By KPMG

Introduction

To summarize the French rules applicable to cross-border mergers and acquisitions (M&A), this chapter addresses three fundamental decisions facing a prospective purchaser.

- What should be acquired: the target’s shares or its assets?

- What will be the acquisition vehicle?

- How should the acquisition vehicle be financed?

Tax is, of course, only one piece of the transaction-structuring jigsaw. Company law governs the legal form of a transaction, and accounting issues are also highly relevant when selecting the optimal structure. These areas are outside of the scope of the chapter, but some of the key points that arise when planning the steps in a transaction plan are summarized later in the chapter.

Recent developments

The last major reforms in the area of cross-border transactions are as follows:

- Increase of the corporate income tax surcharge to 10.7 percent (from 5 percent) for corporate taxpayers with annual sales turnover above 250 million euros (EUR), for financial years ending on or after 31 December 2013. This brings the maximum corporate income tax rate to 38 percent (from 36.1 percent).

- Reform of the tax loss rules:

– For fiscal years ending on or before 20 September 2011:

• carry back: 3 years, no value limit

• carry forward: no time limit or value limit.

– For fiscal years ending after 20 September 2011:

• carry back of losses to the profit of the previous year (instead of the last 3 years) and limited to EUR1 million (previously no limit)

• carry forward of losses are limited to 50 percent (60 percent for fiscal years ending between 21 September 2011 and 30 December 2012) of the current year tax profit in a given offsetting year (applicable to the portion of profit in excess of EUR1 million); when losses are carried back, a credit is granted, rather than a refund. The credit may be used in the following 5 years and is refundable in the sixth year.

- Specific thin capitalization rules are extended to bank loans guaranteed by a related party.

- Anti-abuse mechanism for interest expenses relating to the acquisition of participations (Carrez Amendment): Interest expense on the acquisition of equity securities is non-deductible, unless it can be proven that management of said securities is exercised by the French holding company or a French company related to the holding company.

- Anti-abuse mechanism for indebtedness involving related parties: Interest related to loans granted by related parties is only deductible where the lender is subject to income tax on the amount of interest received at a rate of at least 25 percent of the standard income tax (if the lender is a foreign tax resident, the comparison is made with the theoretical income tax that would have been due in France had the lender been a French tax resident).

- Capital gains derived from participation shares (i.e. where the seller holds more than 5 percent of the capital of the subsidiary) are exempt from tax if the participation is held for more than 2 years. However, a lump sum equal to 12 percent (previously 5 or 10 percent) of the gain, which is deemed to represent costs and expenses, is taxed at the standard corporate income tax rate.

- Creation of a 3 percent levy on distributions of dividends (including constructive dividends) and reserves made to resident and non-resident shareholders by both French companies and French branches of foreign companies (with an exception for distributions within tax-consolidated groups).

- Restriction on the deductibility of interest: 25 percent (15 percent for fiscal years starting before 1 January 2014) of net interest expense is not tax-deductible (if the net interest expenses exceed a EUR3 million threshold).

- Extension of the concept of ‘real change of activity’ leading to a forfeiture of the tax loss carry-forwards.

- Tightening of the conditions for the transfer of tax losses in the course of restructuring transactions.

- Transfer taxes applicable to transfers of shares of listed and non-listed SA (corporation) and SAS (simplified joint stock company) are now calculated at the rate of 0.1 percent.

– transfers of shares in a SARL (limited liability company) remain subject to tax at the rate of 3 percent for that part of the price exceeding EUR23,000.

– transfers of shares in companies whose assets are more than 50 percent real estate (société à prépondérance immobilière) are subject to transfer tax at the rate of 5 percent (with no allowance and no cap), regardless of the legal status of the company.

- Implementation of anti-abuse measures aimed at limiting the deductibility of patent concession fees.

- Increase in withholding tax (WHT) rates:

– 30 percent for dividends and other securities income paid to non-residents (75 percent where the seller is located in a non-cooperative country or territory)

– 45 percent for capital gains on substantial shareholdings derived by non-residents (75 percent where the seller is located in a non-cooperative country or territory).

- Increase in VAT rates as of 1 January 2014:

– standard rate: 20 percent (previously 19.6 percent)

– intermediary rate: 10 percent (previously 7 percent)

– reduced rate: 5.5 percent (unchanged)

– super-reduced rate: 2.1 percent (unchanged).

- Reversal of the burden of proof for the application of controlled foreign company (CFC) rules in the case of undertakings controlled by French companies and located in low-tax jurisdictions.

Asset purchase or share purchase

Although an asset purchase may be considered as a more flexible funding option, a share purchase can be more attractive, notably regarding the amount of registration tax and the right to transfer tax losses of the target company. Some tax considerations relevant to each method are discussed later in this chapter.

Purchase of assets

Purchase price

Where several assets are purchased at market prices, there are no statutory rules governing the allocation of the purchase price among the various assets purchased. For depreciation purposes, the contract may allocate a value to each asset transferred, which will be the basis of depreciation.

Transfers between associated parties must normally be made at market value, although market value, being an economic rather than a tax concept, is not defined in the law. The market price generally is the price that an ordinary buyer would agree to pay.

Where the assets are transferred at a price that is lower or higher than their market value, the difference can be qualified as a deemed distribution, subject to the 3 percent contribution on dividend distributions and to WHT where the one of the parties is a non-resident.

Within a tax-consolidated group, if assets are transferred between members at a price that is lower or higher than the assets’ market value, the difference constitutes an indirect subsidy, which is neutralized at the level of the tax-consolidated results. However, such indirect subsidies have to be de-neutralized in the group-taxable results of the financial year (FY) during which either the company that grants or the company that benefits from the indirect subsidy leaves the tax group or the tax-consolidation group ceases to exist.

Goodwill

Under French tax rules, goodwill, which is considered an intangible asset, generally cannot be amortized except by the creation of a provision, subject to strict conditions.

The value of the goodwill is included in the net worth of the company. If goodwill is transferred, it must be included in the recipient company’s accounts.

Depreciation

Most tangible assets may be depreciated for tax purposes, the major exception being land. Rates of depreciation vary depending on the asset. Higher rates are allowed for plant and machinery used in two- or three-shift manufacturing and for assets subject to substantial corrosion or abrasion.

As of 1 January 2005, new accounting rules apply to depreciation. Based on International Financial Reporting Standards (IFRS), component accounting is used for the separate components of an asset, and depreciation is booked component-by-component.

Typical rates are as follows:

- motor vehicles: 20 percent, straight-line method

- plant and machinery: 10 percent to 20 percent, straight-line method

- buildings: 2 percent to 5 percent, straight-line method.

Intangible assets, such as goodwill and securities, may not generally be amortized, but, under certain circumstances, they may be depreciated by way of provisions. However, the acquisition costs of technical processes, patents, patterns and know-how are usually depreciated over the length of their legal or contractual life.

Under French tax rules, patents may be depreciated over a period that is shorter than their period of legal protection but not less than 5 years.

Tax attributes

Under French tax law, it is not possible to transfer liabilities. only assets can be sold. Liabilities may be transferred in a disposal of shares.

Value added tax

In the absence of special rules, the standard valued added tax (VAT) rate is 20 percent (19.6 percent until 31 December 2013).

However, a VAT exemption is applicable where the sale qualifies as a transfer of assets or part thereof within the meaning of French and European Union (EU) law, such as a transfer of a business.

On the transfer of a business, the exemption applies to the disposal, subject to payment, of all the assets constituting the business (i.e. intangible and tangible assets excluding real estate).

The effective transfer of the clientele is necessary to qualify for such VAT exemption. The disposal of an isolated element would then be subject to VAT, unless the element in question is the clientele or real estate, in which case the disposal is usually subject to the transfer tax.

The VAT exemption does not apply to inventories sold alone.

Transfer taxes

In principle, the purchaser pays French registration tax. However, article 1705 of the French Tax Code provides for a joint and several liability of both the purchaser and the seller for the payment of this tax.

The transfer of immovable property is subject to a 5.09 percent registration duty, calculated on the sale price (or the fair market value of the related assets if higher). For transfers occurring between 1 March 2014 and 29 February 2016, this rate can be increased to up to 5.80665 percent, depending on the French department in which the immovable property is located.

In the transfer of a business, the word ‘business’ refers to the French notion of fonds de commerce. From a legal standpoint, a fonds de commerce is an aggregate of business assets, both tangible and intangible, used in a particular business. It consists mainly of a clientele attached to a particular group of business assets. It may also consist of a right to a lease or a specific collection of equipment, tools and merchandise.

Article 719 of the French Tax Code stipulates that the transfer of a business would trigger, from 6 August 2008, the payment of a transfer tax amounting to:

- 3 percent for the portion of the sale price (or the fair market value, if higher) that does not exceed EUR200,000 after application of a EUR23,000 allowance

- 5 percent for the portion of the sale price (or the fair market value, if higher) that exceeds EUR200,000.

The tax is assessed on:

- the intangible assets transferred, such as clientele, goodwill, leasehold rights to the business premises, patents, inventions, trademarks, current contracts (e.g. distribution agreements), licenses and administrative authorizations

- tangible fixed assets, such as furniture and equipment

- tools and supplies.

New merchandise (inventories) is usually not subject to French registration tax or VAT if certain conditions are met (French Tax Code, articles 723 and 257). When these conditions are not fulfilled, the new merchandise is subject to VAT.

Choice of acquisition vehicle

The following vehicles may all be used to acquire the shares or assets of the target company:

- subsidiary

- branch of a foreign company

- treaty country intermediary company

- local holding company

- joint venture

- other special purpose vehicle (such as a partnership).

The choice of the structure can be critical for tax purposes, especially if it is intended to set up a tax-consolidated group.

Moreover, some specific constraints must be taken into account, such as thin capitalization rules (see later in the chapter) as well as the Charasse and Carrez amendment rules.

According to Charasse amendment rule, if a tax-consolidated group member purchases a company outside the tax-consolidated group from shareholders that directly or indirectly control the target company (the notion of control being defined by the French Commercial Code) and the target company becomes a group member, a portion of the group’s financial expenses is not deductible for tax purposes for 9 years, even if no loan is used to purchase the target company.

According to the Carrez amendment rule, the deduction of interest expenses relating to the acquisition of qualifying participations (titres de participation) requires substantiating that those participations are effectively managed by the company holding them or by a company established in France and belonging to the same economic group (subject to conditions). In addition, when the subsidiary can be considered to be ‘controlled’ by another company within the meaning of the French Commercial Code, such a control must be effectively exercised from France. Otherwise, a portion of all the taxpayer’s interest expenses is considered to be non-tax-deductible and must be added back to its tax result. This add-back is made over a period of 8 years, as from the year following that of the acquisition of the qualifying participation.

Local holding company

If profits are to be reinvested in the business or invested in other undertakings carried on by the buyer in France, the buyer should consider incorporating a local holding company to act as a dividend trap. The local holding company would receive the dividends free of tax (i.e. exempt up to 95 percent or even 100 percent in the case of tax consolidation, subject to conditions) from the ventures carried on in France or abroad by the group. However, a 3 percent contribution on dividend distributions is payable by the French distributing company unless the latter and the holding company that receives the dividends belong to the same tax-consolidated group.

In addition, using a French holding company partly funded by debt and forming a tax group with the target could allow the interest paid by the parent company to be offset against the operating profits of the target (subject to thin capitalization restrictions, the Charasse and Carrez amendment rules and the general limitation to interest deductibility). The holding company could reinvest those dividends in other subsidiaries.

Foreign parent company

The use of a foreign parent company to acquire the shares or assets of the target company has important tax consequences for dividend distributions and interest.

Firstly, the French Tax Code stipulates that dividends distributed by French companies to non-residents shall, in principle, give rise to the application of a WHT to be levied and paid to the public treasury by the distributing company. The statutory rate of this WHT is, in principle, 30 percent where the dividends are distributed to legal entities (75 percent where the latter is located in a so-called non-cooperative country or territory). The WHT rate may be reduced under the terms of international tax treaties that have been concluded by France, provided certain requirements are met.

Secondly, according to article 119 of the French Tax Code, which incorporates the EU Parent-Subsidiary Directive, dividends paid by a French company its EU Member State parent company are exempt from WHT when the following conditions are met:

- The parent company and the distributing subsidiary take the form of one of the companies listed in the appendix to the 90-435 EU Directive.

- Both companies are subject to corporate income tax at the standard rate in the EU Member State where they are located.

- The parent company’s place of effective management is in a EU Member State.

- The parent company has held at least 10 percent of the subsidiary’s share capital for at least 2 years (or has committed to hold the participation for at least 2 years).

Thirdly, according to of the French Tax Code (article 235 ter ZCA), dividends paid by a French company are subject to a 3 percent contribution payable by the distributing company.

Finally, the French Tax Code provides that interest paid by French individuals or companies to non-resident entities is, in principle, exempt from a French WHT unless if paid to a so-called non-cooperative country or territory (WHT applies at the rate of 75 percent in this case).

Non-resident intermediate holding company

Most tax treaties signed by France contain provisions designed to prevent treaty shopping. The EU Directive also contains an anti-abuse clause that may apply to non-EU investors who set up an eU investor company for tax purposes only.

Local branch

When profits will be regularly repatriated, it is sometimes desirable to form a branch or use an existing one to acquire the assets of the target company. The remittance of branch profits is subject to a 30 percent special branch profits tax. Tax treaties may provide for a lower rate or exemption from this tax. Moreover, no branch tax is levied within the EU.

French corporate tax is the same for a branch as for a subsidiary and, except for the branch tax, no WHT is levied in France on foreign branch profits. The overall French corporate tax rate is either 34.43 percent or 38 percent (see recent developments).

A French branch of a foreign entity may be the head of a French tax group.

A number of legal and tax issues need to be considered when choosing between a branch and a subsidiary. The main tax issues concern corporate tax. Examples are as follows:

- Head office expenses reasonably attributable to the operations of a branch are, in principle, tax-deductible. The expenses of an exchange of services between a subsidiary and a parent company are only deductible if carried out on an arm’s length basis.

- Branch profits, whether or not remitted to head office, are subject to a 30 percent WHT or branch tax, depending on the relevant tax treaty, although an exemption may be obtained if there is no remittance.

- Branch profits remitted to the head office are also subject to the 3 percent contribution on dividend distributions (see recent developments).

- The profits of a subsidiary are subject to WHT tax only if they are distributed. Dividend distributions made abroad are subject to a 30 percent WHT, which is normally reduced by tax treaties.

- Moreover, there is a WHT exemption on the basis of the EU Directive (discussed in this chapter’s section on foreign parent companies), except where the head office is located in an EU member State.

- Branches generally are not covered by France’s tax treaties and thus cannot usually benefit from them. Subsidiaries are French entities and thus qualify for reductions or exemptions from taxes.

- Branches are not presently entitled to claim a credit for foreign taxes paid, whereas subsidiaries, as residents, may claim a credit for foreign taxes (in particular, WHT).

Joint ventures

Where an acquisition is to be made in conjunction with another party, the question arises as to the most appropriate vehicle for such a joint venture. Although a partnership can be used, in most cases, the parties prefer to conduct the joint venture via a limited liability company. A limited liability company offers the advantages of incorporation (legal existence separate from that of its members) and limited liability for its members. In a partnership, the partners have unlimited joint and several liability for the debts of the partnership.

Choice of acquisition funding

A purchaser using a French acquisition vehicle to carry out an acquisition for cash needs to decide whether to fund the vehicle with debt or equity. The tax implications of the two approaches are discussed later in the chapter.

Debt

The principal advantage of debt is the potential tax deductibility of interest paid to a related party or to a bank in the framework a bank loan.

Deductibility of interest

Generally, interest paid by a company is tax-deductible. However, the French tax rules include an exception concerning the deductibility of interest paid on shareholders’ accounts. Such interest is tax-deductible only if the borrowing company’s capital is fully paid-up (article 39.1.3 of the French Tax Code), and only up to the rate of the yearly average of average effective rates accorded to companies by credit institutions for variable rate loans having an initial duration of over 2 years (article 39.1.3 of the French Tax Code). For the FY ending 31 December 2013, the maximum deductible interest rate was 2.79 percent).

Moreover, French thin capitalization rules apply to any loan or advance between affiliated companies and between sister companies.

Interest paid to a related party should not exceed the interest rate provided for by article 39.1.3 of the French Tax Code. Any excess interest is permanently non-tax-deductible and may be subject to WHT if paid abroad. However, a higher rate is accepted for tax purposes if it corresponds to a rate the French paying company could have obtained from a third-party bank. In this case, the paying company must prove that the interest rate used is arm’s length (e.g. by providing bank offers).

Then it must be determined whether the theoretically deductible interest effectively can be deducted in the financial year of accrual. This would be the case if the paying company is not considered thinly capitalized; that is, where the borrower meets one of the following three ratios:

- the borrower’s intragroup debt-to-net-equity ratio does not exceed 1.5:1 (debt-to-equity ratio)

- the amount of interest does not exceed 25 percent of the current pre-tax result plus intragroup interest and deductible depreciation (interest coverage limit)

- the amount of interest does not exceed the total interest amount received by the French borrower from affiliated entities (received intragroup interest limit).

Whenever the amount of acceptable interest simultaneously exceeds these three thresholds, the excess amount is not immediately deductible, but it can be carried forward over future FYs. the deferred interest is deductible in the following FY (FY + one) if the interest accrued during FY + one does not exceed the interest coverage limit of FY + one. If it does, the deferred interest is deductible only up to the difference between the interest coverage limit of FY + one and the amount of FY + one interest. The part of the deferred interest not available for deduction in FY + one is rolled over, but the amount of the deferred interest is decreased by 5 percent per year as from the second year of carry forward.

Further to the French 2011 Finance act, these French thin capitalization rules apply to all loans that, while borrowed from a third-party company, are guaranteed by an affiliated company, subject to certain exceptions such as, among other things bonds issued under a public offer or pledge on borrowers’ shares.

Affected guarantees include personal safety guarantees (e.g. personal securities, first demand guarantees and even letters of comfort in certain circumstances) and security interests (e.g. pledges of the debtor’s securities, mortgages).

However, the interest limitation does not apply:

- when the borrower proves that the debt/net equity ratio of the group equals or exceeds its own debt-to-net-equity ratio

- to certain financial operations or structures (i.e. group cash pools, credit institutions or goods leased through finance leases) under certain conditions

- when the portion of interest that is not immediately deductible is less than EUR150,000.

In addition, specific rules apply to tax-consolidated groups: generally, a deferred interest is limited to the excess of the interest paid to related (but not tax-consolidated) entities over the 25 percent coverage limit computed at the level of the tax group.

As mentioned earlier, the Carrez amendment rule disallows deductions of interest expenses relating to the acquisition of qualifying participations (titres de participation) that are not managed by the company holding them or by a company established in France and belonging to the same economic group.

Moreover, a general restriction to the deductibility of interest: has been introduced for fiscal years starting on or after 1 January 2014. only 75 percent (85 percent for earlier fiscal years) of the net interest expenses are tax-deductible (unless such net interest expenses are lower than EUR3 million).

Finally, the Finance Act for 2014 introduces a new anti-abuse mechanism for indebtedness involving related parties. Interest related to loans granted by related parties now are only deductible where the lender’s interest received is subject to income tax of at least 25 percent of the standard income tax. (If the lender is a foreign tax-resident, the comparison would be made with the theoretical income tax that would have been due in France if the lender had been a French tax resident).

Withholding tax on interest and methods to reduce or eliminate withholding tax

The corrective Finance Act for 2009 substantially changed the tax treatment of French-source interest arising on financial advances. As of 1 March 2010, the general principle is that French-source interest is exempt from French WHT.

The sole exception to this exemption concerns the interest arising on financial advances granted by entities located in non-cooperative jurisdictions. According to French tax law, non-cooperative jurisdictions are countries and territories that:

- are not EU Member States

- have not concluded treaties with at least 12 different Member States or territories containing a mutual assistance clause allowing for the exchange of information

- have not entered into any such treaty with France. The French tax authorities publish a list of non-cooperative jurisdictions annually.

The interest derived from financial advances granted by entities located in such jurisdictions is subject to a 75 percent French WHT.

Checklist for debt funding

The use of bank debt may avoid thin capitalization, the recently enacted anti-abuse mechanism and transfer pricing problems.

Interest paid by a company in the framework of a bank loan is tax-deductible when some conditions are met.

However, when bank loans are guaranteed by a company affiliated with the borrower, the interest paid to the bank is also subject to the thin capitalization rules.

Moreover, according to the Carrez amendment rule, a portion of interest paid to purchase substantial shareholdings is added back to the tax result when the company cannot prove that the decisions regarding those shares are made by it (or by a French company belonging to the same group) and that the company actually has an influence over the target company.

In addition, for fiscal years starting on or after 1 January 2014, only 75 percent (85 percent for fiscal years opened before 1 January 2014) of the net interest expenses are tax-deductible (unless such net interest expenses are lower than EUR3 million)

Equity

If there is a risk of non-deductibility of interest, it may be better to use equity to fund the acquisition.

Under French corporate law, the capital of a company may be increased to finance the acquisition. This capital increase may result from a cash contribution or from issuing new shares to the seller in satisfaction of the consideration.

From a French registration tax standpoint, increasing share capital by way of a contribution under the apport à titre pur et simple regime (i.e. the sole consideration received in exchange should be new shares issued by the French company) only triggers the payment of small registration duties limited to a fixed registration duty of EUR375 (if the contributed company’s share capital is less than EUR225,000) or EUR500 (if the contributed company’s share capital is equal to or higher than EUR225,000).

Favorable tax treatment for reorganization operations

Mergers

The following comments relating to the restructuring of companies concentrate on mergers. Specific issues arising from dissolutions, split-ups and spin-offs are dealt with separately.

Direct taxes

A merger involves the dissolution of the absorbed company followed by an increase in the capital of the absorbing company.

The absorbed company is taxed at the current rate of corporate tax on the profit and provisions of the financial year (currently 33.33 percent). A 3.3 percent surtax for companies that have a taxable income basis higher than EUR763,000 increases the corporate and short-term capital gains tax rates to 34.43 percent. Moreover, a 10.7 percent surtax applies to companies with a turnover of more than EUR250 million. As a result, the maximum corporate tax rate amounts to 38 percent for those companies.

Long-term capital gains arising from the transfer of substantial shareholdings (held for at least 2 years) are 88 percent exempt. They are thus taxable at the reduced rate of (i) 4 percent (33.33 percent × 12 percent); (ii) 4.1316 percent (34.43 percent × 12 percent); or (iii) 4.56 percent (38 percent × 12 percent).

Short-term capital gains are taxed at the same rates as business profits (currently 33.33 percent, 34.43 percent or 38 percent, depending on the company’s taxable income basis and turnover).

The absorbing company acquires the assets transferred free of tax.

Preferential treatment is available in the case of mergers (article 210 a of the French Tax Code). The principal advantages of this treatment are as follows:

- The absorbed company is not subject to corporate tax on net capital gains on fixed assets transferred in a merger. With respect to intragroup mergers, in principle, assets are contributed on a net book value basis, whether it is an upstream or a downstream merger.

- Where the merger is between unrelated parties, assets are contributed on a fair market value basis, unless it is a reverse merger.

- The absorbing company must include in its own balance sheet the provisions and depreciations made by the absorbed company.

- Capital gains on non-depreciable assets can be exempt from French corporate income tax and are not taxed even if the merger value of these assets is higher than their value in the absorbed company’s accounts.

- If the absorbing company re-sells a non-depreciable asset, it must calculate the capital gain or loss on the basis of the tax value of the asset in the absorbed company’s accounts (rollover).

- If the absorbing company sells the transferred assets, the relevant date for long- and short-term capital gains is the date of acquisition by the absorbed company.

In principle, the absorbed company’s losses cannot be offset against the absorbing company’s profits, except when a special ruling from the tax authorities is granted. this ruling can only be obtained when the merger is carried out under the preferential regime and where certain conditions regarding the transferred activities are met.

Registration tax

Under article 816 of the French Tax Code, the merger of two companies gives rise to a liability to registration tax, paid by the absorbing company at a fixed amount. This amount is EUR375 if the absorbed company’s share capital is lower than EUR225,000 and EUR500 in other cases.

Retroactive effect

Mergers may be given retroactive effect from both an accounting and tax standpoint. However, the merger’s effective date cannot be earlier than the more recent of:

- the first day of the absorbing company’s FY

- the first day of the absorbed company’s FY.

This provision enables the results realized by the absorbed company during the months preceding the effective date of the merger to be offset against the profits and losses incurred by the absorbing company in the same period.

Dissolution without liquidation

Direct tax

According to article 1844-5 of the French Civil Code, the dissolution without liquidation (transmission universelle de patrimoine) of a company owned by a sole shareholder is not followed by liquidation. Instead, it entails the transfer of all the company’s assets and liabilities to the sole shareholder. In accordance with the Finance Act of 2002, the dissolution without liquidation qualifies for the favorable tax regime under article 210 a of the French Tax Code as described above for mergers.

Thus, the tax treatment of a dissolution is the same as that applicable to mergers.

Registration tax

The dissolution of the merged company remains subject to a registration tax of EUR375 or EUR500 (article 811 of the French Tax Code). However, the transfer of real estate resulting from such an operation can be subject to a registration tax of 0.715 percent (article 678 of the French Tax Code).

Retroactive effect

Dissolutions may have a retroactive effect only from a fiscal standpoint. Unlike mergers, retroactive effect is not allowed for dissolutions from an accounting standpoint.

Spin-off

A spin-off (or partial business transfer) is an operation whereby a company transfers part of its assets and liabilities to another company in exchange for shares. the portion of assets transferred must constitute a complete and autonomous branch of activity.

The concept of a complete and autonomous branch of business requires that the collection of assets and liabilities to be transferred are those of a division of a company that constitutes, from a technical standpoint, an independent activity capable of being carried on using the division’s own resources under normal conditions in the economic sector concerned. In short, a complete and autonomous branch of activity is a collection of assets and liabilities of a company’s division able to carry out an activity autonomously.

Regarding direct taxes, under article 210 B of the French Tax Code, a partial transfer is eligible for the favorable tax treatment applicable to mergers if all the following conditions are met:

- The transfer is of a complete and autonomous branch of activity.

- The transferring company retains the shares it receives in exchange for the assets for at least 3 years.

- The transferring company commits itself to calculate capital gains on the sale of shares with reference to the value that the assets had in its own accounts from a tax standpoint.

If one of these conditions is not met, it remains possible to obtain a ruling from the French tax authorities. This ruling may be granted by right if:

- The contribution is based on economic reasons and is not motivated by tax avoidance reasons.

- All guarantees are provided to the French tax authorities that they will subsequently be able to tax the capital gains on which the taxation has been deferred.

Regarding registration tax, the transfer is subject to the favorable treatment provided for in article 817 of the French Tax Code, which limits the registration tax to a fixed amount of EUR375 or EUR500, depending on whether the level of share capital is lower than or equal to EUR225,000.

Split-up

The split-up of a company (scission) is a legal operation whereby all the assets and liabilities of the company are transferred to two or more new companies. The old company ceases to exist and its shareholders receive the shares issued by the new companies. The preferable treatment available for mergers/spin-offs for direct tax can also be applied to the split-up to the extent that:

- The split-up company transfers at least one autonomous branch of activity to each company benefiting from the contribution.

- The shareholders who held at least 5 percent of the split-up company commit to keep the shares of the beneficiary companies or the new company for at least 3 years.

The favorable registration duties treatment applicable to mergers also applies to a split-up without particular conditions.

However, the favorable tax treatments only apply to a split-up within the framework of a reorganization and not to a split-up resulting in equity sharing.

Deferred settlement

Deferred payments under earn-out clauses are subject to the same tax treatment as capital gains or losses realized on the sale.

Other considerations

Concerns of the seller

Capital gains are taxable at the standard French corporate income tax rate subject to the restriction noted earlier. Stamp tax is payable by the buyer.

The seller will mainly be concerned with the indemnities and/or warranties requested by the buyer (usually subject to negotiation).

For companies, capital gains on the sale of substantial shareholdings held for at least 2 years are 88 percent exempt from tax. They are thus taxable at the reduced rate of either (i) 4 percent (33.33 percent × 12 percent); (ii) 4.1316 percent (that is, 34.43 percent × 12 percent); or 4.56 percent (38 percent × 12 percent). If the shares sold do not qualify as substantial shareholdings, the capital gain is taxable at the standard corporate income tax rate of 33.33 percent, 34.43 percent or 38 percent.

For individuals, the capital gain is subject to personal income tax at the progressive rates (up to 45 percent) after application of an allowance of (i) 50 percent where the shares have been held between 2 and 8 years; and (ii) 65 percent where they have been held for more than 8 years (higher allowances exist for shares of small and medium enterprises, subject to conditions). The capital gain is also subject to social contribution at a rate of 15.5 percent (with no allowance). These rules apply for capital gains realized as from 1 January 2013.

If a seller sells all or part of their assets to a buyer who carries on their own business with those assets, the tax authorities may consider that the buyer has purchased the goodwill and may subject the transaction to registration tax at the maximum rate of 5 percent.

Company law and accounting

Types of reorganization

- Merger (fusion) involves the absorption of one company by another company. The absorbing company may be a new company that takes over one or more existing companies, or it may be an existing company that takes over one or more existing companies.

- Split-up (scission) consists of the transfer of all of a company’s assets to two or more existing or new companies. In principle, a split-up involves complete and independent branches of activity.

- Spin-off (apport partiel) occurs when a complete and independent branch of activity of one company is transferred to another company. The spin-off may be made to an existing company or a new company.

- Dissolution without liquidation (transmission universelle de patrimoine) occurs when all shares of a company are held by a single shareholder; it may be decided to dissolve this company, leading to a transfer of all its assets and liabilities to the single shareholder.

- Exchange of shares (fusion à l’anglaise) occurs when a contribution of shares is deemed to be a complete branch of activity benefiting from the favorable tax treatment for corporate tax purposes in three cases:

- where the contribution applies to more than 50 percent of the capital of the contributing company

- where the contribution confers on the beneficiary company a direct holding percentage of the voting rights, when no other partners hold more

- where the beneficiary company already holds more than 30 percent and the contributions give it the majority of the voting rights.

Investment in France

France relaxed its regulations on foreign investment in 1996. In principle, investment in France does not require prior approval from the Exchange Control Authorities. Nevertheless, foreign investment in certain economic sectors connected with public health, public security and public authority must be pre-approved by the Ministry of Finance, based on the fulfillment of certain conditions. The approval is deemed to be granted if, within 2 months of filing a prior authorization, the Ministry of Finance has not opposed the investment.

A Decree dated 30 December 2005 sets out the rules applicable to foreign investments and makes a distinction between foreign investments from an EU Member State and those from a third country.

The following investments from a third country are subject to prior authorization:

- acquisition of control of a French company

- direct or indirect acquisition of all or part of a branch of activity of a French company

- the crossing of the 33 percent threshold of direct or indirect holding of the share capital or of the voting rights of a French company.

When the investment is made from an EU Member State, the prior authorization rule only applies to the first and second types of investment described earlier in the chapter. The need for prior approval also depends on the economic sectors involved. Prior authorization is deemed to have been obtained for:

- investments between companies that are members of the same group, which means that the same shareholder holds more than 50 percent of the share capital or of the voting rights of the entity

- investments made from an EU Member State by an investor that holds more than 33 percent of the direct or indirect shareholding or voting rights and that has already been authorized to acquire control of the entity.

Moreover, some categories of investments in France must be the subject of an administrative report to the Exchange Control Authorities, such as:

- the formation of a new French company by a non-resident

- the acquisition by a non-resident of all or a part of a French company’s branch of activity

- any operation carried out by a non-resident on the share capital of a French company, provided that at the end of the operation the company is owned more than 33.33 percent by non-residents

- the aforementioned operations carried out by a French company, at least 33.33 percent of whose share capital or voting rights are owned by a non-resident

- expansion of the activities of an existing company where the amount at stake is over EUR1.5 million

- acquisition of agricultural land (except for the wine-producing business)

- liquidations of foreign investments in France.

Lastly, some categories of investments must be reported to the Banque de France for statistical purposes, notably:

- any operation between related companies (i.e. loans, deposits, etc.) over EUR15 million

- real estate investments

- acquisition or sale of a French company by a non-resident over EUR15 million

- acquisition or sale of real estate in France by a non-resident over EUR15 million

- liquidations of foreign investments in France.

Note that the aforementioned rules are fully applicable to mergers and takeovers.

Choice of entity for investing in France

Commercial companies are divided into joint stock companies (sociétés de capitaux) and partnerships (sociétés de personnes).

The most frequently used company forms in France are the SA (corporation), the SAS (simplified joint-stock company), and the SARL (limited liability company).

Corporation, Société Anonyme (SA)

- Earnings are taxed once at the corporate level.

- Distributions of earnings are at first subject to a 3 percent contribution payable by the distributing company (unless the distribution occurs within the same tax consolidated group).

- Distributions of after-tax earnings are also taxed at the shareholder level. France reduces the financial effect of taxing corporate profits twice (at the entity and recipient levels) through a 40 percent tax deduction for individual shareholders. There is no deduction for dividends paid to a company. However, if the parent company owns at least 5 percent of the French subsidiary’s share capital and keeps the shares for at least 2 years, the parent company is eligible for the 95 percent dividend exemption provided for by article 145 of the French tax Code. The 5 percent share is taxed at the current tax rate. However, within a tax-consolidated group, dividends are 100 percent tax-exempt as from the second year of tax consolidation.

- Minimum share capital for an Sa is eUr37,000.

- Shareholders have limited liability for the company’s debts.

- There is no maximum number of shareholders (minimum seven).

Limited liability company, Société à Responsabilité Limitée (SARL)

- Minimum share capital is EUR1.

- Minimum number of shareholders is one.

- Maximum number of shareholders is 100.

- The shareholders must give their prior majority approval to the transfer of SARL shares to third parties.

- Shareholders may participate in the management of the company.

- Taxed according to the same rules as an SA.

Société par Actions Simplifiée (SAS)

- Minimum number of shareholders is one.

- Both companies and individuals may be shareholders.

- Minimum share capital is EUR1 (introduced in loi de Modernisation de l’économie-LME, dated 4 August 2008).

- Taxed in the same way as an SA.

- Shareholders have limited liability for the company’s debts.

- Restriction regarding public offering.

General partnership, Société en Nom Collectif (SNC)

- No minimum or maximum capital requirements.

- Minimum of two partners.

- All the partners are jointly and severally liable for the partnership’s liabilities.

- Not taxed at the entity level (unless an election for corporate tax is made).

- Partners are taxed on their share of earnings whether or not distributed.

Limited partnership, Société en Commandite Simple (SCS)

- No minimum or maximum capital requirements.

- Minimum number of shareholders is two general partners (commandités).

- Two categories of partners: general partners (commandités) and limited liability partners (commanditaires).

- General partners are jointly and severally liable for the company’s debts.

- Liability of the limited liability partners is limited to the amount of their contribution to the SCS’s capital.

- General partners are subject to income tax on their share of the SCS’s income whether or not distributed.

- The limited liability partners’ share of SCS income is subject to corporate tax at the SCS level. Dividend distributions to limited liability partners are taxed at their level under normal tax rules.

Limited stock partnership, Société en Commandite par Actions (SCA)

- Minimum share capital for SCA is EUR37,000.

- Minimum number of shareholders is one general partner (commandité) and three limited liability partners (commanditaires).

- General partners (commandités) are jointly and severally liable for the SCA’s debts.

- Limited liability partners (commanditaires) are considered as shareholders and their liability for the SCA’s debts is limited to the amount of their capital contribution.

- Taxed as an SA.

Group relief/consolidation

There is a special tax regime for groups of companies. A French parent company and its 95 percent-owned subsidiaries may elect to be treated as a group so that corporate income tax is imposed on the aggregate of the profits and losses of the group members.

The group may be composed of a parent company holding directly 95 percent or more of all its subsidiaries. A group may also exist if the 95 percent shareholding is held through other subsidiaries. Such subsidiaries can be located either in France or in an EU country (although in the latter case, the foreign intermediary subsidiary is excluded from the tax-consolidated group).

To qualify for group treatment, all the companies must be subject to French corporate tax.

An election for this special regime is made for a period of 5 years. A new company may be included in the group. If a company leaves the group, adjustments must be made, which can be expensive for the parent company.

The group profit is taxed at the standard rate of corporate tax. The group profit or loss is the sum of all the members’ profits and losses.

The advantages of group treatment are as follows:

- Netting of the profits and losses of the companies of the group.

- Double taxation is avoided; consequently, dividend distributions made within the group are exempt from corporate tax as from the group’s second FY.

- Tax neutrality is achieved for transfers of assets and for any transactions within the group (but clawed back if the group terminates or one company leaves the group).

The main drawbacks of the tax group regime are as follows:

- Potential increase in the corporate income tax rate (depending on the group’s overall turnover, the exceptional contribution of 10.7 percent can apply)

- Potential increase in the company value added contribution (CVAE) rate (depending on the group’s overall turnover).

- Potential limitation of the deduction of interest expenses (application of the Charasse amendment rule and appreciation of the EUR3 million threshold at the group level for application of the general limitation of the deductibility of interest expenses).

Transfer pricing

Where the companies involved in a cross-border reorganization have had commercial relationships before the transaction, it may be necessary to review, modify or amend the transfer pricing agreement in force in order to avoid any potential transfer pricing reassessment.

Companies with a turnover or gross assets of over EUR400 million (or companies held directly or indirectly by such an entity by more than 50 percent as well as companies holding directly or indirectly more than 50 percent of such an entity) are required to maintain at the disposal of the tax administration documentation justifying the transfer pricing policy with affiliated companies.

For fiscal years ending as from 30 September 2013, these companies also have to file annually an abridged version of their transfer pricing documentation (within 6 months of the date of the tax return filing).

Foreign investments of a local target company

Profits made by controlled foreign companies (CFC) established in low-tax countries and whose parent companies are subject to French corporate income tax are taxed at the French parent company’s level. This treatment applies where the French company directly or indirectly holds more than 50 percent of the subsidiary’s capital (5 percent if more than 50 percent of the CFC is held either by companies located in France or by companies that control or are controlled by said companies located in France).

However, this measure does not apply if the French parent company can prove that the main effect of the controlled subsidiary’s operations is other than that of locating profits in a low-tax country (which is the case where the subsidiary is engaged in an actual industrial or commercial business in the jurisdiction where its establishment or head office is located).

Further, article 209 B is not applicable to companies established in the EU unless the structure constitutes an artificial scheme that aims to avoid the application of French legislation.

Comparison of asset and share purchases

Advantages of asset purchases

- The purchase price (or a portion of it) can be depreciated or amortized for tax purposes (but not to the extent that it includes goodwill).

- A step-up in the cost base of individual assets for capital gains tax purposes is obtained.

- No previous liabilities of the company are inherited.

- It is possible to acquire only part of a business.

- There is greater flexibility in funding options.

Disadvantages of asset purchases

- Possible need to renegotiate supply, employment and technology agreements, and change stationery.

- A higher capital outlay is usually involved (unless debts of the business are also assumed).

- May be unattractive to the seller, thereby increasing the price. Indeed, in most cases, capital gains derived from the sales of assets are subject to the standard corporate tax rate whereas capital gains on shares benefit from a 90 percent exemption.

- Higher transfer duties (a transfer of goodwill is subject to higher registration tax than a sale of shares of an SA, SAS or SARL).

- Accounting profits may be affected by the creation of acquisition goodwill (at a consolidated level).

- The benefit of any losses incurred by the target company remains with the seller.

Advantages of share purchases

- Likely more attractive to the seller, so the price is likely lower.

- May benefit from tax losses of target company (the target company retains its tax losses).

- May gain benefit of existing supply or technology contracts.

- Transfer duties are quite low.

Disadvantages of share purchases

- Liable for any claims or previous liabilities of the entity.

- No deduction for the purchase price (but interest payable on acquisition financing may be deductible for the purchasing company).

- Less flexibility in funding options.

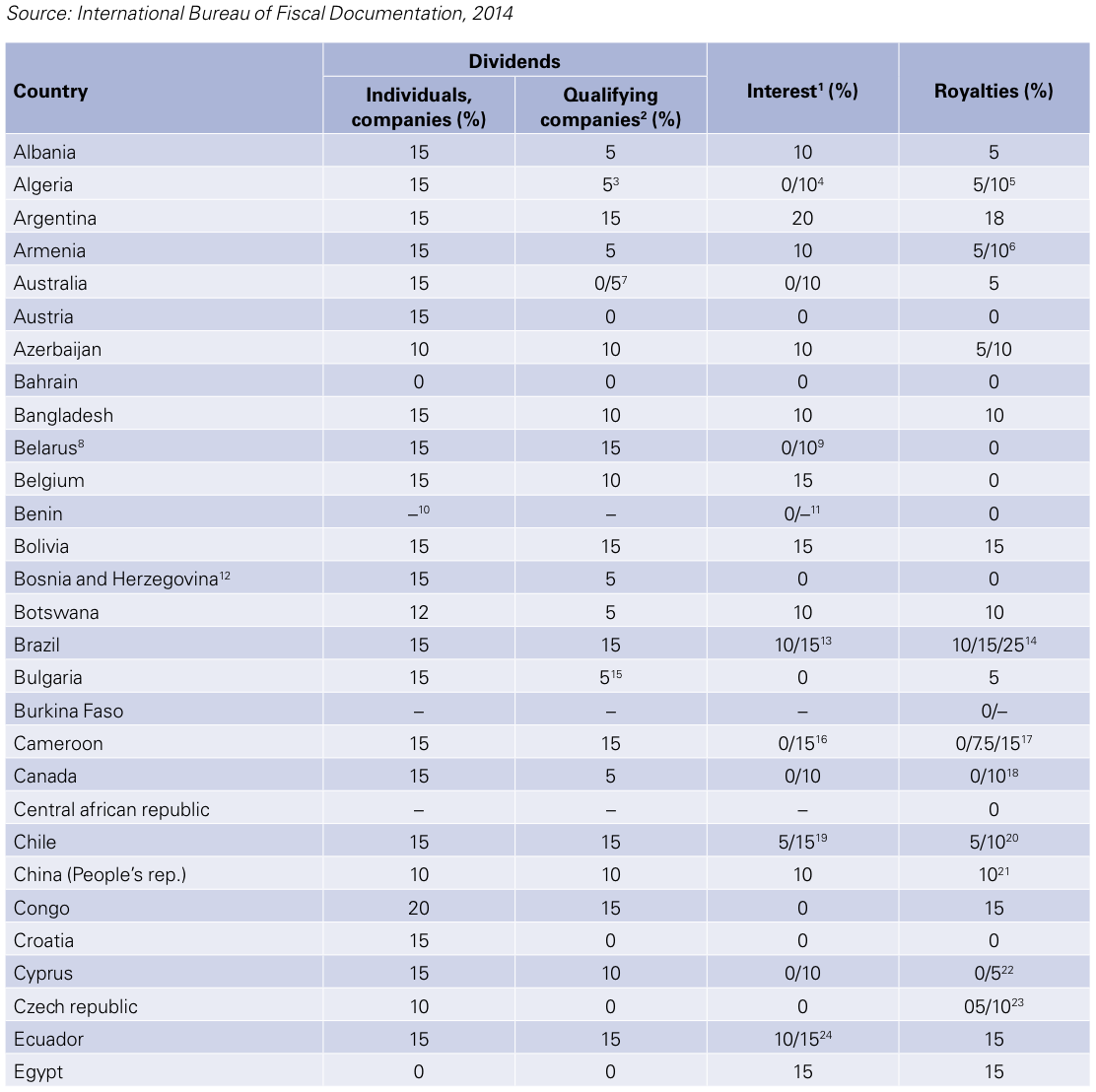

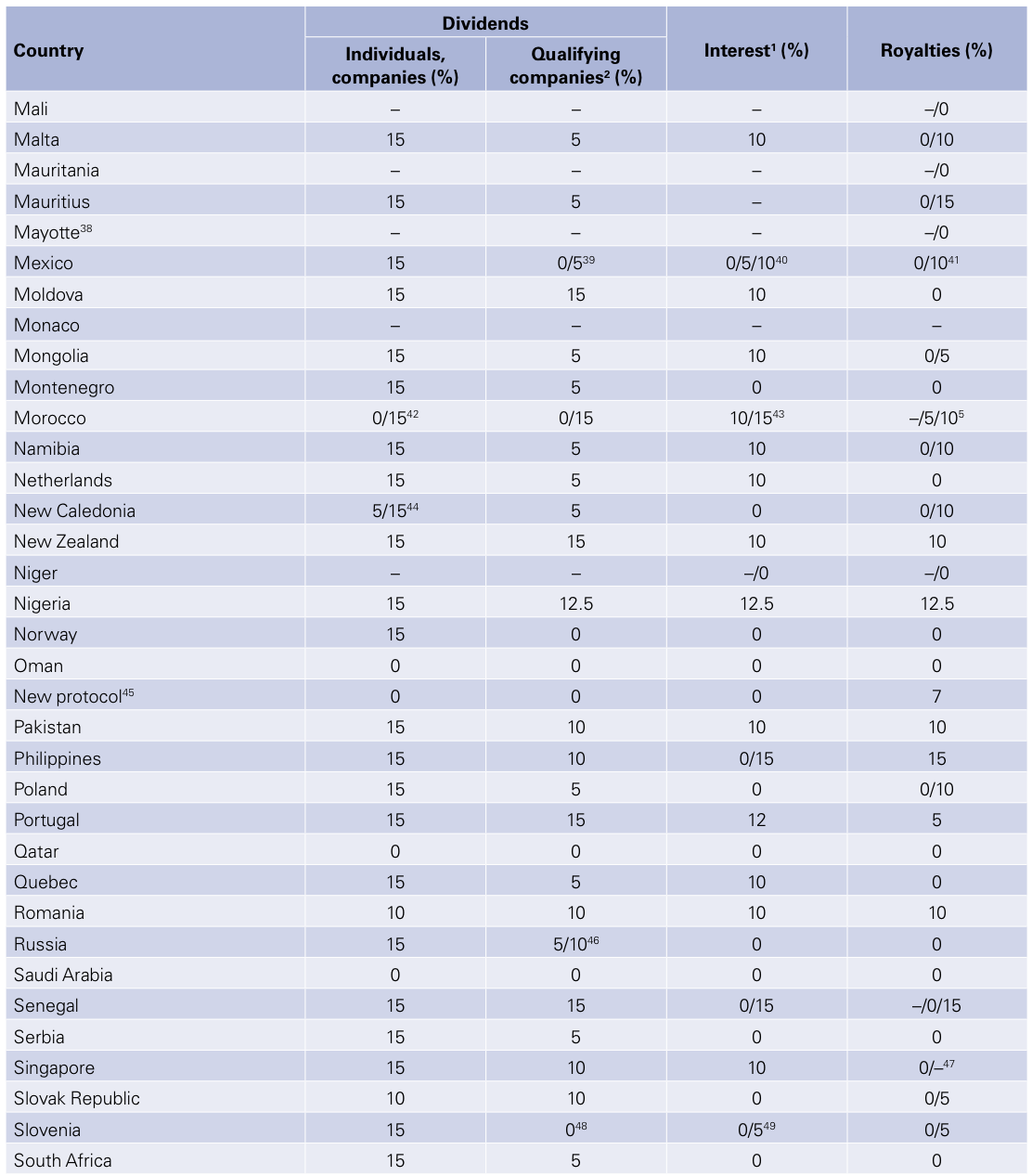

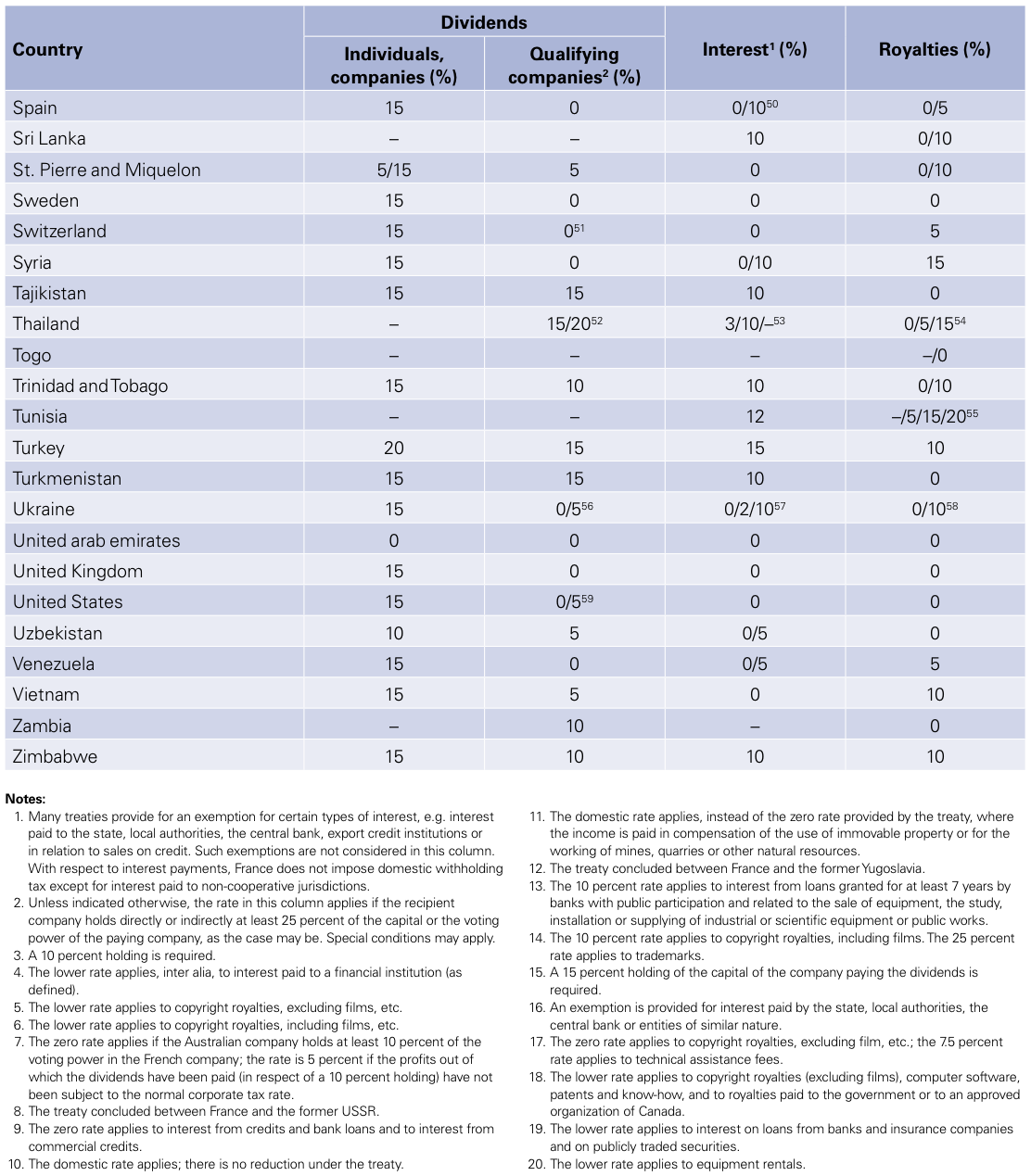

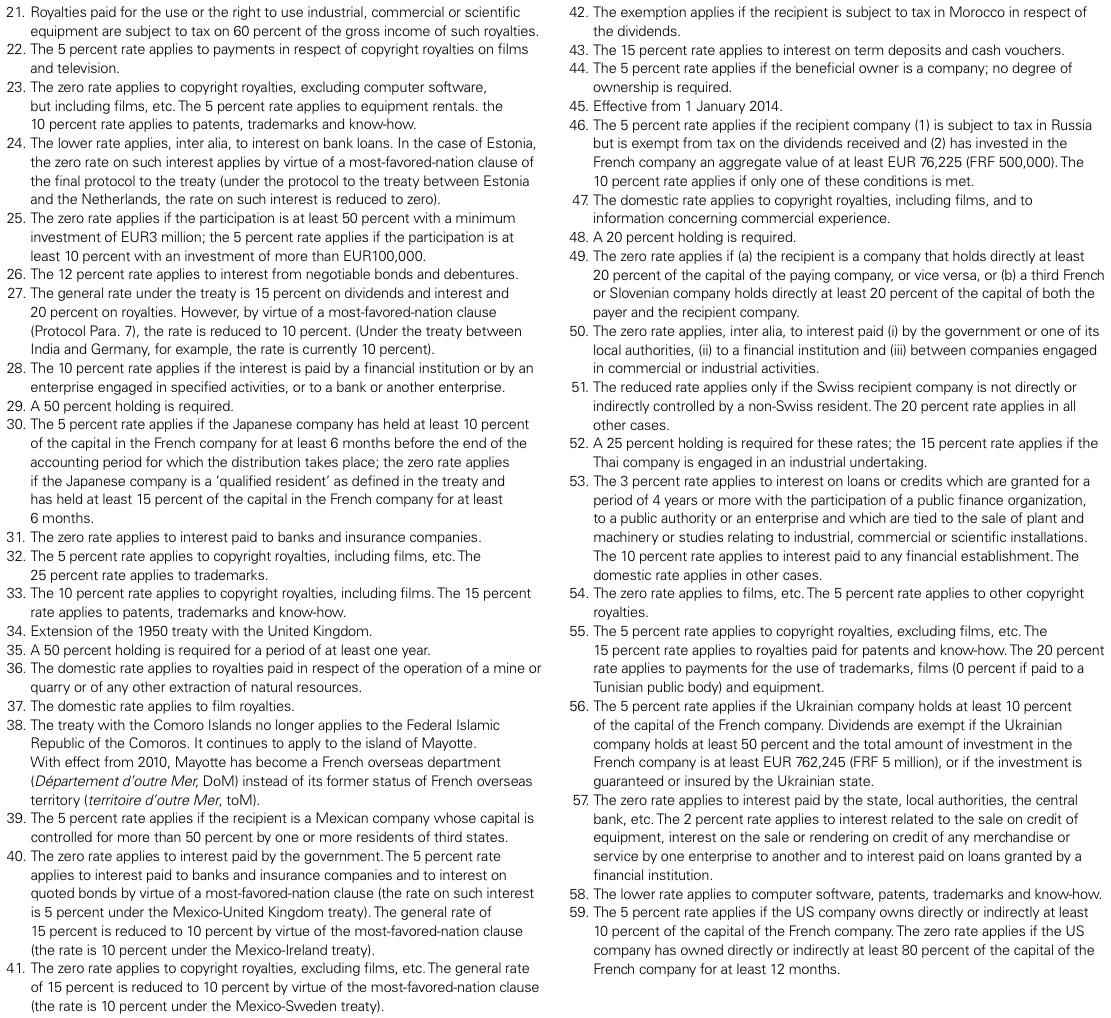

France – Withholding tax rates

France tax treaties. This table is based on information available up to 10 January 2014. This table sets out reduced withholding tax rates that may be available for various types of payments to non-residents under France tax treaties.

Stay up to date with M&A news!

Subscribe to our newsletter