By Neal Ransome – PricewaterhouseCoopers

M&A activity proliferates

2006 and the first half of 2007 saw a significant increase in M&A activity in the global pharmaceutical and healthcare sectors, continuing the upward trend exhibited in recent years.

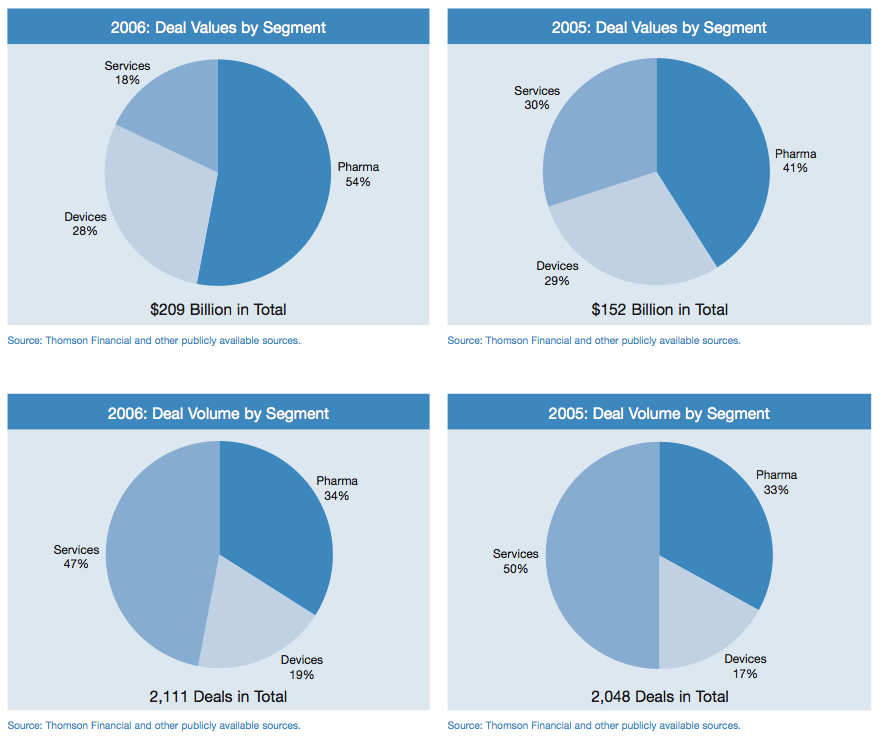

Altogether in 2006 there were 2,111 deals across the pharma/medical devices/healthcare services sectors with a total deal value in excess of $209bn compared with 2,048 deals with a total deal value of $152bn in 2005. In addition to this increased aggregate deal value, 34 deals individually worth more than $1bn were recorded in 2006 compared with only 28 in 2005.

There have been 995 deals in the first half of 2007 worth a total of $140bn, suggesting that 2007 is going to be another busy year in M&A for the sector.

Pharmaceuticals

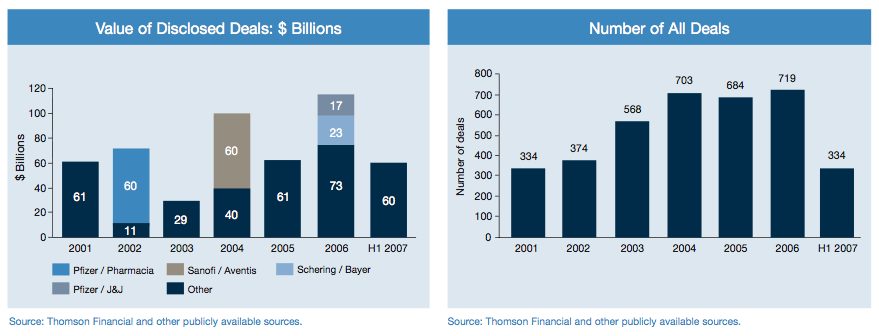

M&A activity in the pharmaceutical sector was worth $113bn in 2006, a significant increase on the $61bn achieved in 2005.

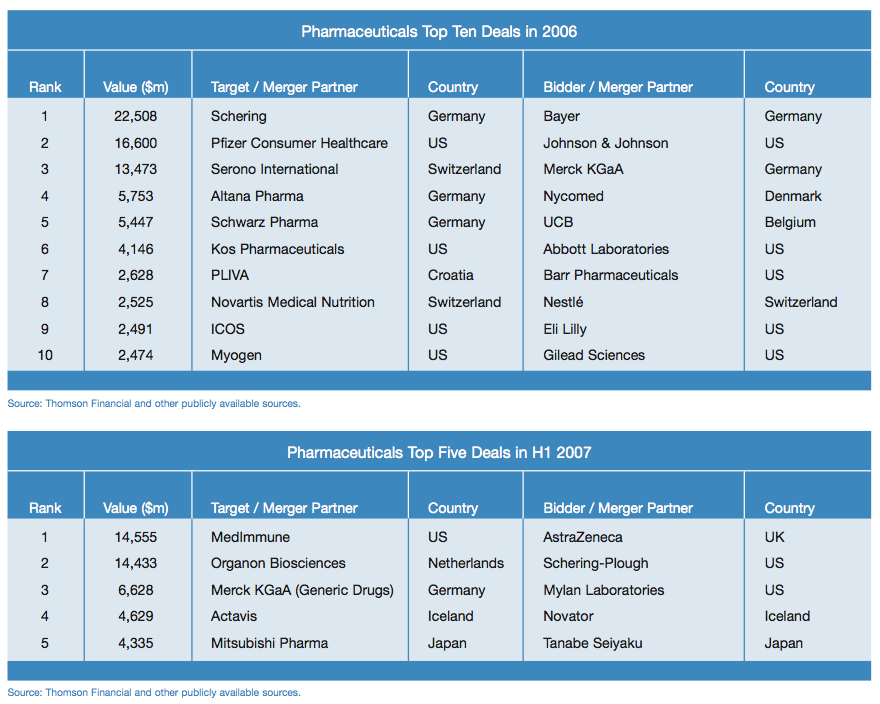

Deal volumes were only slightly up year-on-year with 719 transactions in 2006 compared with 684 in 2005. The surge in deal value was partly caused by three substantial deals, each worth over $10bn. In total, the top ten deals alone accounted for nearly $80bn in value (compared with just under $40bn for the top ten deals in 2005) – largely a result of intensifying competition as pharmaceutical players jostle to boost product pipelines with sizeable acquisitions.

This trend of increasing activity has continued into 2007. In the first half of the year we have already seen 334 transactions valued at $60bn.

A year of strongly contested deals

The largest deal of 2006 was Bayer’s $22.5bn acquisition of Schering.

This has brought together Schering’s reputation for innovative research with Bayer’s development and regulatory capabilities to create Germany’s largest healthcare company.

As a rival bidder to Bayer, and having missed out on Schering, Merck KGaA subsequently purchased Serono for $13.5bn from its controlling family shareholders, strengthening Merck’s product pipeline.

Product pipelines a priority

The strengthening of product pipelines is a key priority for large pharmaceutical companies now facing patent expiry and generic competition.

Pfizer decided to sell its consumer healthcare segment in order to focus on acquiring products and internal R&D in its core pharmaceuticals business. Again, this was a closely contested deal with Johnson & Johnson acquiring the business in a $16.6bn transaction which saw Reckitt Benckiser, following its purchase of Boots Healthcare International last year, and GlaxoSmithKline both reported as competing bidders.

Schwarz Pharma was acquired by the Belgian company UCB, another deal involving the disposal of a large, predominantly family-owned European business. The combined company will build on Schwarz Pharma’s strong late-stage pipeline and look to specialise in a number of high growth therapeutic areas, particularly neurology, oncology and inflammation.

The year also saw Nestlé, widely recognised for its strong food and beverage brands, strengthen its presence in the nutraceuticals sector as it secured Novartis’ medical nutrition business for $2.5bn. As a provider of specialised enteral and oral nutrition products it will be accessing a growing market supported by the demographics of an ageing population.

Competition for generics

Within the generics arena, the purchase of the Croatian company PLIVA was the highest profile transaction in 2006.

This deal involved a three-month bidding war between eventual acquirer Barr Pharmaceuticals and Actavis. It reflects a strong appetite for consolidation within the generics sector where economies of scale are key. The acquisition enabled Barr to increase access to the European markets and in particular Eastern and Central Europe where medicinal drug consumption is growing rapidly. The combination has created the fourth largest global generic pharmaceutical company and will allow Barr to gain a footprint in the emerging biosimilar market, building upon PLIVA’s biologic research programme.

STADA also looked eastwards at higher growth markets and lower cost manufacturing with its $581m acquisition of Serbian Hemofarm.

Other significant generics deals in this consolidating sector included Hospira’s $2.1bn acquisition of injectable oncology drugs specialist Mayne Pharma; Watson Pharmaceutical’s $1.9bn acquisition of Andrx Corp; Dr Reddy’s acquisition of German Betapharm for $571m; and Mylan Lab’s $736m acquisition of Matrix Labs. This latter deal gave Mylan access to lower cost API (active pharmaceutical ingredient) manufacturing in India as well as its European sales and marketing operations.

The generics sector has seen continued activity into 2007, most recently the battle to gain control of Merck KGaA’s generics unit. Mylan Laboratories beat competition from trade buyers and private equity houses to acquire the business for $6.7bn. This highly contested deal has propelled Mylan to number three position in the global generics market behind Teva and Novartis.

Also in the first half of 2007, Actavis was taken private by Novator, an investment firm founded by Actavis’ Chairman. At the time analysts commented that this would allow Actavis to bid more aggressively in M&A transactions having previously missed out on the Pliva and Merck KGaA transactions.

Regional analysis

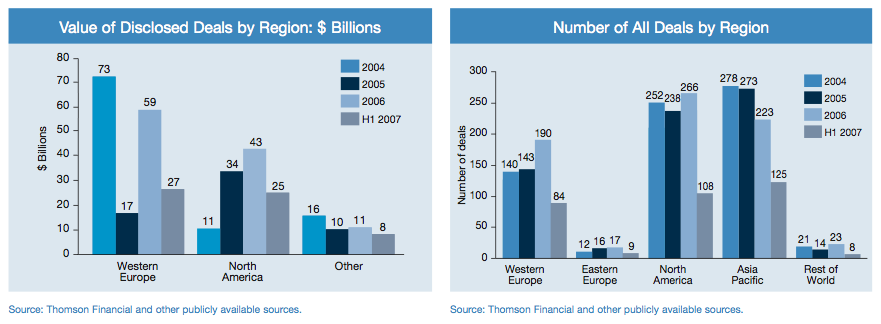

While deal values in North America increased by over 25% compared to 2005 levels, it was mid-market consolidation within the European market which really fuelled deal activity in 2006 and has continued to be high in 2007.

Four of the five largest deals in 2006 involved pan-European consolidation, with three of the targets being based in Germany. In addition to the deals already mentioned, the Danish group Nycomed (private equity backed) was successful in acquiring the German company Altana, a provider of prescription drugs, for $5.8bn.

The pharmaceutical sector is not as benign a market as it was in previous decades. Pharmaceutical companies are faced with diminishing pipelines, products coming off-patent, and increasing pricing pressure from purchasers. Faced with these threats, critical mass becomes increasingly important if companies are to compete on the global stage. More recently, this has put European companies in particular, under growing pressure to consolidate.

Future Outlook

We have anticipated the consolidation of the European mid-market for a number of years, and while we have seen some similar activity in previous years, 2006 was the first year in which there was real momentum behind this trend.

European consolidation is expected to continue into 2008, as will the tendency for larger pharmaceutical companies to focus increasingly on their core competencies, divesting divisions such as OTC and animal health.

Another key trend sweeping through the industry is the need to scale down operations in anticipation of declining sales as a result of products coming off patent.

A more aggressive prediction would be that despite limited evidence to support the theory that mega-mergers improve R&D productivity, the market will see one mega-merger before the close of 2008 (the first since 2004) driven by a company unwilling to entertain the prospect of a declining top line.

Biotechnology

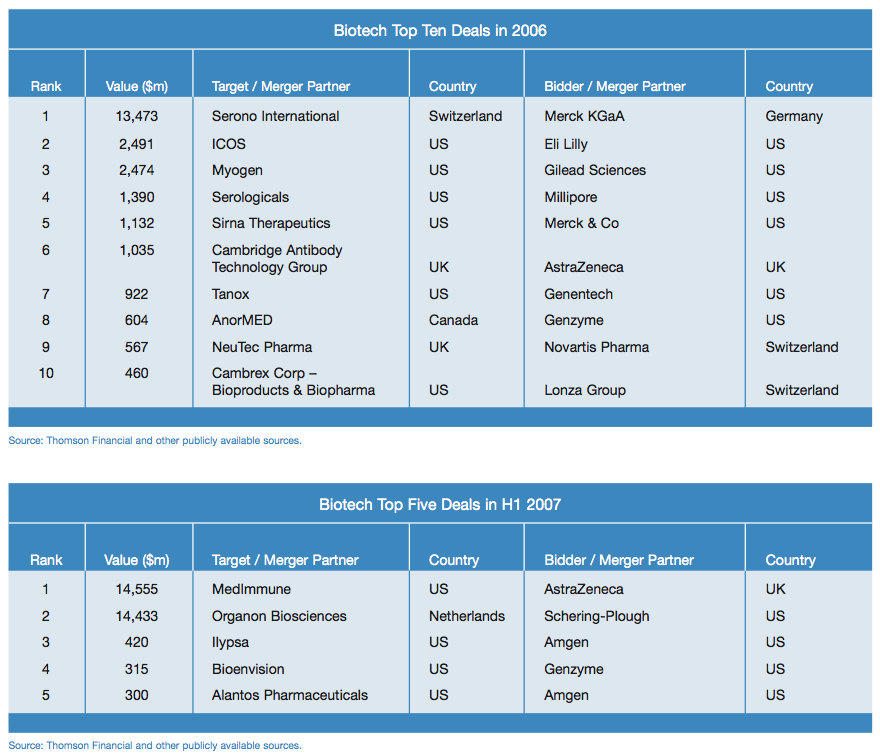

The top ten deals in the biotechnology sector in 2006 had a combined value of $25bn compared with $15bn in 2005.

Three biotechnology deals were among the top ten pharma deals in 2006, reflecting the growing importance of the segment.

The value of the top five deals in the first half of 2007 was $30bn, comfortably exceeding the value of the top ten deals in the prior year, as a result of the acquisitions of MedImmune and Organon Biosciences by AstraZeneca and Schering-Plough respectively. These were also the top two pharma deals coming in at $14.6bn and $14.4bn respectively.

While North American targets comprised the majority of top deals in 2006, it was Switzerland’s Serono that commanded the number one spot at a value of $13.5bn. The purchase of Serono saw Merck KGaA strengthen its position in the biotechnology sector with additional capabilities in developing and manufacturing innovative biologics. The acquisition also served to strengthen its ethical portfolio particularly in the areas of oncology, autoimmunity and inflammatory and reproductive health.

Large pharmaceutical players dominate

Following at a distance were the still sizeable acquisitions of ICOS by Eli Lilly and Myogen by Gilead, standing at just under $2.5bn each.

Myogen will help to expand Gilead’s pulmonary portfolio and follows its purchase of privately-held Corus Pharma for $365m. ICOS, acquired by Eli Lilly to increase its market share in the erectile dysfunction market, was another deal in the trend that is seeing larger pharmaceutical players acting on the high growth potential in the biotechnology sector. Indeed, five of the top ten deals fell into this category of big pharma acquiring smaller biotech.

Merck & Co’s acquisition of Sirna Therapeutics gave it access to Sirna’s core technology with the potential to treat HCV and other retroviral infections including HIV. In a further display of its appetite for biotech opportunities Merck announced in 2007 the $400m acquisition of biotech company GlycoFi in a deal that followed on from its partnership agreement.

Consolidation of former alliances

A strategy adopted by many big pharma companies in recent years has been to enter into alliances with biotech companies as a means of assessing their technology and building a relationship prior to making an outright acquisition.

In 2006 several such partnerships were consolidated. Eli Lilly and ICOS had previously been involved in co-marketing and developing a proprietary treatment, while Genentech’s $922m acquisition of Tanox involved a drug previously subject to collaborative agreements. Such deals allow the acquirer to purchase on the basis of proven relationships and to eliminate royalty payments while accessing full revenue streams.

AstraZeneca was another big pharma involved in cementing a former alliance with the $1bn purchase of UK-based Cambridge Antibody Technology Group. It secured CAT’s proprietary antibody engineering platform to enhance its pipeline of biological therapies. The more recent acquisition by AstraZeneca of MedImmune – at $14.6bn the largest pharmaceutical and biotech transaction to date in 2007 – has significantly accelerated AstraZeneca’s biologics strategy, bringing critical mass and, in combination with CAT, creating a fully integrated biologics and vaccines business.

Growth for niche biotech companies

While large pharma companies have been particularly busy, biotechnology players have also been active in the M&A market.

Millipore’s acquisition of Serologicals will unite two high growth companies and allow for an expanded portfolio with strengths in markets such as drug discovery, antibodies, reagents and stem cell culture. Global biopharmaceutical player Genzyme won a battle with Millennium Pharmaceuticals to purchase AnorMED, successfully securing the late stage stem cell transplantation product Mozobil. Genzyme followed this with the acquisition of Bioenvision during the first half of 2007, gaining Genzyme exclusive rights to the oncology product Clofarabine which it had co-developed with Bioenvision.

Amgen has also been acquisitive, expanding its renal care offering with the purchase of Ilypsa, which develops non-absorbed drugs for renal disorders. This was followed by Amgen’s acquisition of Alantos Pharmaceuticals which develops drugs for the treatment of diabetes and inflammatory diseases, helping Amgen to diversify its portfolio beyond its epo franchise.

Emphasis on molecular activity

The biotechnology sector as a whole has made marked advances in recent years.

The advent of genetic profiling is allowing for strong growth, and with an inherently complex manufacturing process there is high demand for new production capacity. One company seeking to meet the increased demand is Lonza. In 2006 it purchased Cambrex’s biopharma business for $460m, acquired a production plant from Genentech for $150m and announced plans to build a second facility in Singapore.

Medical Devices

Consolidation in the mid-market

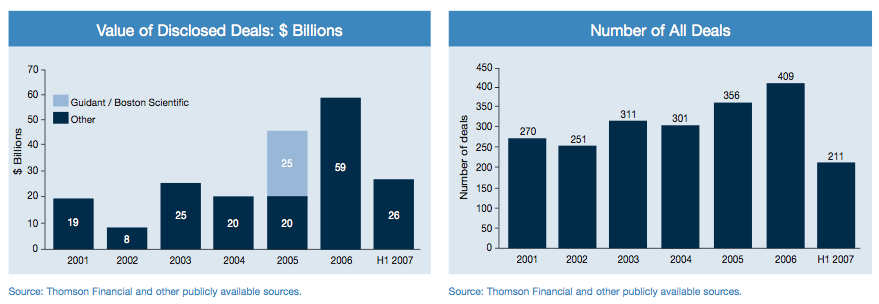

The total deal value in the medical devices sector in 2006 was $59bn, a substantial increase on the 2005 total of $45bn, particularly given that the latter figure included Boston Scientific’s $25bn Guidant acquisition.

The growth reflects an increase in both average deal values and the total number of deals. This stood at 409 in 2006 compared with 356 in 2005.

This trend has continued into 2007, where we have seen 211 deals worth a combined $26bn in the first half of the year.

The sector cannot lay claim to any blockbuster deals in either 2006 or H1 2007. It has instead been characterised by consolidation among mid and small-sized companies and product lines.

Private equity at the forefront

Traditionally steering clear of large pharmaceutical deals, private equity houses were once again at the forefront of the medical devices segment, claiming three of the top ten deals in 2006 and two of the top five in H1 2007.

The largest deal in 2006 was the $10.8bn Biomet acquisition. The acquiring consortium, comprising Blackstone, Goldman Sachs, Kohlberg Kravis Roberts and Texas Pacific, defeated Smith & Nephew in its attempt to acquire its rival and hence strengthen its position in the reconstructive orthopaedics market. In 2007 Smith & Nephew has partly compensated for the frustration of failing to acquire Biomet with its $889m acquisition of the Swiss company Plus Orthopedics.

Phadia, a provider of in-vitro allergy testing systems and autoimmunity testing was acquired by Cinven in a secondary buyout from PPM Capital, while Gambro, which specialises in renal products and services, was taken private by EQT/Investor AB for $5.3bn.

In 2007 Molnlycke Health Care was acquired for $3.7bn by a consortium comprised of Investor AB and Morgan Stanley, and VWR International was acquired by Madison Dearborn Partners from Clayton, Dubilier & Rice private equity investors for $2.2bn.

High demand for diagnostics

The diagnostics sub-sector, in particular, has been subject to increased activity as new technologies improve our ability to detect diseases and screen for genetic susceptibilities.

Siemens made two large acquisitions in the fields of immunodiagnostics and molecular diagnostics. The acquisition of Diagnostic Products for $1.8bn was followed by the $5.3bn acquisition of Bayer’s Diagnostic division.

We see molecular diagnostics as an area of particular interest with trends mirroring those seen in biotech following the advent of gene analysis.

The Siemens deals were part of a targeted strategy to create the healthcare industry’s first integrated diagnostics company by combining the entire imaging diagnostics, laboratory diagnostics and clinical IT value chain.

One of Siemens’ major competitors, General Electric, appears to be pursuing a similar strategy, and in 2007 launched an $8bn bid to acquire two units from Abbott Diagnostics. However, after prolonged negotiations, this deal was called off.

Philips, meanwhile, looked to strengthen its position in diagnostic imaging with the acquisition of Intermagnetics General, a manufacturer of magnetic components used in magnetic resonance imaging and patient monitoring devices. The deal strengthens Philips’ position in the growing MRI market, giving it access to enhanced technologies and allowing it to further integrate its supply chain.

Diagnostics activity continues in 2007

The largest medical device deal of H1 2007 was the $5.8bn acquisition of Cytyc by Hologic.

Both companies provide medical devices and equipment relating to women’s health and diagnostics and their combination will create a global leader in this area. Cytyc itself had made two significant acquisitions in 2007 (Adeza Biomedical and Adiana) prior to being acquired by Hologic.

Another diagnostics deal announced in 2007 was Inverness Medical Innovations’ acquisition of Biosite, which had previously been in merger discussions with Beckman Coulter, and is a leading developer of protein markers.

Vascular activity

Abbott Laboratories’ acquisition of vascular intervention and endovascular assets from Boston Scientific broadens Abbott’s portfolio to enable it to cover a complete line of vascular devices.

This transaction arose following anti-trust issues related to Boston Scientific’s acquisition of Guidant in 2005.

Also in the vascular business, Johnson & Johnson acquired Conor Medsystems for $1.5bn in a bid to boost its drug-coated stent business. Johnson & Johnson lost out in its bid to acquire Guidant in 2005 and the Conor acquisition will provide it with next-generation stent technology to enhance its position in a competitive market.

Fund raising

Public markets

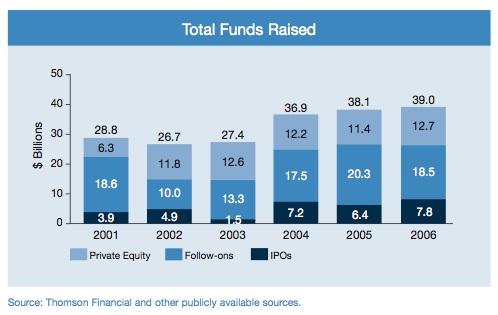

2006 saw total IPO proceeds increase to $8bn from $6bn in 2005. Although a large proportion of these listings were biotech companies, the number of IPOs was well down on 2005, reflecting a strong M&A market.

Brazil, enjoying strong growth forecasts and increasing foreign direct investment, had three sizeable IPOs. The largest of these was Profarma, a pharmaceutical distributor, for proceeds of $349m. This was followed by health and dental providers Medial Saúde and Odontoprev for $340m and $240m respectively.

Our 2004 Insights predicted a possible re-listing for the US-based pharmaceutical manufacturer Warner Chilcot. It had been quoted in the UK but was then taken private by a financial consortium led by Bain Capital. Its 2006 US IPO fulfilled this prediction, raising $1.1bn.

Other significant IPOs in 2006 included Spanish pharmaceutical manufacturer Grifols, UK care home provider Southern Cross Healthcare, the Chinese device manufacturer Mindray Medical International, and Russian anti-cancer drug manufacturer Veropharm.

In secondary offerings, Bayer raised $1.5bn, the proceeds being used to help fund its acquisition of Schering. Similarly, care home services provider Brookdale Senior Living commanded $874m in an offering that facilitated its $1.2bn acquisition of American Retirement Corporation.

Private equity

Private equity interest in healthcare has continued unabated.

The focus has remained on the medical devices and healthcare services sectors where revenues are perceived to be more stable, and R&D risk is reduced, rather than in the pharmaceutical or biotechnology sectors. In total over 850 private equity deals contributed nearly $13bn in straight equity funding.

Private equity, traditionally benign within the pharmaceuticals sector, provided the funding for Nycomed’s acquisition of Altana Pharma during 2006.

While we do not expect a sudden surge in such deals, it is likely that private equity will command an increasing presence in the pharmaceutical sector as the process of developing and selling medicines responds to increasingly commercial demands. We have seen private equity, in recent years, engage in transactions of escalating values across all industries and sectors. On this basis at least one of the 13 companies in the Big Pharma universe appears to be within reach of private equity – a current possibility that may materialise before the end of this decade.

Hospitals continued to be a key area of interest. Deals in 2006 included the buyout of HCA Inc by a consortium led by Bain Capital and KKR, and Apax’s acquisition of European hospital group Capio. Apax also co-invested with Netcare, the South African hospital provider, in its $3.9bn acquisition of the UK hospitals group General Healthcare.

The strong fundamentals exhibited in the healthcare sector continue to attract private equity interest, be it hospitals or care homes, with ageing demographics and increased preventative care presenting a positive background and fuelling deals on both sides of the Atlantic.

Stay up to date with M&A news!

Subscribe to our newsletter