before the financial crisis.

As we predicted in our previous Barometer, much of 2014 has seen a big increase in multibillion-dollar deals. Now, increasing competition at the top end and a renewed focus on growing core businesses will fuel more middle-market deals.

As a result, after a five-year slump — and many stalled M&A revivals during that time — deal activity globally is set to return to 2006 levels.

The appetite for M&A is as high as it has been for more than three years, supported by relatively stable economic confidence. Meanwhile, deal fundamentals remain very strong: balance sheets are healthy, credit is available and valuations are seen as steady.

The biggest indicator of positive deal sentiments is pipeline. Deal pipelines have increased by a remarkable 30% since April. In addition, two thirds of executives expect M&A pipelines to expand further over the next year — this is more than double the number expecting expansion six months ago. In the past, this might have been the recipe for a wave of high-risk M&A.

Not today. Greater complexity in the shape of global ‘megatrends’ such as digital transformation and external pressure such as that exerted by shareholder activists are helping to ensure executives are focused on lower risk transactions. High profile mega-deals will continue in this environment. However, the Barometer finds that the majority of acquisitive companies are focusing on M&A to strengthen their core business, with an eye to boosting market share, managing costs and improving margin growth. As a result, the vast majority of planned deal activity will consist of bolt-on acquisitions that will complement their current business model.

This is positive news for the M&A market. After years of contraction and stagnation, deal activity globally looks set to return to pre-crisis levels. The transformative deals hitting the headlines in 2014 are set to continue. However, the next chapter of the M&A story should be middle-market momentum, taking deal activity to new heights.

Key findings

40% Big increase in global companies expecting to do deals in the next 12 months; up by a third in six months

81% Vast majority seek middle-market deals below US$1b, driving next M&A wave; focus on expanding core business

66% Two-thirds report bulging M&A pipelines; expectation for further expansion doubles in six months

44% Nearly half see global economy as stable; helping boost M&A appetite after five-year slump

Macroeconomic environment

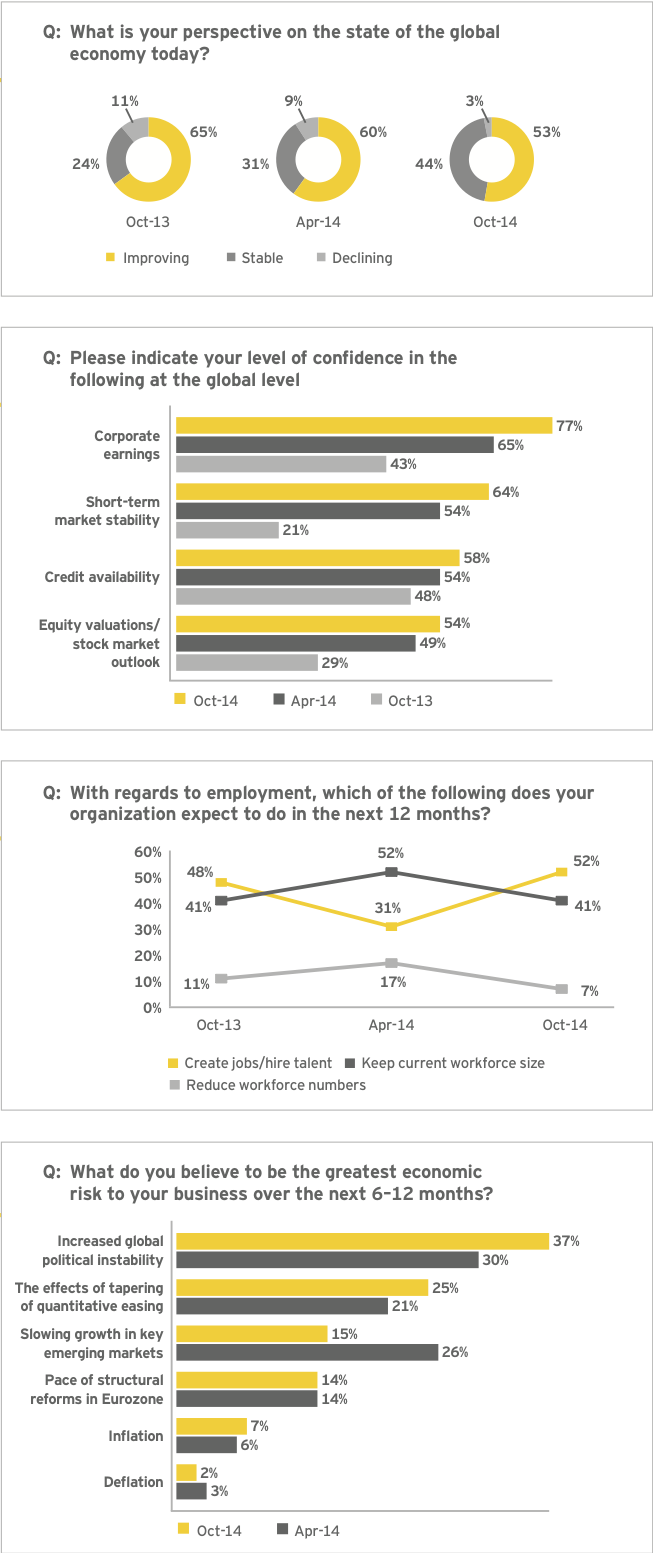

Despite a continuation of disruptive external influences, greater confidence in global economic stability lays the foundation for future M&A.

The number of executives that view the global economy as stable has almost doubled in the past 12 months.

• Executives are increasingly confident in the stability of the global economy

While fewer executives today believe the global economy is improving, the number that believe the economy is stable has almost doubled. Greater confidence in economic stability allows companies to plan more freely for growth and M&A. Stability is an essential ingredient in a healthy M&A environment. Another positive signal is that the number of those who believe the economy is declining has dropped to negligible levels.

• Outlook for corporate earnings shows strong growth

The number of executives who are confident about the outlook for corporate earnings has increased significantly over the last 12 months.

Corporate earnings, particularly in the US, were remarkably strong in the first half of 2014, with 70% of the S&P 500 beating estimates. Results in the UK and Eurozone were mixed, as currency and regional concerns influenced respondents in those geographies.

Other market indicators are also trending positive.

• Confidence in market indicators driving positive hiring intentions

Improved sentiments are driving positive hiring intentions. Companies are more confident about hiring: more than half expect to create jobs or hire talent, up from 31% in April 2014. The number of companies planning to reduce their workforce has dropped to 7% from 17% six months ago.

• Resilient M&A sentiments not dampened by increased geopolitical risks

Although they do not expect major shocks to the economic or financial system, our respondents identify geopolitical instability as a potential threat to their business. Driven by tensions between Russia and Ukraine and ongoing conflict in the Middle East, geopolitical issues figure more prominently than six months ago. In contrast, concerns about emerging markets and deflation have both fallen.

In the past, issues such as these would have stalled any M&A uptick. Now, executives are more comfortable taking risks amid all this uncertainty.

Corporate strategy

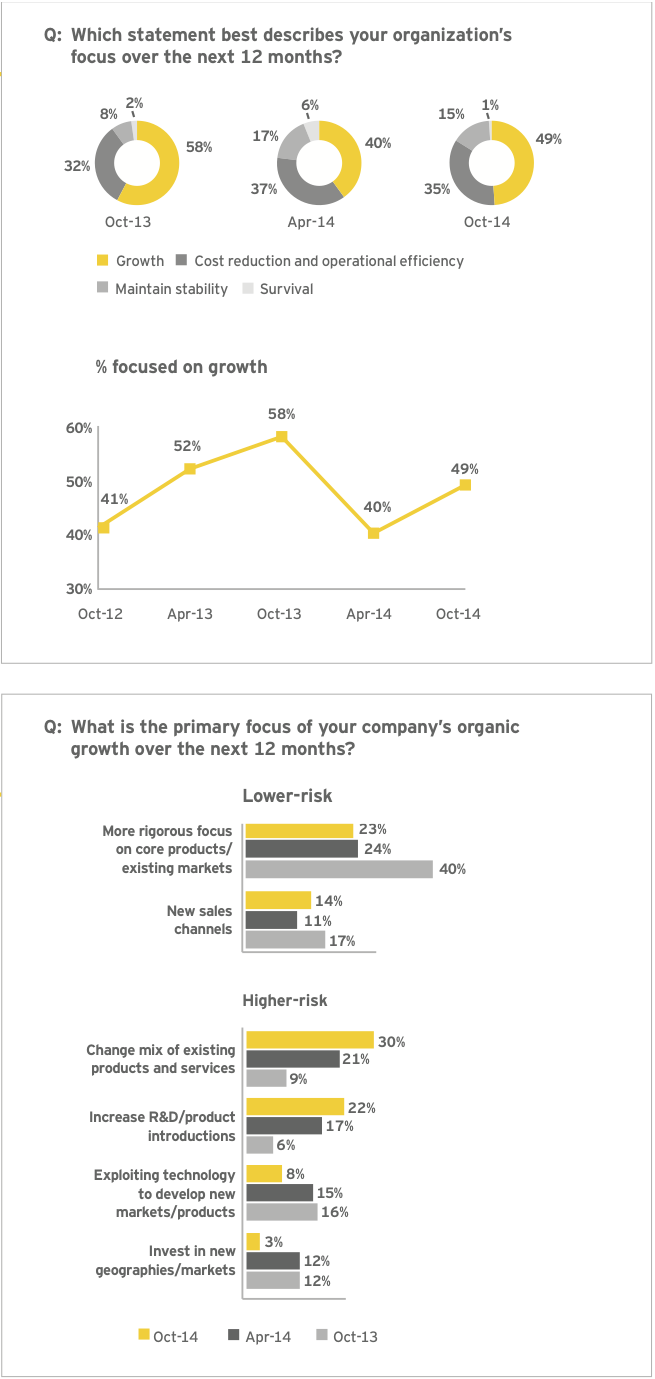

Companies are making moves to position themselves for growth in a challenging environment shaped by fast-emerging global megatrends and enhanced shareholder engagement.

In line with their growing confidence in global economic stability, more companies are expanding their core business by changing their mix of products and services and increasing product introductions. Our survey shows a threefold increase in the number of companies adopting both of these strategies.

• Companies seek growth — but not at the expense of cost efficiencies

The focus on growth is tempered by a disciplined approach to cost reduction and operational efficiency, as executives remain mindful of lessons learned during the global financial crisis. Fewer companies are preoccupied with survival.

• Organic growth centers on core capabilities; higher-risk strategies remain attractive

In line with their growing confidence in global economic stability, companies are taking on more risk as they expand their core businesses by changing the mix of products and services. Our survey shows a threefold increase from a year ago in the number of companies changing their product mix.

This reflects a pattern of complex activity where companies are divesting non-core units and strengthening and expanding their core and complementary businesses through sophisticated transactions, such as asset swaps, spinoffs and joint ventures.

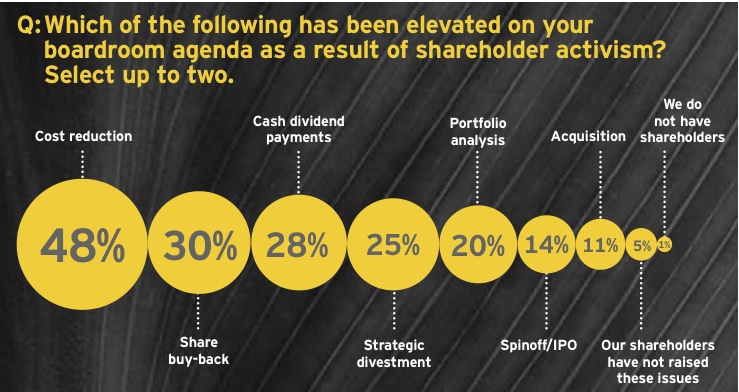

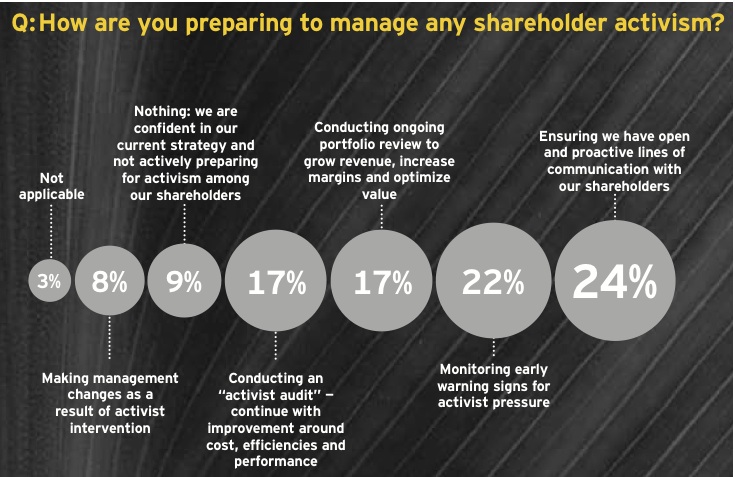

Activist shareholders influence boardroom agenda

The C-suite agenda — organic and inorganic growth priorities — is increasingly swayed by the growing influence of shareholder activism.

With growing success and greater influence, activist investors continue to rise in prominence as the market enters a new phase of low but stable growth. Cost management, portfolio optimization and returning cash are key areas of focus. M&A will also likely be part of the story with asset sales and acquisitions part of the ever-broadening activist dialogue.

As a result, companies are stepping up their efforts to manage shareholder activism, enhancing communication with stakeholders, monitoring signs of activist pressure and performing ongoing portfolio reviews.

The consumer products sector, which has seen several notable cases of activist intervention, is especially susceptible to activist influence due to the high profile of the companies and the investment opportunities available.

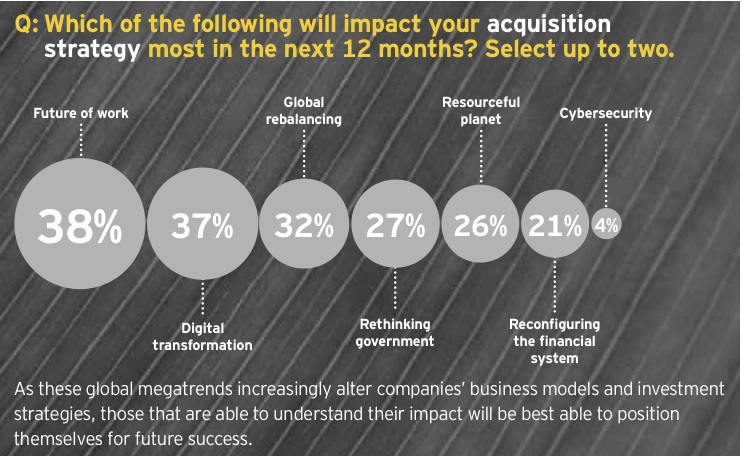

Massive global changes reshaping corporate strategies

Executives expect global megatrends — particularly rethinking government, the future of work and digital transformation — to have a significant impact on their business and acquisition strategies.

Governments worldwide are rethinking their strategies and policies in response to huge challenges. From building social safety nets in key emerging markets to reducing deficits and debt in developed countries, governments are trying to meet these challenges without dampening economic expansion. These changes have far-reaching implications for business, creating an urgent need to stay agile, keeping up with policy changes and ensuring compliance and collaboration with public-sector agencies.

Driven by shifting expectations and needs by both employers and employees, the traditional talent contract is being rewritten. An increasing number of mobile, part-time and self- employed workers are changing the nature of work and the workplace. The move to a more flexible workforce will provide more opportunities for collaboration and productivity, as well as acquisitions. Dealmaking in many industries, especially those that are high-tech or IP-rich, will center on the battle for talent.

In contrast to the overall trend toward a focus on the core, technology assets are in demand in nearly every sector. Emerging technologies are combining with advanced networks, computing and new ways of communicating to fundamentally change businesses. As companies adapt to these advances, dealmakers in all industries will need to decide how they strategically invest in technology. Front-end early adapters will be the most attractive acquisition targets, offering innovative and nimble strategic capabilities to acquirers.

As these global megatrends increasingly alter companies’ business models and investment strategies, those that are able to understand their impact will be best able to position themselves for future success.

M&A outlook

The appetite to execute deals is high, and pipelines are bulging and set to expand further. M&A activity is about to reach pre-crisis levels. Transformative M&A will continue. However, the strongest growth in M&A activity in the coming year will be middle-market momentum as companies strengthen their core businesses.

The spate of megadeals during 2014 is having a ripple effect on the M&A market. They increase confidence in M&A and trigger transaction activity further down the deal chain.

M&A activity set to rebound globally after five-year slump

• Appetite to acquire hits three-year high

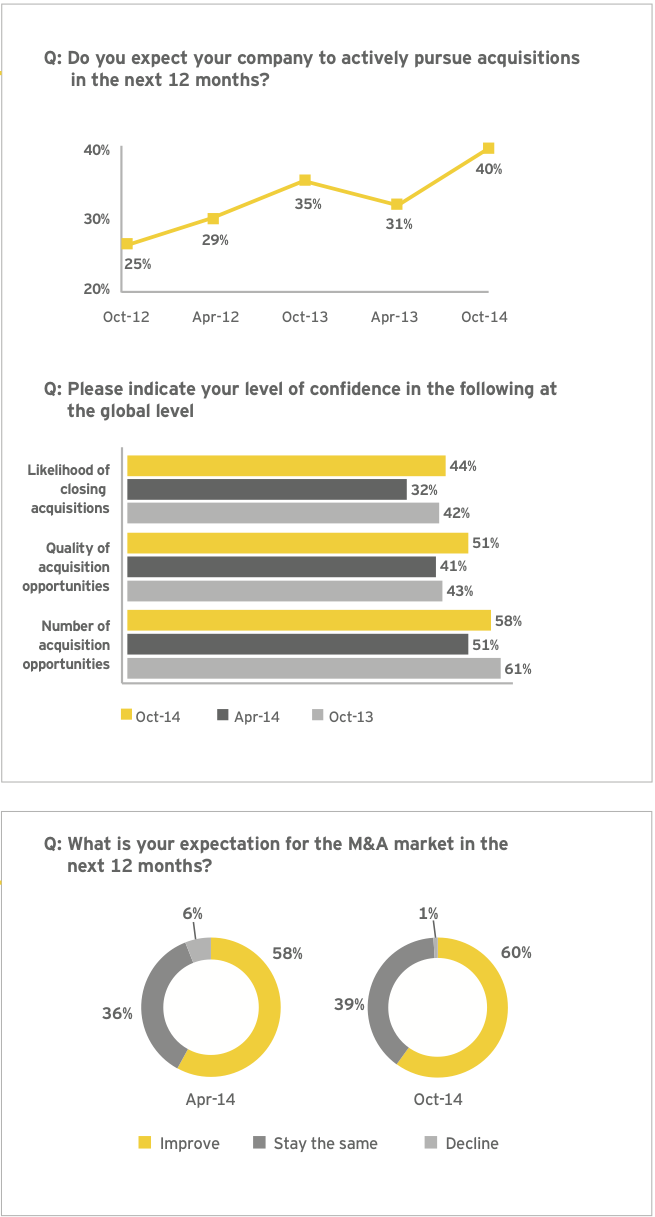

Companies’ appetite to do M&A is at a three-year high, with 40% of executives expecting to pursue acquisitions in the next 12 months. This is a clear signal of intent to look at deals as a route to growth.

Dealmaking challenges still persist: just under half of executives are confident about the likelihood of closing acquisitions. This may be because of increasing rigor in the search for strategically aligned assets, more thorough due diligence or greater competition.

• Executives see accelerating M&A market in the near term

An improving view of the resilience of the global economy, strong equity markets and enhanced corporate earnings have helped boost the outlook for M&A among respondents. While 2014 has been notable for high-profile megadeals, the Barometer suggests that middle-market M&A will provide a significant lift to deal activity.

Almost two thirds of respondents expect deal volume to increase further in the next 12 months — even after a relatively positive 2014 for M&A. This suggests continuous improvement in outlook and the number of respondents anticipating a decline is now negligible. Unlike the heavy focus on US-based assets in recent years, a rise in M&A is anticipated across all sectors and geographies in the next year.

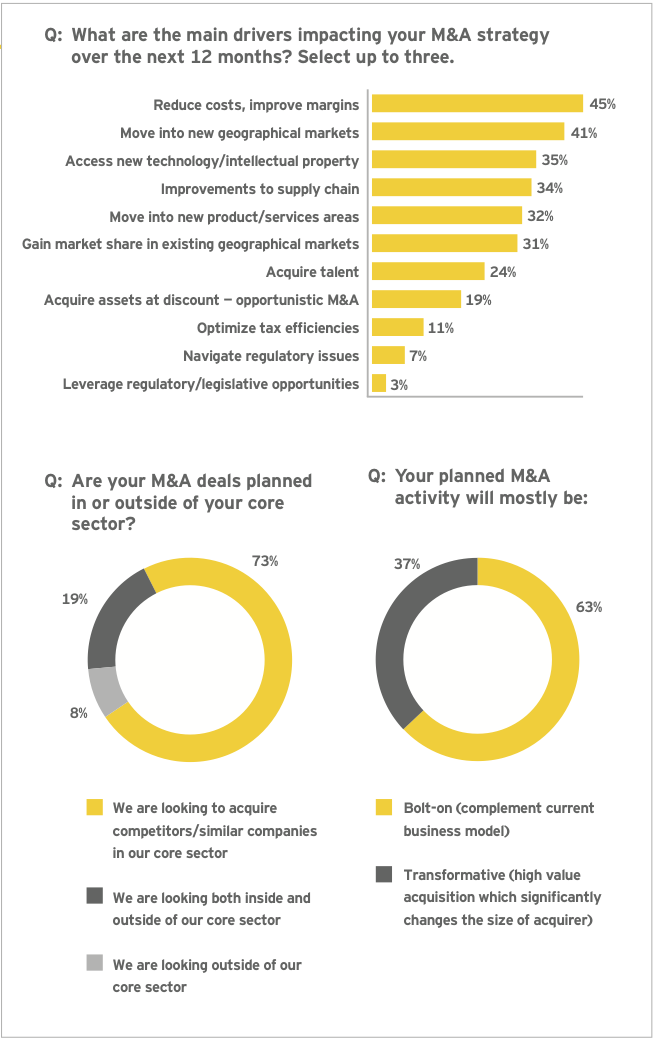

Middle-market deals to fuel M&A rebound

Focus on core and bolt-on acquisitions to drive middle-market deals

Our previous Capital Confidence Barometer correctly predicted the rise of multibillion- dollar deals in 2014. These megadeals are having a significant ripple effect on the M&A market. They increase confidence in M&A and trigger transaction activity further down the deal chain.

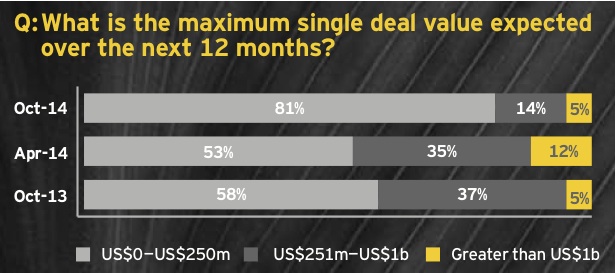

With the appetite to acquire at its highest for three years, we now expect a new wave of M&A with much more focus on mid-market sized deals. This new middle market momentum should lift M&A activity as companies seek to strengthen — and expand — their core business.

The climate continues to remain favorable for large acquisitions. However, the growth of M&A should be defined by the major shift in focus among respondents looking to do deals valued at $250 million and under.

The majority of companies are focusing on acquiring businesses in their core sectors, with an eye to boosting market share, managing costs and improving margin growth. As cost efficiencies are paramount, for the vast majority, planned M&A activity will consist of bolt-on acquisitions that will complement their current business model.

The increasing influence of shareholder activism is helping to ensure that cost management remains a critical component of organic and inorganic growth strategies. Half of respondents say that cost reduction has been elevated on the boardroom agenda as a result of shareholder activists.

While the majority of companies are focusing on acquiring bolt-on businesses, more than a third still expect to undertake transformational deals. The upper end of the M&A market should continue to see megadeals, but we can also now expect a formerly subdued middle market to vigorously enter the fray. The net result should be a far more buoyant deal market than we’ve seen for the past five years.

The majority of deals swelling pipelines are focused on strengthening the core business, by boosting market share, managing costs and improving margin growth.

Bulging pipelines expected to expand even further in the next year

• Bullish deal intentions as pipelines swell

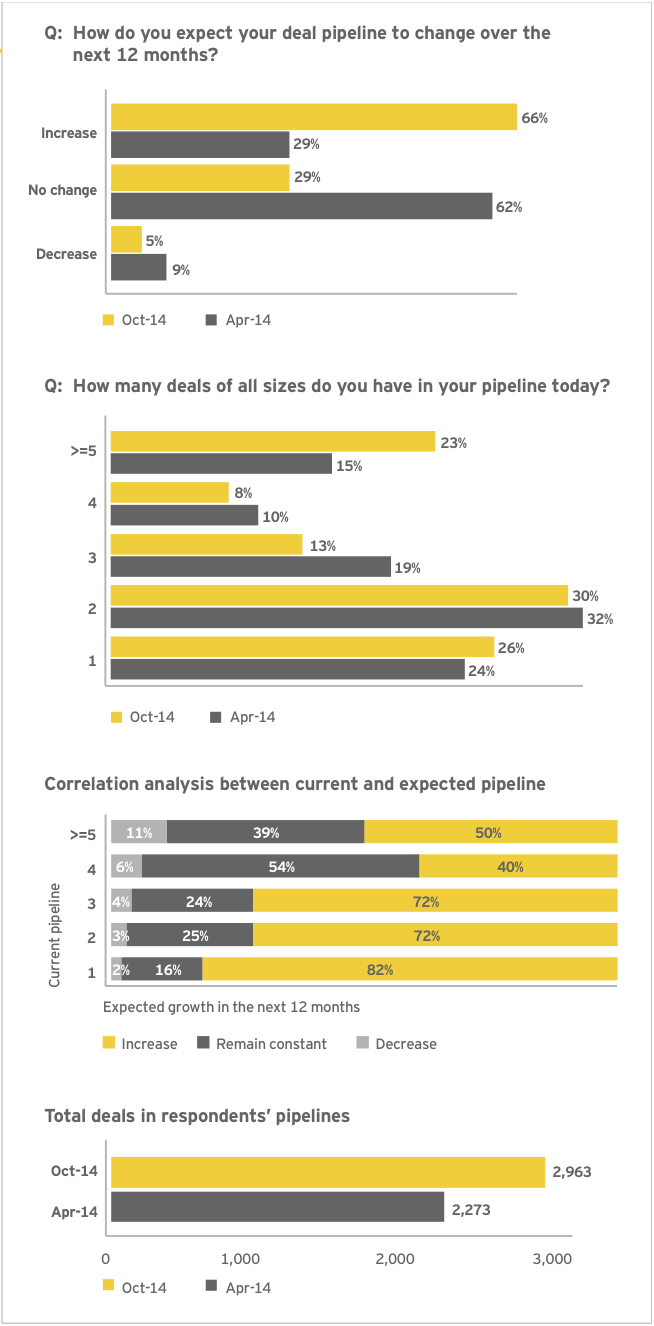

The number of companies that have more than five deals in the pipeline has increased significantly. Renewed discipline in dealmaking is forcing companies to thoroughly examine many more investment opportunities to find the best strategic fit.

The number of deals being considered by our respondents has also substantially increased, with the aggregate total up 30% since April 2014.

A further sign of growing momentum: almost two thirds expect M&A pipelines to expand further over the next year — more than double the number expecting increases six months ago.

An analysis of the correlation between current pipelines and expectation to increase shows that companies with the smallest pipelines express the most desire to expand in the next 12 months. Companies with larger pipelines are overwhelmingly in favor of maintaining or even increasing theirs as well.

This move toward larger pipelines bodes well for a rebound in M&A in the near term — especially in the middle market, where there are more assets for companies to target.

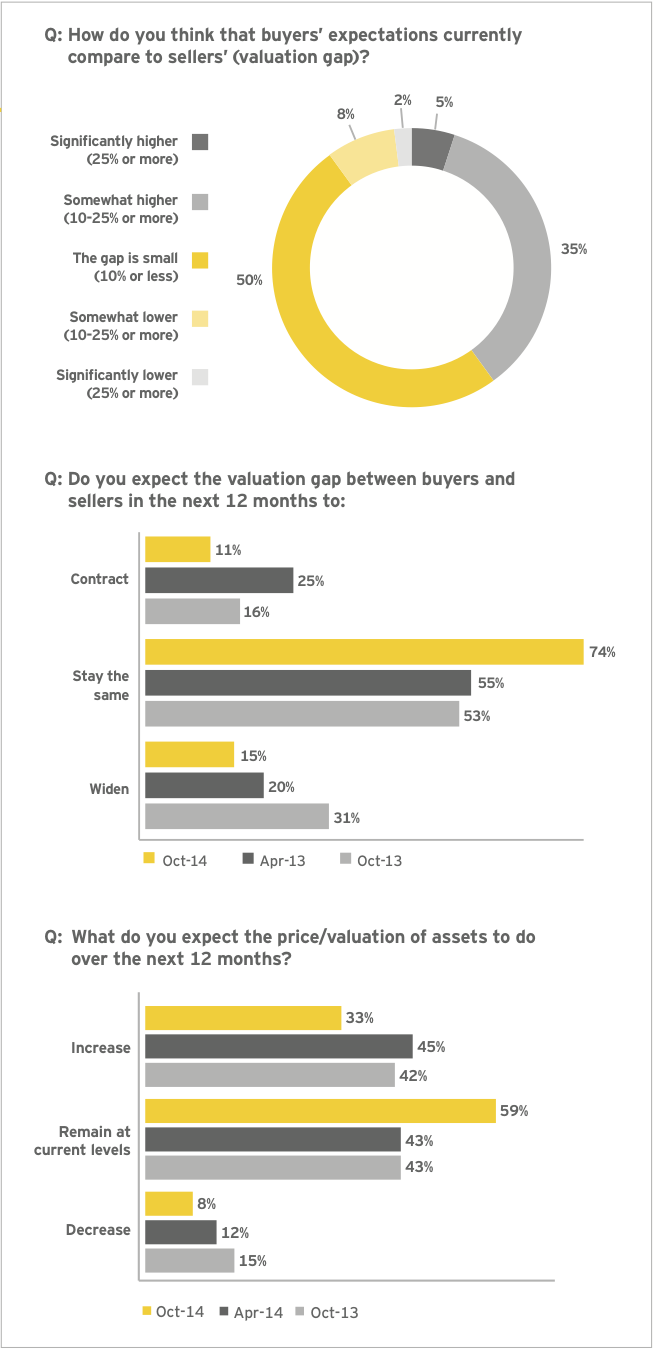

Stable valuations to enable dealmaking

• Modest valuation gap and confidence in asset prices underpin positive deal sentiments

There is a strong consensus among our survey respondents. Half of executives see only a small discrepancy between buyers’ and sellers’ expectations on asset valuations. This, combined with the outlook for stability in the valuation gap and the overall value of assets, will encourage dealmaking in the near term.

The number of respondents that see the current valuation gap as either higher or lower than 25%, which would be difficult to resolve through negotiations, is now down to only 7%.

The more stable outlook for both the valuation gap and price of assets in the next 12 months reinforces the view on stability in macroeconomic conditions and the M&A market.

As buyers become more confident in newly acquired assets’ long-term value, and sellers no longer hold out for higher prices in the future, volumes should accelerate — especially in the lower middle market, where the valuation gap is most easily bridged.

Dealmaking focuses on core business

• Acquisition plans center on core

The majority of companies are focusing on acquiring businesses in their core sectors, with an eye to boosting market share, managing costs and improving margin growth. This is strongly aligned to their focus on organic growth plans.

Companies are planning to strengthen and expand the core. They are assessing a range of transaction drivers — but cost efficiencies are paramount.

Consequently, for the vast majority of companies, planned M&A activity will consist of bolt-on acquisitions that will complement current business models or be in adjacent sectors.

More than a third of companies plan to make acquisitions that give them access to new technologies or intellectual property. In many sectors, this will translate into the acquisition of innovative middle-market assets.

In the current climate, transformative M&A — high-value acquisitions that significantly change the size of the acquirer — and deals that shift the scope of their business look set to continue. More than a third of respondents are considering such transactions.

However, mid-market deals look set to drive volume in the M&A market over the coming 12 months.

Strong deal sentiment across many sectors

Search for intellectual property and strong brands to drive key sectors

The top industry sectors have been transacting vigorously and will continue to see more activity going forward.

45% Automotive and transportation

Automotive sector M&A is being motivated by renewed optimism, brought about by increasing sales in both developed and emerging markets and a sector-wide drive to decrease costs and improve efficiencies. A significant number of deals focus on acquiring emergent technologies, such as driverless cars and advanced materials.

44% Technology

Technology deals derive from increasing competition for assets related to smart mobility, cloud computing, social networking, big data analytics and accelerated adaptation. Furthermore, some established technology companies are making deals involving “moonshots” — technologies that may drive dramatic change and commensurate returns, such as the “Internet of Things” (IoT) and augmented or virtual reality.

42% Life sciences

Life sciences deals are driven by increased specialization in therapeutics and advanced treatments, consolidation in medical devices and an ongoing drive to grow market share and improve margins. As they face significant growth challenges ahead, pharmaceutical companies will need to become more acquisitive, but the growing strengths of big biotechnology and emerging pharmaceuticals are leading to both increased competition for deals and more expensive targets.

41% Consumer products and retail

Consumer products companies have sharpened their focus on developed-market businesses. In the absence of ample growth avenues, companies are targeting operational efficiency by making strategic divestments. Portfolio optimization is emerging as a critical theme, driving strategic transactions amid increasing investor pressure on companies to deliver shareholder value. Large consumer product players are optimizing their brand portfolios and market exposure by disposing of non-core and lower-growth businesses and rechanneling investments into acquiring or expanding in faster-growth or higher-margin businesses.

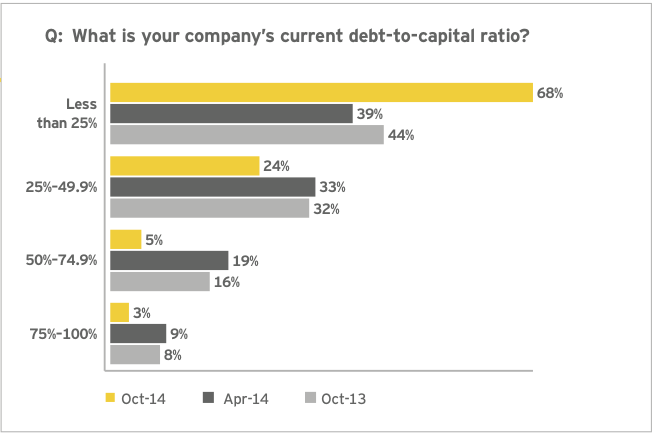

Debt to fund future dealmaking

• Balance sheet strength leads to drop in highly leveraged companies

Leverage has declined since the global financial crisis, thanks mainly to increases in equity value. According to the S&P Global BMI (Broad Market Index) — a cross-country, cross-sector index — the value of average market capitalization has increased 60% since October 2009, whereas total debt rose by only 19%.

The majority of companies in our survey report a debt-to-capital ratio of less than 25%, leaving them well positioned to withstand any near-term increase in interest rates.

• Strong balance sheets leave room for debt

Nearly half of executives expect their companies’ debt-to-capital ratios to increase over the next 12 months, indicating a willingness to take on more debt to fund growth ambitions.

Those looking to decrease debt-to-capital ratios have more than halved since April 2014.

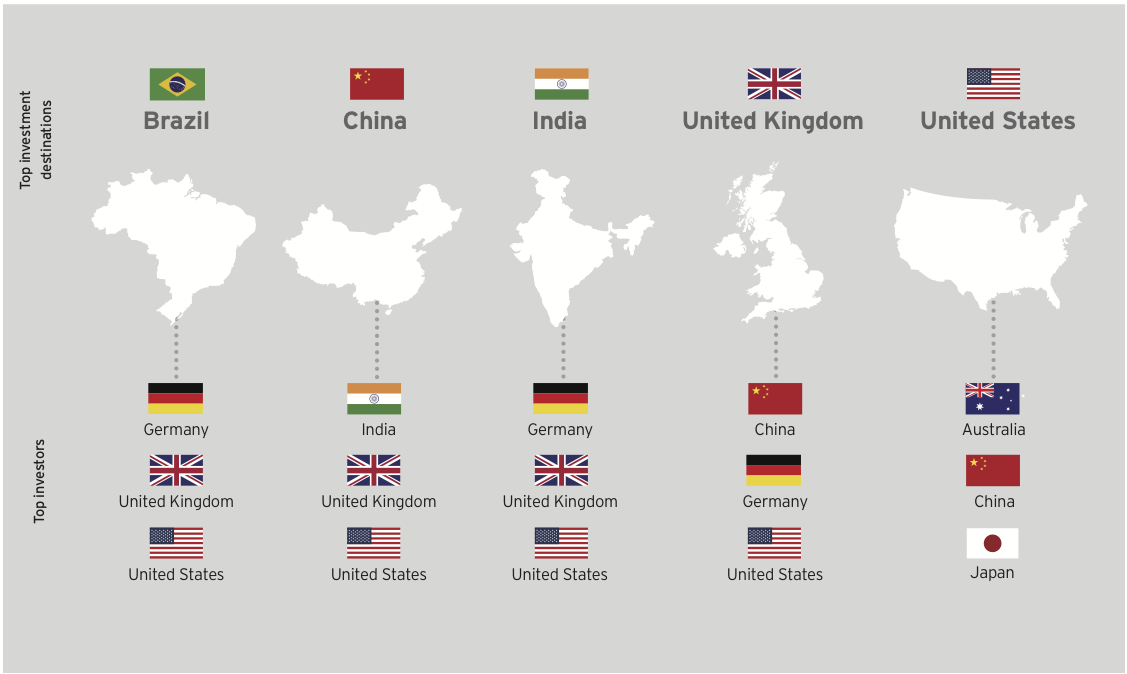

Companies are focusing their crossborder M&A activity around a core group of developed and top-tier emerging countries.

The US and UK continue to attract inbound M&A investment. China, India and Brazil are also very attractive dealmaking destinations for our survey respondents.

Top investment destinations and their top three investors

• M&A in Brazil is likely to remain firm, supported by a governmental focus on infrastructure and a weakening currency, and underpinned by Brazil’s growing middle class. However, with elections coming up in October, investors may be in a wait-and-watch mode in the third quarter of 2014.

• China remains attractive due to its continuing strong and stable levels of economic growth. With economic rebalancing a stated policy of the Chinese government, further investment opportunities should arise for inbound investors.

• India’s deal market is expected to improve. Investor sentiment is seeing a significant recovery, with stock markets hitting all-time highs. In addition, the new government’s pro-business stance should foster a more benign investment landscape for inbound investment.

• The UK has long been a favored destination for foreign firms wanting to access the wider EU market. With strong domestic growth forecast through 2014–15 and a focus on reducing onerous red tape, the UK should be able to continue this trend.

• The US M&A market is attractive to foreign investors, thanks to improving economic fundamentals and strong corporate earnings. In this positive transaction environment — and with an interest rate rise not expected before early 2015 — we expect high levels of deal activity to sustain over the coming months.

Companies are focused on optimizing their allocated capital

A strong Capital Agenda should be at the core of all strategic boardroom decisions. It is the framework for all growth and capital management questions.

About this survey

The Global Capital Confidence Barometer gauges corporate confidence in the economic outlook and identifies boardroom trends and practices in the way companies manage their Capital Agendas — EY’s framework for strategically managing capital.

It is a regular survey of senior executives from large companies around the world, conducted by the Economist Intelligence Unit (EIU). Our panel comprises select global EY clients and contacts and regular EIU contributors.

• In August and September, we surveyed a panel of more than 1,600 executives in 62 countries; more than half were CEOs, CFOs and other C-level executives.

• Respondents represented 18 sectors, including financial services, consumer products and retail, technology, life sciences, automotive and transportation, oil and gas, power and utilities, mining and metals, diversified industrial products and construction.

• Global companies’ annual global revenues ranged from less than US$500m to greater than US$5b: <US$500m (18%); US$500m— US$999.9m (24%); US$1b—US$4.9b (31%); and >US$5b (27%).

• More than 800 companies would have qualified for the Fortune 1000 based on revenue.

• Global company ownership was publicly listed (64%), privately owned (22%), PE/portfolio-owned (9%) family- owned (3%), and government/state-owned (2%).

Stay up to date with M&A news!

Subscribe to our newsletter