Blog Webinar Recap: How to Value Small and Medium Enterprises

- Blog

Webinar Recap: How to Value Small and Medium Enterprises

- IMAA

SHARE:

In the Institute for Mergers Acquisitions and Alliances’ webinar on How to Value Small & Medium Enterprises, experts from Valutico – Greg Brown, Alex Harris, and Max Lahrmann – delved into the pivotal role of small and medium-sized enterprises (SMEs) in fostering economic growth and sparking innovation. The discussion brought to light the unique challenges and methodologies in valuing these vital yet often overlooked components of the economy. Continue reading to learn about the key takeaways from the webinar, including why SME valuation is essential, the discrepancies between theory and practice, and specific considerations unique to SMEs.

Key Takeaways on Why We Need SME Valuation

The webinar highlighted several key reasons why valuations are crucial for small and medium enterprises (SMEs), noting that these businesses differ significantly from larger, publicly traded companies. Here are the main points:

- Transaction or Negotiation Purposes: Valuations play a critical role when an SME is about to be sold. A favorable valuation can significantly strengthen a company’s position during negotiations, providing a solid backing for its asking price or terms.

- Financial Reporting: For official matters like financial reporting, including purchase price allocations and impairment testing, SME valuations are essential. Accurate valuations ensure that financial statements reflect the true value of the enterprise.

- Taxation Purposes: Valuations are integral to various tax-related processes, such as inheritance tax calculations, capital gains assessments, and the valuation of share options. This is also relevant in forensic situations, where an in-depth investigation of a company’s value is required.

- Determining Fair Value: Establishing a fair value for an SME is crucial for multiple stakeholders, including investors, owners, and potential buyers. This helps in making informed decisions based on the true worth of the business.

- Company Succession: In the context of company succession, understanding the valuation of an SME is vital. It ensures that the transition of ownership, whether within a family or to external parties, is based on a fair and accurate valuation of the business.

These reasons, while sometimes overlapping with those of larger companies, are particularly pertinent for SMEs and are a daily aspect of the world of valuation.

Key Takeaways on the Discrepancy Between Theoretical Discussion and Practice

The webinar delved into the noticeable discrepancies between traditional valuation theories and their application to small and medium enterprises (SMEs). The key points discussed were:

- Theoretical Focus on Large Public Companies: Traditional valuation theory primarily focuses on large, publicly traded companies. This includes access to abundant data, transparency, and operating in an optimized market.

- Data and Market Differences in SMEs: In contrast, valuing SMEs often involves different scenarios. These enterprises may not have the same level of data availability or market optimization as larger companies.

- Capital Asset Pricing Model (CAPM) and Portfolio Theory Limitations: While these models aim to determine an objectified value, they are generally tailored for situations involving larger entities with diverse asset portfolios.

- Owner Involvement in SMEs: A unique aspect of SMEs is the strong involvement of the owner, who, in many cases, is synonymous with the company, especially in single-person enterprises. This leads to a lack of diversification and a different risk profile compared to larger companies.

- Management’s Role and Investment: Often in SMEs, the management is not independent but deeply involved with personal stakes in the company. This can impact the valuation due to the intertwined nature of personal and business finances.

The session highlighted that while traditional valuation models provide a foundation, applying them to SMEs requires consideration of these unique factors.

Key Takeaways on the Specifics of SMEs

The webinar explored distinct characteristics of small and medium – sized enterprises (SMEs), highlighting how these differ from larger companies and significantly influence their valuation. Understanding these specifics is key in accurately assessing the value of an SME. The discussion was segmented into three primary areas: Organization and Management, Financial and Legal Aspects, and Reporting and Planning.

Organization and Management

The webinar highlighted the unique aspects of organization and management within SMEs, which differ significantly from larger companies. These differences impact the valuation of SMEs in several ways:

- Management as a Key Asset: In SMEs, management often constitutes the highest asset of the company. Unlike larger companies, management in SMEs, especially in family businesses, is usually irreplaceable. This leads to a unique risk profile, where the business’s continuity can be heavily dependent on the owner.

- Risk in Key Personnel: Key persons are usually the owners or certain individuals and there is risk when they fall out.

- Employee Composition: Employees in SMEs often come from the owner’s friends and family circle, unlike larger companies that typically have a more diversified employee pool. This factor can introduce additional business risks.

- Management Compensation: In SMEs, management compensation and business payouts are sometimes intertwined, which can complicate financial assessments.

- Public Listing Status: Most SMEs are not publicly listed. If they are, they represent a unique situation, as they may not be traded regularly, making them incomparable to publicly traded companies of different sizes.

Financial and Legal Aspects

The webinar also covered the financial and legal peculiarities of SMEs, which play a crucial role in their valuation. These aspects are often distinct from what is observed in larger enterprises:

- Legal Structure Choices: Entrepreneurs often choose their legal structures based on tax considerations, which can sometimes lead to unfavorable positions when selling these businesses.

- Asset Differentiation: The distinction between company and private assets is often blurred in SMEs. Examples include shared use of properties or vehicles for both personal and business purposes, complicating the valuation process.

- Non-Standard Financing Structures: Many SMEs have unconventional financing structures, like subordinated loans or private guarantees, posing challenges in determining their true value.

Reporting and Planning

Focusing on reporting and planning, the webinar addressed how these processes in SMEs are often distinctly different from those in larger companies, impacting their valuation:

- Tax-Driven Reporting: Reporting in SMEs is often driven by tax considerations. In some cases, there may be no reporting at all, making valuation difficult due to a lack of data.

- Experience-Based Planning: Unlike larger corporations, which are often number-driven, many SMEs plan based on experience, lacking a robust mid or long-term plan. This approach can make it challenging to predict the company’s future trajectory.

- Unusual Transactions and Employment Forms: SMEs sometimes engage in non-market usual transactions and have different forms of employment contracts, such as service contracts, which are more common than in larger companies.

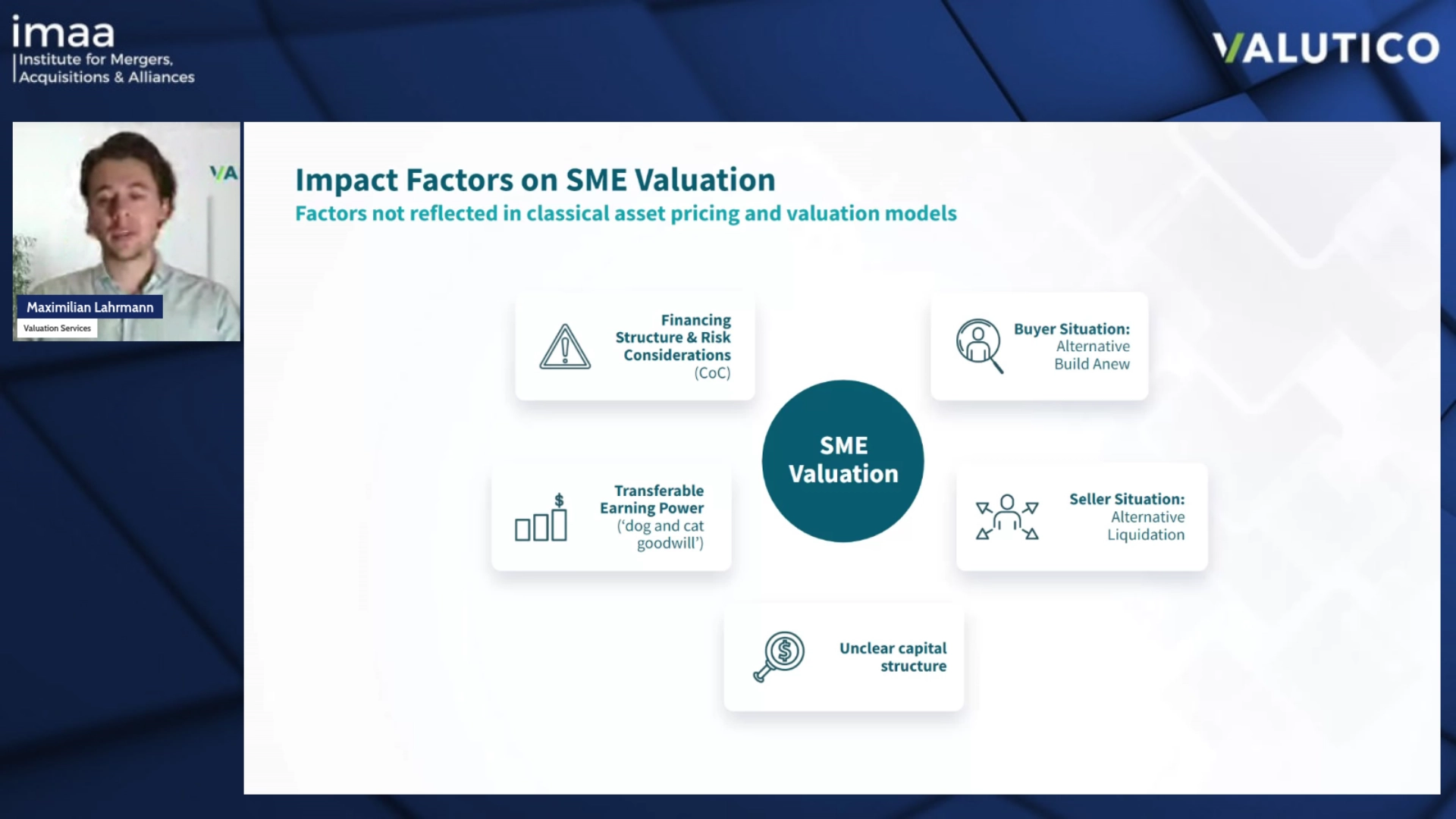

Key Takeaways on Impact Factors on SME Valuation

The webinar provided key insights into the practical challenges and factors impacting the valuation of SMEs. Here are the points discussed:

- Buyer Situation: The process of buying an SME is considerably more complex than purchasing shares of a publicly listed company. This complexity and the significant investment required reduce the pool of potential buyers, as not everyone has the necessary capital or network for such a transaction.

- Seller Situation: Selling an SME presents unique challenges. For asset-heavy SMEs, owners might consider liquidation as an alternative to selling, as it could potentially yield a similar financial outcome but with a more straightforward process.

- Unclear Capital Structures: Often, SMEs have unclear capital structures and a lack of transparency, leading to difficulties in valuation due to inadequate data.

- Transferable Earning Power and Goodwill: The concept of ‘dog and cat goodwill’ was mentioned, highlighting the importance of transferable earning power in the valuation of SMEs.

- Financing Structure and Risk Considerations: The webinar stressed the importance of considering the financing structure and associated risks. SMEs typically face higher risks, influencing factors like cost of capital and discount rates. The ability of SMEs to borrow capital under favorable conditions is often more limited compared to large conglomerates, impacting their financial valuation.

These factors collectively underline the complexity and unique challenges in SME valuation, emphasizing the need for tailored approaches and careful consideration of these distinct aspects.

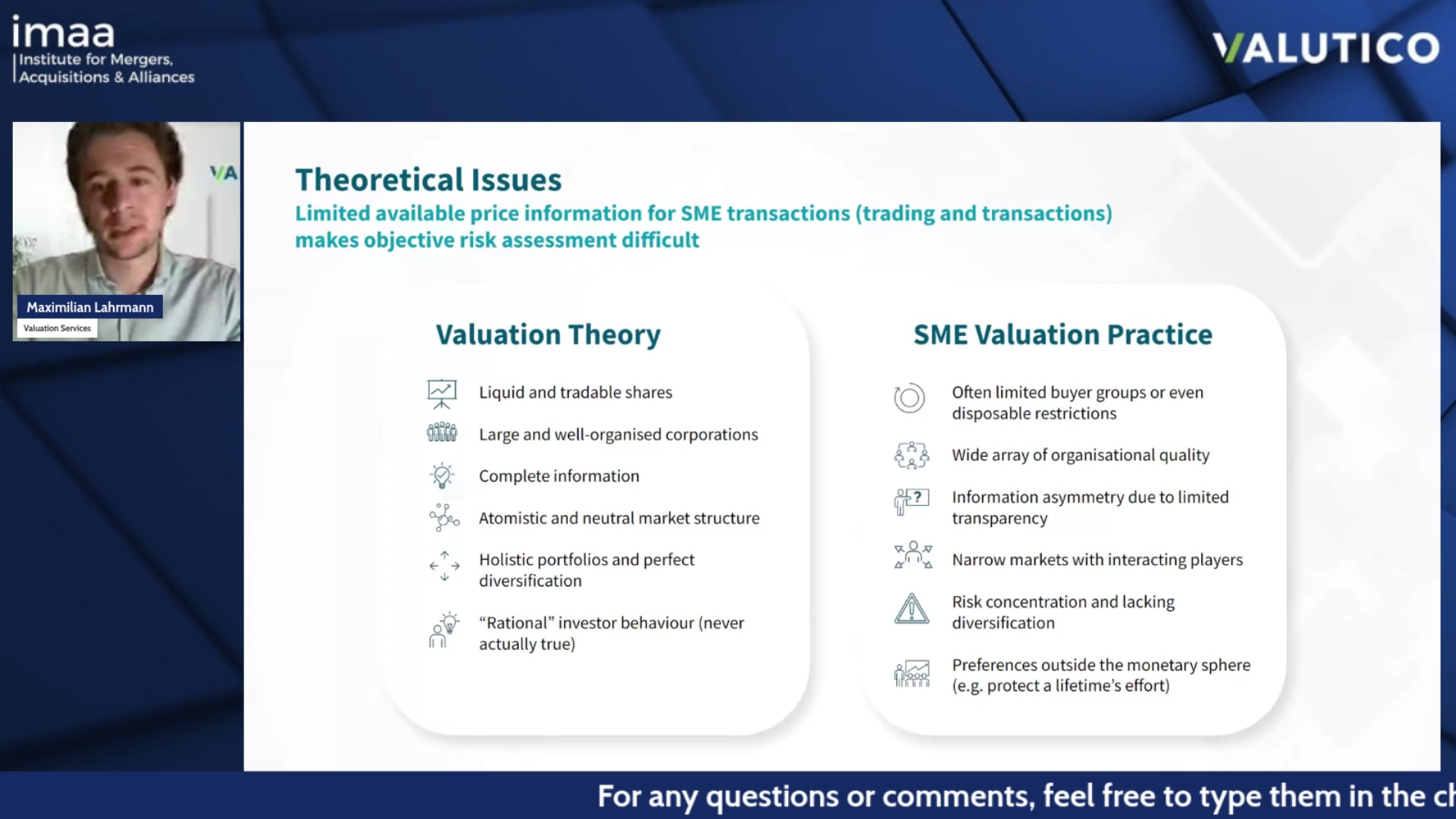

Key Takeaways on Theory vs Practical Approach in Valuing SMEs

The webinar contrasted theoretical valuation models with practical approaches in the context of SMEs, highlighting several key differences:

- Ideal Market Conditions: Valuation theory typically assumes liquid and tradable shares, easy transfer of information, and large, well-organized corporations. In this idealized environment, data is complete and perfect, markets are neutral and optimistic, portfolios are diversified, and investor behavior is rational. This theoretical framework allows for a direct focus on valuation processes.

- Practical Challenges in Valuing SMEs: In reality, valuing SMEs involves unique challenges that deviate significantly from theoretical assumptions.

- Limited Buyer Groups and Disposure Restrictions: Unlike buying shares in large companies, investing in an SME requires a strong network and capital position. The market for SMEs is far less transparent, making the process more complex.

- Organizational Quality and Risks: There’s often uncertainty about an SME’s organization and potential risks, which are not easily discernable during due diligence.

- Information Asymmetry: Due to limited transparency, there is often an imbalance in information available to buyers and sellers, complicating negotiations.

- Narrow Markets with Interacting Players: The market for SMEs can be not as transparent, affecting both buyers and sellers and presenting unique challenges.

- Risk Concentration and Lack of Diversification: As previously mentioned, SMEs often have a dependency on the owner or managing director, leading to a risk concentration and lack of diversification.

- Preferences Beyond Monetary Considerations: Contrary to the rational investor model, SME owners often view their business as more than a financial asset. Emotional attachment to the business, seen as a lifetime effort, can influence negotiations and valuations, challenging the idea of a purely financially driven decision.

In summary, while theoretical valuation models provide a structured framework, the practical valuation of SMEs requires navigating a more complex and less predictable landscape, with emotional, organizational, and market factors playing significant roles.

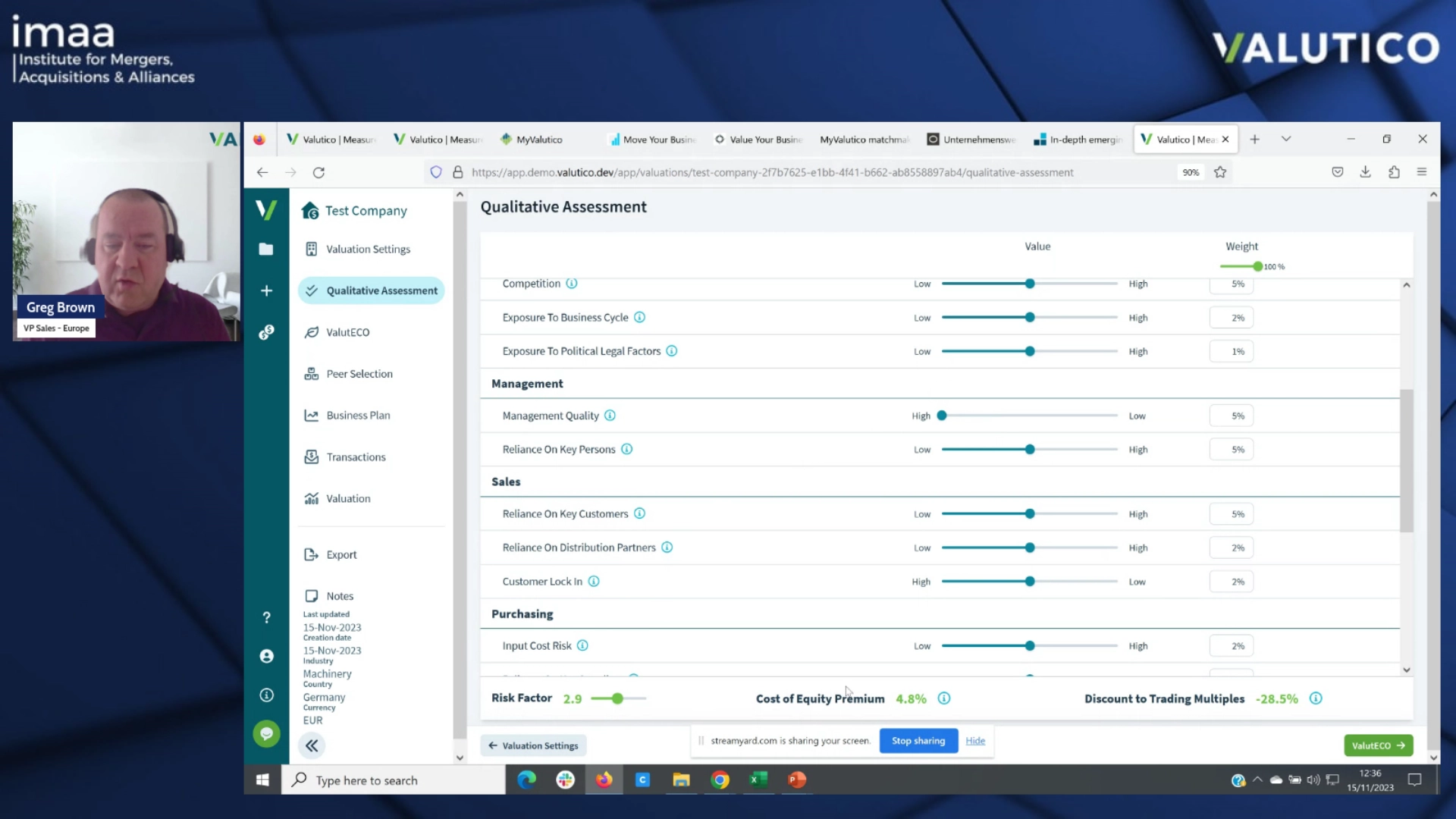

Case Study: Valuing a Machinery Company

A practical case study was also presented during the webinar illustrating the application of SME valuation theories and methodologies in a real-world context. This case study focused on valuing a machinery company, utilizing the advanced capabilities of Valutico’s cloud-based valuation platform. The demonstration provided a step-by-step guide on how to leverage the software for comprehensive SME valuation, underscoring the blend of theory and practice in the valuation process.

The Valuation Process:

The valuation process using Valutico’s software involves several key steps:

- Initial Setup: Adding the company’s name, selecting the home market and industry sector. For better accuracy, it’s suggested to choose a listed peer that closely resembles the business activities of the SME.

- Qualitative Assessment (Risk Assessment): Correcting the shortcomings of traditional models like CAPM, this step involves assessing factors like company size, market positioning, competition, and management quality. It impacts the cost of equity premium and the liquidity discount.

- ESG Module (Optional): For larger businesses impacted by sustainability issues, an ESG module with a questionnaire can be used to affect the cost of capital allocation and discount rate.

- Peer Selection: Identifying relevant peers for benchmarking, using filters to refine the search, and ensuring the peers align with the company’s product/service line and market.

- Financial Data Input: Incorporating historical and projected financial data, with options for manual input or using industry estimates.

- Transaction Data Review: Reviewing and selecting relevant transaction data, with an option to supplement market data with additional transactions.

- Final Valuation and Presentation: Presenting valuation results using various methodologies, with options for customizations and adjustments based on professional judgment.

Key Insights from the Case Study

The case study provides key insights into the practical aspects of using advanced valuation software for SMEs. It emphasizes the need for a comprehensive understanding of both qualitative and quantitative factors influencing SME valuation. The insights highlight the software’s flexibility and depth, showcasing how technological integration can streamline the valuation process while ensuring accuracy and offering diverse customization options.

- Customization and Flexibility: The platform allows for customization and flexibility in selecting peers, financial data, and valuation methods.

- Practical Challenges: The demonstration highlights the practical challenges in SME valuation, including data collection, peer comparison, and dealing with qualitative factors.

- Technology Integration: The use of a cloud-based platform illustrates how technology can streamline and enhance the valuation process.

Encouragement to View Webinar to See the Full Demonstration

To fully grasp the intricacies of valuing an SME using this software, it’s highly recommended to watch the full webinar. The webinar not only demonstrates the valuation process step by step but also provides insights into how to navigate the platform effectively. It’s a valuable resource for anyone interested in SME valuation, offering a practical perspective that complements theoretical knowledge.

Webinar Q&A Highlights

The webinar concluded with a Q&A. Below are the questions and their summarized responses:

Answer: The approach to narrowing down the peer group involves focusing first on operations to find peers operating in the same area, which is crucial for valuation. The second aspect is considering the geographical market, as it significantly influences profitability and market structure. If these criteria are met, further refinement can be done by looking for smaller cap companies if valuing a smaller company and using keyword research to identify unique aspects of the company.

Answer: For valuing a loss-making startup, the Venture Capital (VC) method is usually used. This method is specifically designed for valuing startups, particularly effective in scenarios of loss-making and fast-growing companies. It involves seeking an exit of the investment at a future date at a price consistent with valuation multiples observable in the markets.

Answer: When valuing SMEs in the current market, it’s important to do extensive market research, particularly focusing on the cost of capital. This includes monitoring operational market trends such as the number of M&A transactions in a specific market and economic factors like the risk-free rate and market risk premiums. These factors influence the markets and are crucial for an accurate valuation.

Wrapping Up: Summary of Key Learnings from the SME Valuation Webinar

The webinar on the valuation of small and medium-sized enterprises (SMEs) provided essential insights into valuing small and medium enterprises, differentiating these processes from those used for larger companies. Key topics covered included the importance of SME valuation for transactions, financial reporting, and company succession. The discussion highlighted the need for a tailored approach in SME valuation, addressing unique challenges such as owner involvement and specific financial and legal aspects. A practical case study using Valutico’s software demonstrated the application of these concepts, emphasizing the role of technology in enhancing valuation accuracy and efficiency. Overall, the webinar bridged theoretical knowledge with practical application, offering valuable perspectives for professionals in SME valuation.

To get the complete insights from this webinar, watch the full replay on LinkedIn, YouTube, or Facebook. If you would like a copy of the presentation, please send us an email at [email protected]

TAGS:

More M&A Insights

Stay up to date with M&A news!

Subscribe to our newsletter