By Deloitte

Banks are on the move

There has been much news about the growth of the emerging market economies, and how institutions in the developed markets are looking to benefit from these fast-growing markets. But the untold story is the reverse; banks based in these markets have been gaining strength, and with that strength, are now looking to expand beyond their borders.

Expansion within their home countries will take emerging markets-based banks only so far, and it provides little diversification when domestic economic volatility spikes downward. That’s one reason why emerging markets- based banks are looking to expand into both developed and developing markets. Emerging markets-based banks are also following their customers, as they expand into new markets, as well as their citizens, as they emigrate to new lands.

As emerging markets-based banks look beyond their borders, the question of readiness arises.

• Are these banks prepared for international expansion?

• What lessons can they learn from banking pioneers that blazed a trail abroad in the 1960s, 1970s, and 1980s?

• And what do they need to do to overcome hurdles of language, culture, talent, regulation, and capital to extend their brands into new markets?

In this report, we address these and other issues with the goal of helping emerging markets-based banks strategize the key steps that they will need to take when considering international expansion.

Trends influencing international bank expansion

As we see shifts in the global economy, banks based in emerging markets are well-positioned for growth within their home markets, and for expansion into new emerging market geographies and developed markets. The banking systems in emerging markets were less impacted by the financial crisis, and as a result, the banks based in them have strong balance sheets — capital which can be invested into growth opportunities. Additionally, the banking systems in emerging markets face common issues including domestic infrastructure and changing demographics. The banks based in these markets have demonstrated that they are well-equipped to innovate and adapt to effectively manage these marketplace issues. We will explore some of these issues below.

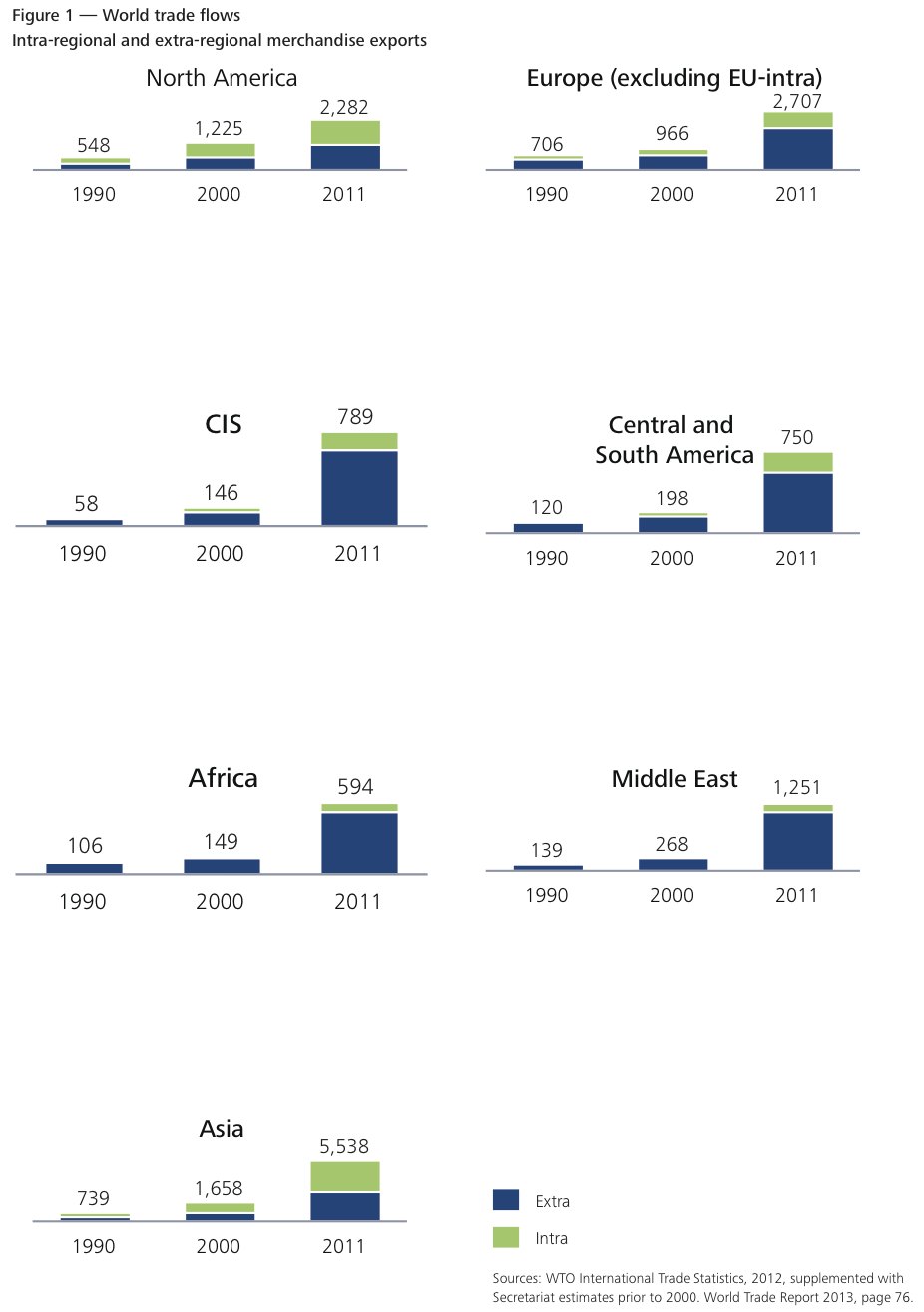

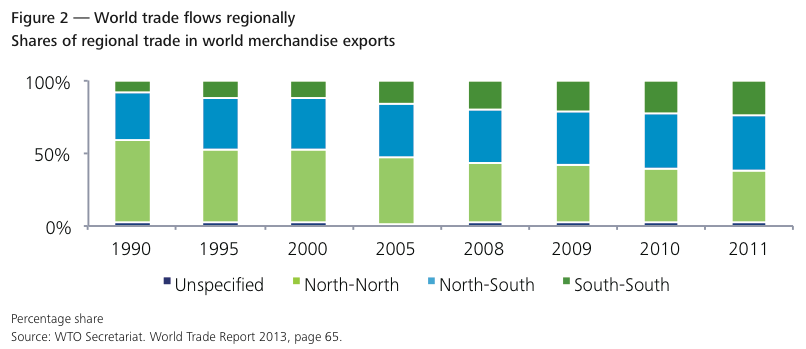

World trade flows. We are seeing an increase in trade flows to emerging markets. Much of this is coming from within the region, as illustrated in Figure 1 and Figure 2, namely in Central and South America and Asia. We have also seen a change in the market share over the last several years, with an increase in South-South trade (emerging market to emerging market). These trends in trade flow reflect and stimulate growth in these markets.

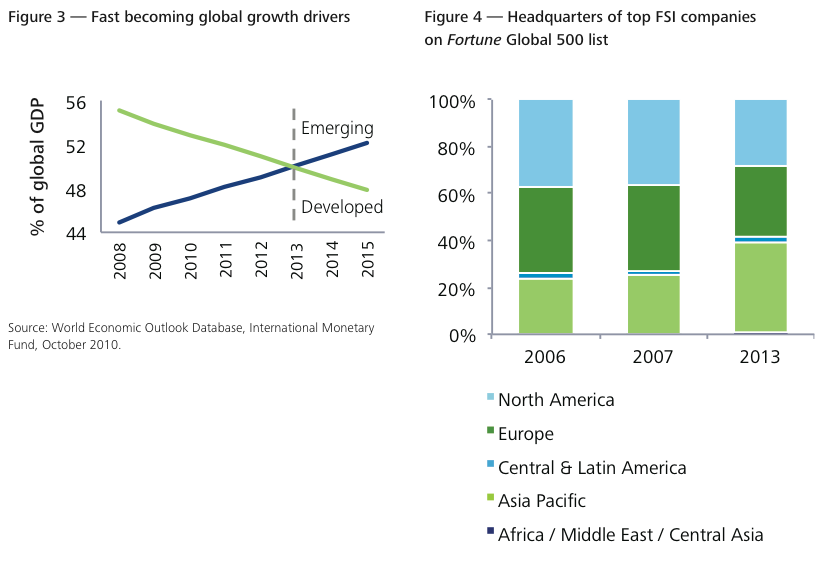

Growing GDP. According to the World Economic Outlook Database and International Monetary Fund, emerging markets and developed markets each account for half of the world’s gross domestic product (GDP) today (Figure 3). Going forward, however, emerging markets will account for more of the global GDP and developed markets will account for less. Emerging markets pose a great opportunity for the future.

Fast-growing companies. Companies based in emerging markets are growing fast and gaining global importance. When looking at the Fortune Global 500 list, which ranks the largest global institutions, the number of financial services firms on the list which are based in North America and Europe has declined, while the number of those based in Asia, Central and Latin America has risen (Figure 4).

Case studies

Mitsubishi UFJ Financial Group, Japan

Following customers to new markets

Mitsubishi UFJ Financial Group (MUFG) is the largest banking group in Japan and the second largest bank in the world, based on assets, according to The Banker’s Top 1000 World Banks ranking for 2013. The Bank has a presence in more than 40 countries and services include commercial banking, trust banking, securities, credit cards, consumer finance, asset management, leasing and financial services.

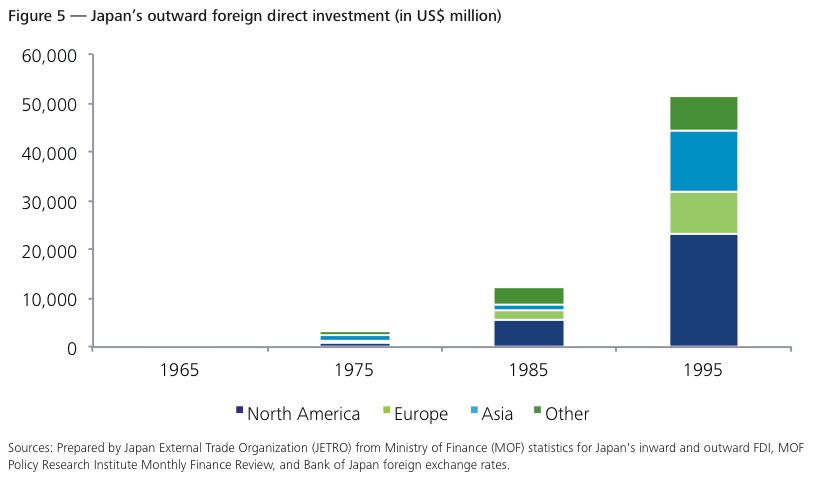

In the 1960s the GDP in Japan was on the rise and we saw production return to pre-war levels. As the manufacturing industry boomed, exports increased, and in the 1980s and 1990s Japan significantly increased their level of foreign direct investment (Figure 5).

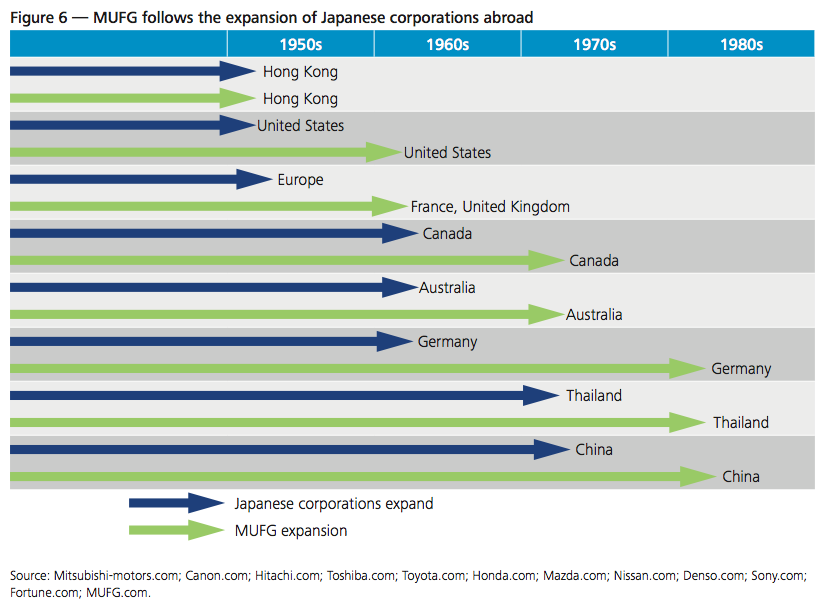

Immediately after World War II, MUFG initially focused its international expansion agenda on the Asia-Pacific region, establishing a presence in Hong Kong in the 1950s, but soon followed its major Japanese customers in electronics, automotive, and other industries as they expanded to the fast-growing mass markets in Europe and North America. MUFG opened offices in France, Korea, the United Kingdom, and the United States in the 1960s; Australia and Canada in the 1970s; and China, Germany, and Thailand in the 1980s (Figure 6). The Bank remains on a global growth trajectory today, recently announcing the close of the acquisition of a controlling stake in Bank of Ayudhya Pcl, one of Thailand’s largest financial institutions. At the same time, MUFG is focused on further strengthening its presence in strategic locations, such as the Americas and Asia.

One of the key lessons that MUFG learned in the early years of international expansion was the importance of having executives work in major business and financial centers, such as London and New York. Such assignments allowed MUFG to demonstrate cultural respect to some of the organization’s largest and most valued customers. Additionally, they also provided executives with high potential for advancement to gain firsthand exposure to the language and culture of markets the organization deemed critical to its future results. Indeed, today, the ranks of senior management at the Bank are filled with executives who completed international secondments earlier in their careers, this helped position MUFG to retain key customer relationships and reinforce strong cultural ties.

Today, when MUFG bankers talk about their overseas success, they cite close ties to local information and culture through an operational structure built around local employees. Strong relationships with governments, information-gathering ability and know-how based on long-term commitment to overseas business are additional strengths. For MUFG, the combination of following customers and respecting cultural ties, along with the integration of local knowledge, has been a key to success. However, the Bank is showing signs of changing its strategy, shifting to a true global management team, more like the well-established western banks which have had a global footprint among their leaders for years. In June 2013 they appointed a non-Japanese executive officer of Bank of Tokyo Mitsubishi, the core Bank subsidiary.

HSBC Holdings plc, United Kingdom

Following customers to new markets; then finding customers in new markets HSBC Holdings plc. (HSBC) is a multinational bank headquartered in London, United Kingdom. According to The Banker, it is the third largest bank in the world based on assets. The Bank operates in 85 countries, with a branch network of 7,200. The organization operates via four primary segments: retail banking and wealth management; commercial banking; global banking and markets; and global private banking.

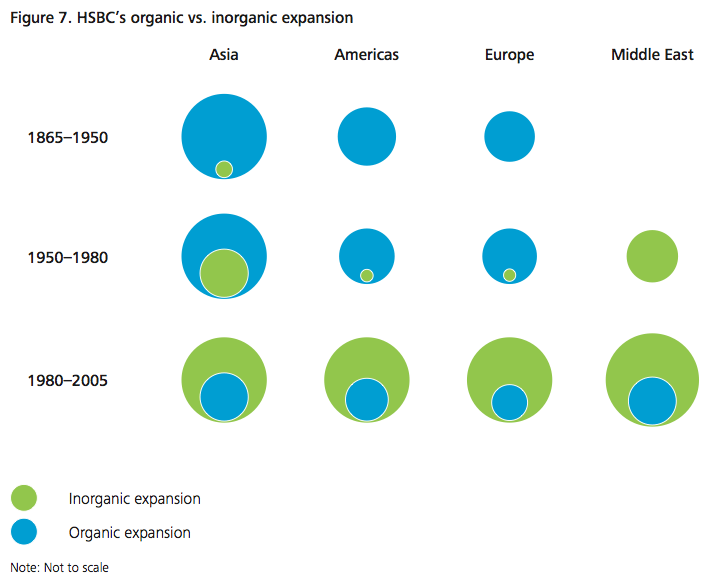

In the mid-nineteenth century, European trading houses handled most of the local business transactions in Hong Kong and other Asia Pacific trading regions. In this context, HSBC was founded in Hong Kong in 1865 to offer local businesses sophisticated banking products.

With the opportunities available in various markets, and the Bank’s competency in financing local trade, within a decade HSBC was financing the export of silk and tea from China, cotton and jute from India, sugar from Philippines, rice and silk from Vietnam, and rubber and tin from Singapore. Through this work, they developed strong relationships with the local governments in these markets. Following their customers, HSBC expanded to major Asian port cities in India, Japan, Philippines, Vietnam, Singapore, Malaysia, Myanmar, Sri Lanka and Indonesia for financing trade. Over time, the Bank began to diversify to support additional industries and enlarged its presence in the Asian market.

HSBC’s financial strength, exceptional client relationships, and regional focus in the Asian markets shielded it from the fallouts of the Great Depression. The Bank maintained its position as the dominant foreign bank in China throughout the 1920s and 1930s, particularly in exchange banking. This was achieved in spite of growing political uncertainty, increasing competition from modern Chinese banks and relatively modest trade growth. However, in 1941, sensing the consequences of another World War, HSBC’s management shifted its head office to London. After the War, in 1946, the head office of HSBC was shifted back to Hong Kong, reconfirming their focus on the region.

After a long period of focusing on Asia, HSBC was beginning to feel the effects of a changing economy and political landscape in the region. In the 1950s they began the withdrawal from China, leaving only one branch in Shanghai. With these changes, the Bank decided to pursue an inorganic strategy and look westwards for growth. They acquired Chartered Mercantile Bank, headquartered in India, and The British Bank of Middle East in 1959. The Bank looked to the Middle East as the next frontier, due to its proximity to the Asian markets and its untapped potential, as foreign banks had minimal presence in the region.

In the 1970s management proposed a “three legged stool” strategy for expansion. The first “leg” was Asia, which was already in place. The second “leg” was the U.S. with the acquisition of 51 percent of Marine Midland Bank in the U.S. in 1980s, and thirdly, in 1992, they purchased Midland Bank in the UK. These initial expansion efforts into these key markets helped to build the Bank into the global player they are today.

Today there is no denying the fact that HSBC is one of the world’s most global banks, with strong fundamentals, excellent client relations, and a true global presence. Their success is due to their focus on client needs and on marketplace opportunities, both while maintaining their fundamental core strength — management, financials, relations with government, and strong reserves.

Today, the Bank’s objective is to become the world’s leading international bank. They are still focused on their roots — looking to capitalize on the trends in international trade and capital flows, as well as economic development and wealth creation in the emerging economies.

Bank expansion today

Over the last several decades, emerging markets-based banks have followed different paths in expanding their reach around the world.

Some of these banks have taken a regional approach to expansion, leveraging synergies that proximity to their home countries offer, while others have established a presence thousands of miles from their headquarters. Consider these examples we see today:

Bank of China, China

Bank of China is the only Chinese bank to be classified as a systemically important financial institution by the Financial Stability Board and has the largest overseas network among its domestic peers. Traditionally a commercial bank, Bank of China has diversified into investment banking, asset management, insurance, aircraft leasing and other financial services through its subsidiaries. The Bank registered a net income of US$30 billion in 2012 over an asset base of US$2 trillion.

Bank of China refers to itself as “China’s most international and diversified bank” and operates in 36 countries. At the end of 2012, total overseas assets for Bank of China were US$498.9 billion, an increase of 13.3 percent from the prior year-end, accounting for 23.5 percent of total assets. Xiao Gang, Chairman of the Board of Directors of Bank of China, published a letter to shareholders in July 2012, explaining why the Bank must go global: “There is good reason to believe that the Chinese economy has reached a point where its status as the biggest country will lead it to become the biggest in outbound direct investment. This new model not only requires Chinese enterprises to expand their global businesses, but also China’s banking sector to accelerate its internationalization.”

Sberbank Rossii, Russian Federation

Sberbank of Russia is the largest bank in Russia and CIS, with a history going back 170 years. The founder and principal shareholder is the Central Bank of Russia, which owns 50 percent of the Bank’s authorized capital and one voting share. The rest of the shares are held by international and domestic investors. The Bank offers the full range of retail, corporate and investment banking services across CIS, Europe and Turkey through its branches and subsidiaries. Net profit for the year ending 31 December 2012 US$9.91 billion over an asset base of US$422.72 billion in 2012.

Sberbank has predominantly taken the acquisition route to enter new markets. In 2011, Sberbank undertook various projects to integrate the subsidiary business into its unified systems. The projects were intended to benefit the customers of its group companies as well as to standardize the underlying processes in each of these companies.

To date they are focusing on expanding to the west, in 2012 Sberbank bought Denizbank, a private bank in Turkey. In October 2013 the Bank increased its stake in a joint venture with BNP Paribas in Cetelem Bank, a Hungary-based bank, taking 74 percent stake.

In a list of strategic goals for 2014 the Bank lists “gradually expand international business through operations in the CIS and Eastern Europe, and build a presence in China and India. ” The Bank reported that international assets make up 12 percent of total Group assets and around 7 percent of profits. Sberbank is present in 22 countries.

Are you ready for global expansion?

Emerging markets-based banks can take the first step toward expansion into developed and developing markets by assessing their readiness along the following dimensions:

Strategy. Understand what market segments you want to pursue. According to a recent study published by the World Economic Forum, three areas afford the greatest opportunities in emerging markets – consumer financial services, small and medium enterprises, and corporate bond markets. But other opportunities exist as well. Emerging markets-based banks need to be focused, yet agile enough to adjust their strategies to assess and capitalize on unanticipated opportunities.

Execution. After defining a clear strategy for international expansion, emerging markets-based banks should focus on how they intend to implement their plans. In many developing countries, alliance with an established local firm is almost a requirement for market entry; in others, foreign banks are allowed to establish representative offices, branches, and/or subsidiaries. Additionally, a number of governments provide support and incentives for their banks to expand internationally, recognizing these opportunities and building them into a plan gives greater chance of success.

Infrastructure. Having adequate technology and business systems is an essential ingredient for international expansion. In some emerging markets, infrastructure resources — ranging from reliable transportation to sources of electricity — are scarce or limited. Business systems need to address these limitations to ensure that customer records and transactions have adequate capacity and protection.

Talent. One of the most critical resources that emerging markets-based banks will need when expanding into developed and developing countries are human resources. The war for talent that many organizations face in their home markets is even fiercer abroad, where companies from many industries — not just financial services — are vying for people who understand the culture, language, and business practices in emerging markets. A bank with a reputation for growth and the ability to offer international assignments is more likely to attract top talent within their domestic markets as well. The best strategy can fail if companies lack commensurate talent.

Regulation. Understanding the nuances of local regulatory regimes is another key element for effective international expansion. Banks that expanded abroad three and four decades ago did not face the level of regulatory scrutiny that banks today face. Developing relationships with local regulators as well as a detailed knowledge of local regulations are important steps for emerging markets- based banks to take. Banks need to also understand the regulations they will face in their home country due to expansion plans.

Capital. Having adequate capital to operate in emerging markets is another requirement for international expansion. Although many emerging markets-based banks came out of the recent global economic crisis in fairly good shape, regulators everywhere expect domestic and foreign banks to meet heightened capital standards. Emerging markets must be prepared to meet these standards for decades, not just years.

Conclusion

Starting the journey to global growth

The decision to expand into developed and/or developing countries is an important one for emerging markets-based banks to consider.

Emerging markets-based banks are in relatively good shape, having avoided many of the issues that banks in developed countries faced during the global economic crisis. Some observers argue that emerging markets-based banks face a window of opportunity for international expansion. If larger banks in developed countries decide to pursue growth in the developing world, how long will that window remain open for emerging markets-based banks?

Emerging markets-based banks are uniquely positioned to prosper in developing countries. They already know how to reach the unbanked and underbanked segments in their own countries; this knowledge is an asset that can translate into other countries and cultures. In addition, emerging markets-based banks have experience operating in often-volatile home markets. This experience can carry over to other developing countries as well.

By taking stock of their capabilities, sharpening their strategic focus, and recognizing that international expansion is a journey, not a footrace, emerging markets-based banks can pave an effective path to future growth in other developing countries.

Stay up to date with M&A news!

Subscribe to our newsletter