By Ragnar van der Valk, Dingenis Blok – PricewaterhouseCoopers, KLM

As soon as the deal has been closed the real work starts: the integration. This is a much-heard comment in the world of mergers and acquisitions. A study by PricewaterhouseCoopers (PwC) shows that, in 89 percent of merger and acquisition cases, the IT function is subject to post-deal integration in some form or other.

IT integration scenario

PwC identifies four generic IT integration scenarios in mergers and acquisitions:

1. Preservation: loose integration of structures, systems and skills, so that the two IT organisations remain autonomous and preserve their own unique operating models and cultures. This is a typical scenario for a financial holding.

2. Combination: alignment of organisational and technical components of the two IT organisations, thereby creating a best-of-breed-type solution.

3. Consolidation: quick integration of all systems, processes, people and assets into the organisational and technical architectures of the acquiring organisation.

4. Transformation: replacement of legacy structures, processes and systems of the two organisations with an entirely new operating model for the merged entities, i.e. a greenfield situation.

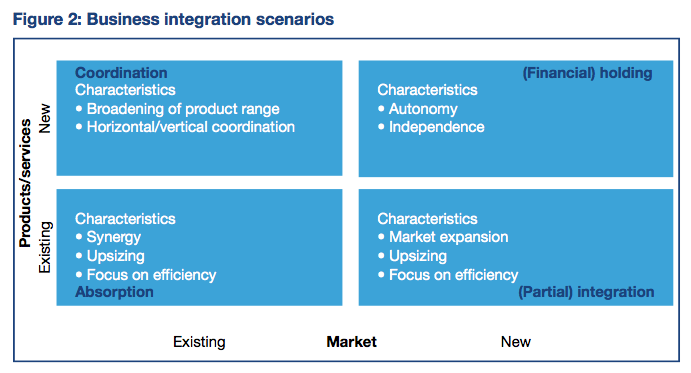

The level of IT integration, from contractual integration to full organisational integration, is largely contingent on the business integration strategy. There are roughly four business scenarios for a merger or acquisition, seen from the perspective of a product and market strategy (product/market combinations): absorption, partial integration, coordination and financial holding.

All four scenarios can lead to different forms of IT integration; absorption and partial integration, being the most drastic forms of business and IT integration, should be special priorities for the parties involved. The ICT function will play a more reactive role in other forms of integration, i.e. in a financial holding. In this form, IT integration will usually take place at contractual and/or infrastructural level at the most.

The need for absorption and partial integration in mergers and acquisitions, and the subsequent IT integration is often fuelled by a need for less organisational autonomy and massive strategic interdependence of the two organisations. Examples of this type of integration are the merger between Air France and KLM, and DHL’s acquisition of Exel.

Organisations in these situations will usually opt to merge (parts of) their business in order to achieve efficiencies, effectiveness and cost reductions, but mostly to form a united front to the client. In this process, the IT function is a key enabler for successful integration. Consequently, the IT function needs to take a proactive approach if the envisaged success is to be achieved.

Transparency

It is only a matter of time before the new, more integrated business will more explicitly demand to see synergy effects based on integrated ICT services, transparency in pricing, and quality delivered by the two ICT organisations. This not only poses a challenge for the structure of the ICT organisation, but also for its financial management. After all, some of the most important points of discussion in the relationship between business and ICT centre around the price/quality ratio and the non-transparent nature of the cost structure of ICT services. This will only become more prevalent in mergers and acquisitions if the two ICT organisations evidently offer similar services but use difference (cost) prices and cost management methodologies and/or working methods. Since the business wants to present a united front to clients, it will, in due course, demand the same of its internal ICT service provider(s).

Financial alignment

In order to support the business in creating transparency in the cost of ICT services as much as possible, the ICT function needs to be subjected to financial alignment . The goal is to achieve a uniform pricing methodology and a consistent cost allocation method between the two ICT organisations, and of the two ICT organisations to (internal) customers.

Financial alignment improves the transparency of the different ICT services and makes it a tool for internal (and external) benchmarking (“which organisation offers which service at which price/quality ratio?”), thereby avoiding unnecessary discussions about price comparisons between the two ICT organisations. Generally speaking, the challenge associated with financial alignment is twofold. The costing systems used by the two ICT organisations are probably the most incompatible factor, but cost management tooling tends to differ as well. This hampers comparison and synergy identification, and undermines the need to create a united front to the business.

Roadmap

The level of required change and the road towards the target situation mostly depends on the specific business situation. Generically speaking, the change will have to be implemented over two axes: “similar tooling” and “similar metamodel” (cost management philosophy). The following directions of change can be identified:

1. Similar tooling: if the two ICT organisations have different tools and they opt for one of the cost management tools that is already in place, it is useful, first of all, to align the tooling before creating a shared cost management model (metamodel). The selected tooling then leverages further financial alignment. The advantage of this approach is a quick introduction of the shared tool, thereby avoiding many semantic discussions about the way of working. The two organisations learn from each other because they face the same (im) possibilities in implementing the selected tool. The drawback of this approach is that the benefits for the client (i.e. the business) are not immediately evident, as a result of which it does not instantly offer the required transparency and cost comparison.

2. Similar metamodel: if the two ICT organisations have similar financial governance and cost management philosophy, alignment of the metamodels will prove a useful first step. In parallel with this, synergy benefits within the ICT function (i.e. benchmarking) can then be considered, as well as the selection of a shared (new) cost management tool. The advantage of this approach is the visibility of the change that is reflected in the transparency and comparability of the ICT expenses. This is countered by the fact that some duplicate expenses will be incurred for IT management and that the systems need to be aligned in the event of system changes and model modifications.

3. Full-scope change: if the two ICT organisations should opt for entirely new tooling, it may be useful to kill two birds with one stone and define a new cost management philosophy starting from a greenfield situation. The effect is direct transparency for the client, combined with low cost-of-costing and IT support expenses. This approach also contains the largest change component, however, and has an immediate major impact on the financial function within the ICT organisations.

Behind the scenes at KLM – Air France

After the merger between Air France and KLM, further alignment was planned in three stages: coordination, harmonisation and, finally, integration. So far, the merged businesses have undergone the coordination and harmonisation stages. Air France and KLM are not yet in the integration stage where ICT is concerned.

In order to streamline this process, the companies established a joint FGG (financial governance group), among other initiatives, in which the two IT controllers and the IT strategy and portfolio managers take seat. The shared financial governance principles for the AF / KLM Group are agreed in this committee and then submitted to the ITC (the companies’ IT management teams) for approval. Key areas of focus of the FGG are identifying and managing issues such as: who are our clients? And what IT products and services do we supply? Other focal points are the segregation of innovation and continuity, and the question of how to allocate the costs to clients. In addition, arrangements are made about financial planning: the three-year budget and group forecasting.

One of the most important aspects that AF and KLM are working on is transparency and comparability of processes, costs and pricing (which is referred to as “comparing apples and apples”). This is reflected in an important benchmarking initiative, i.e. the cost management alignment project that the two organisations have initiated jointly. This project is based on a shared tool for cost allocation by products and services, the ultimate goal being a shared metamodel of cost allocation for both ICT organisations. The target of alignment in costing methodologies and tooling will avoid unnecessary discussion about price benchmarking, and will yield cost savings in the future. Furthermore, a shared tool has been selected for forecasting and reporting ICT expenses, so that they become comparable and addable.

In addition to the general principles, agreements have been made in relation to rates and allocation methods between the parties. This applies to joint innovation projects, the use of each other’s joint applications and to joint purchasing alike. It forms the basis of the financial settlement, so that further alignment is encouraged.

The support and endorsement of the selected policy by AF / KLM top management is instrumental in aligning the two IT organisations. This is currently vested in the strategic management committee (SMC). The success of the alignment is contingent on understanding of each other’s culture. Culture is one of the decisive factors in decision-making processes and the way in which changes are digested. The scale and speed of the change processes will be accepted only in close consultation and if they are in alignment. Differences in the role and expectations of the client are crucial in this regard as well.

Key success factors

The following are key success factors (KSFs) for financial alignment:

• Involvement on the part of the business (i.e. the client): the (internal) client needs to be involved in defining the cost management objectives and the way in which they can impact ICT expenses. The client is the most important stakeholder and influencer of the service provision of the IT function, and needs to be given a voice in how to visualise influencing of IT expenses and how to focus on IT cost management.

Focus on the three Cs: Change, Culture (both organisational culture and geographical culture in international mergers and acquisitions) and Communication. From a tooling perspective, financial alignment resembles alignment of two cost management models, but, fundamentally, it marks the beginning of a change in the financial management of the ICT organisation. This requires focus on communication and change management, especially in an international context.

• Alignment with IT governance: recalibration of financial governance is a prerequisite for the success of financial alignment (e.g. IT principles involving charge-out). Therefore, financial alignment directly impacts the overall management and rules of the IT function: IT governance. There needs to be a clear and transparent link between the different focal points.

• Support from senior management: since financial alignment is a lengthy change process with great impact on all those involved, it is crucial that management sponsorship should be clearly anchored throughout the process, both within the ICT organisations and with the (internal) client.

• Benefits tracking: as the goal is to achieve transparency in costs and increase the comparability of ICT services, the effects of drastic financial alignment need to be monitored strictly throughout the process based on a business case. This prevents questions about the effect of, and need for, the proposed change during the project. The ultimate goal is to create transparency in costs and steering options, and these emerge when the change is initiated.

“IT can be a key enabler for successful integration”

Final comments

IT integration issues will be the order of the day in the next few years considering the expected wave of merger and acquisitions. The positive effects of this integration will, however, have to be manifest. Financial alignment within the ICT organisation is an important tool for achieving transparency, cost awareness and focus on the best price/quality ratio of ICT services.

Stay up to date with M&A news!

Subscribe to our newsletter