By KPMG

Deal Trends / Executive Summary

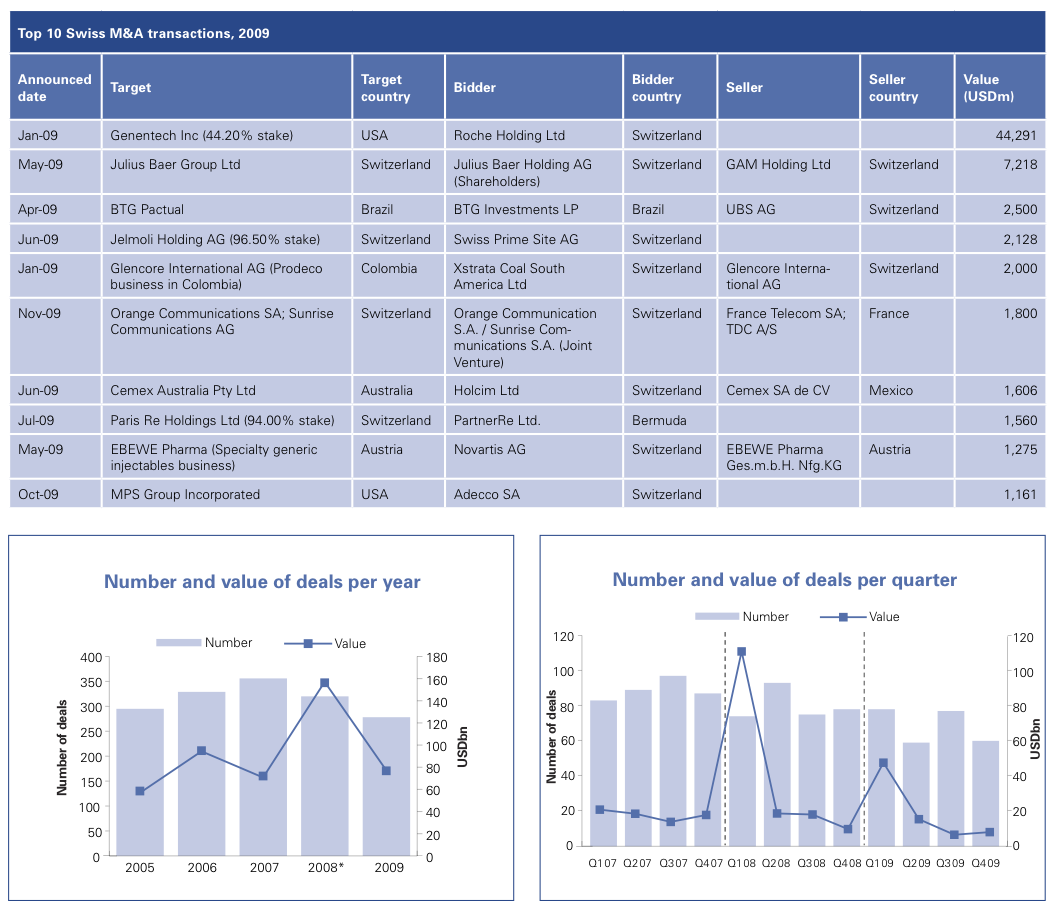

The global financial crisis has had a profound impact on almost every aspect of the global economy. The Swiss M&A market is certainly no exception in this regard with 2009 witnessing a sustained decline in the volume and value of transactions coming to the market. Over the last 12 months, 276 such deals were announced worth a combined USD 78.6 billion. Compared to 2008 this represents a 14% decline in deal volume and an even more pronounced 50% fall in total transaction values, where such values were disclosed.

The continued reluctance of banks to finance M&A deals has meant that cash continues to be king in the Swiss market. Indeed, companies are currently hoarding cash in a bid to strengthen balance sheets and as a result, M&A is not on the agenda for many corporates. Continued uncertainty around the market’s emergence from the effects of the economic downturn has heightened firms’ cautiousness, significantly restricting deal flow with companies still reticent to broker a transaction. Consequently, the majority of deals that have come to the market have either been very strategic in nature or driven by corporate survival and a fundamental need to get the transaction done. Against this gloomy backdrop, it has to be noted that strong corporate players have in fact used the period of economic downturn to re-evaluate their strategy and are, now that the market is recovering, able to take strategic initiatives in a considered and confident manner. Deals are being done, albeit in a very different style than in 2007.

While Swiss firms have perhaps been less exposed to the downturn than others, there is still little visibility on corporate performance with no clear outlook for company results and uncertainty over order books. Nevertheless, the fact that domestic firms are less leveraged than their European counterparts has meant that distress driven M&A deals have been less commonplace. This could develop further in 2010, depending on the economic development, but it is looking as if the Swiss corporates have weathered the worst of the storm. On the buy side, firms are beginning to look at prospective targets, although the conservative nature of many companies has so far minimised the level of announced activity.

Despite the uncertainty regarding the corporate outlook for 2010, it is notable that equity markets have rallied in the last six months. In turn, this has forced up the value of publicly listed firms. Inflated equity prices have meant that, oftentimes, the share price of a company belies the weak underlying fundamentals and uncertain economic outlook.

Consequently, it is arguable that the significant rally in equity markets has been excessive and over the medium term, a firm’s performance and share price will converge with either equity markets experiencing a downward correction (W-shaped recession) or the economic outlook improving. Remarkably, a fall in share prices could actually spur public M&A as valuations become comparatively more attractive to prospective acquirers.

Looking at individual sector activity, the Financial Services and Healthcare and Life Sciences sectors have witnessed the most significant transactions in the Swiss market and this is unlikely to change going forward. A number of domestic and overseas Financial Services companies are looking to do deals within the asset management and private banking spaces which are particularly fragmented and ripe for consolidation. Private banking M&A will also be driven by the impending changes to offshore banking regulations and the clampdown on so-called tax havens. Indeed, the likes of ING and Commerzbank have already moved to dispose of such assets in Switzerland in 2009.

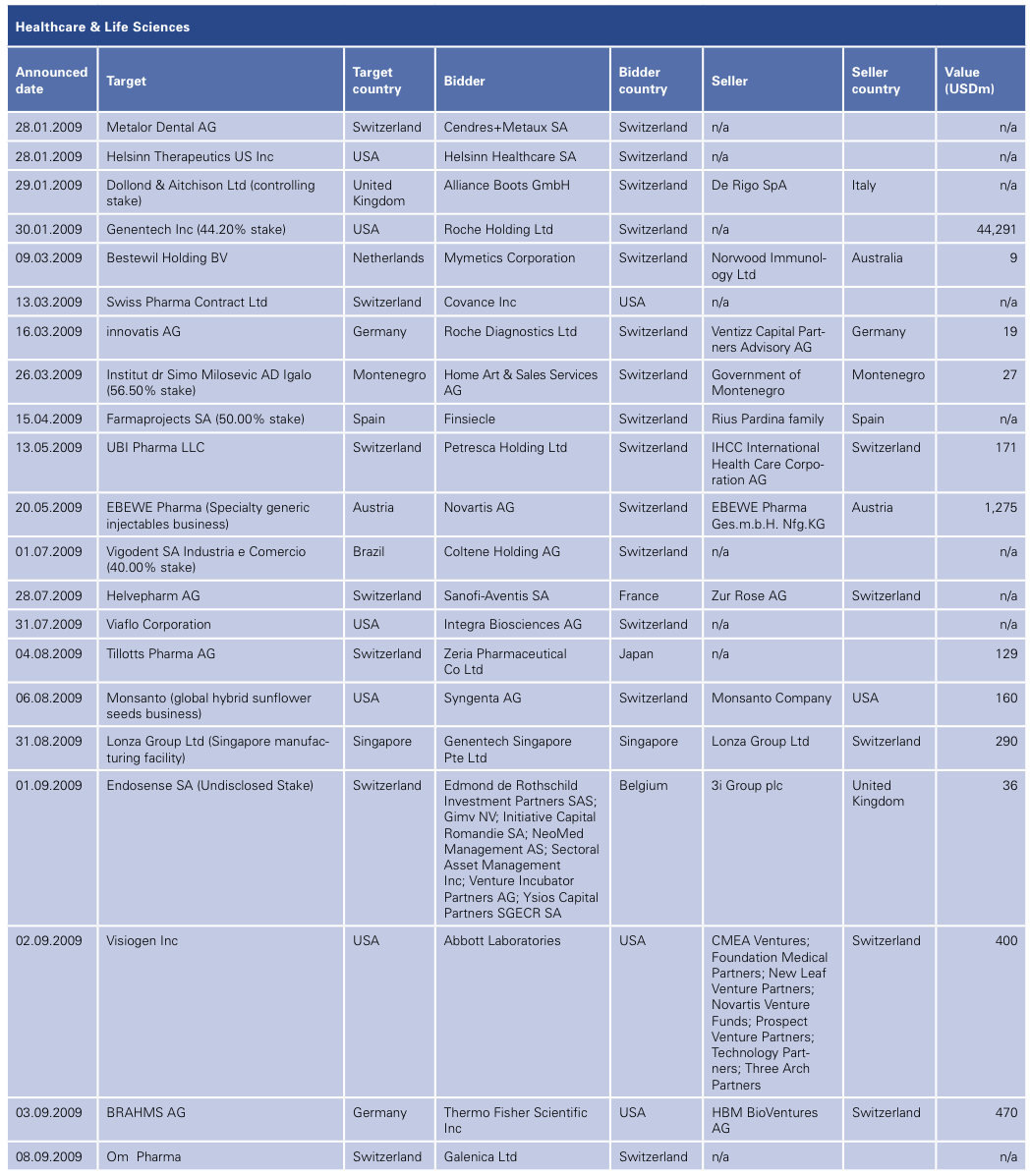

The countercyclical nature of the Healthcare and Life Sciences sector will ensure that deals continue to be brokered. Activity will be driven by sector-specific issues with firms needing to refill the pipeline of new drugs in the face of imminent patent expirations. The lack of available financing is not an insurmountable obstacle due to the cash-rich nature of many firms operating in the sector. This is borne out by the fact that the largest Swiss M&A deal of 2009 saw Roche acquire the remaining 44.2% stake in Genentech for USD 44.3 billion at the height of the financial crisis in the first quarter of the year.

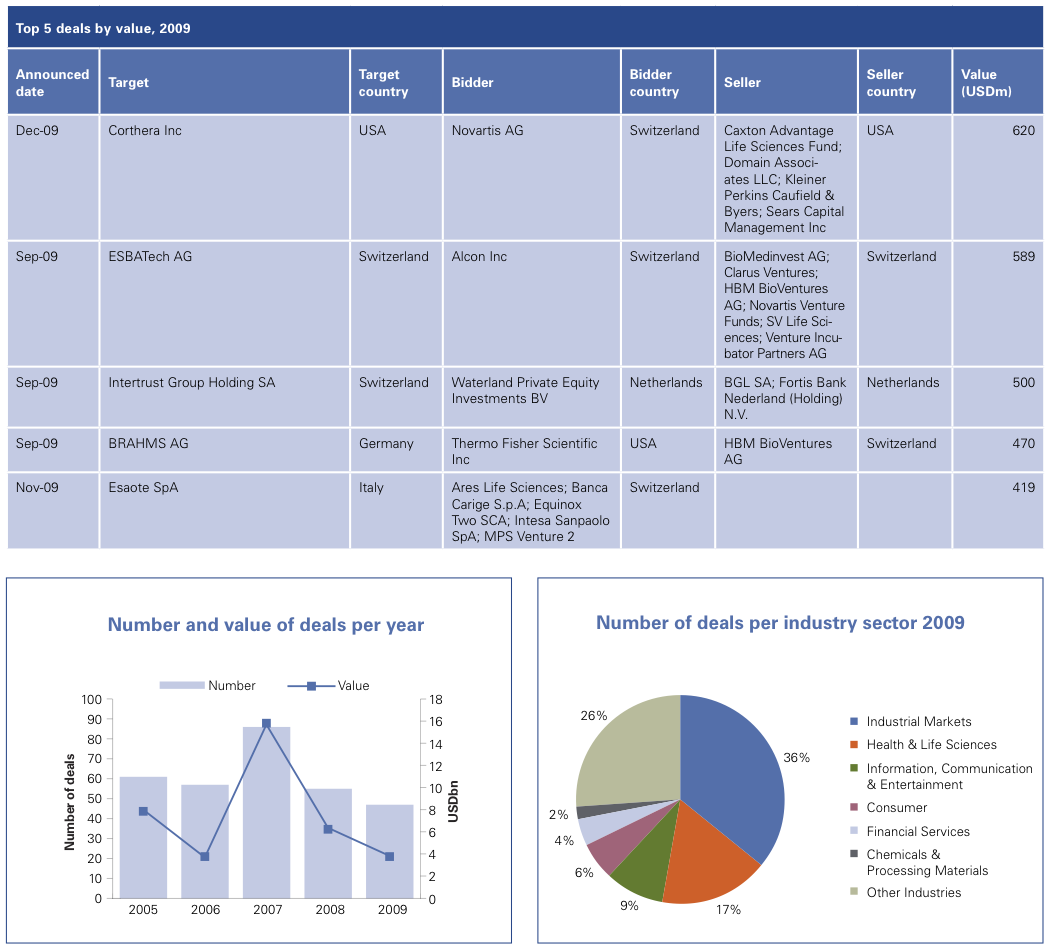

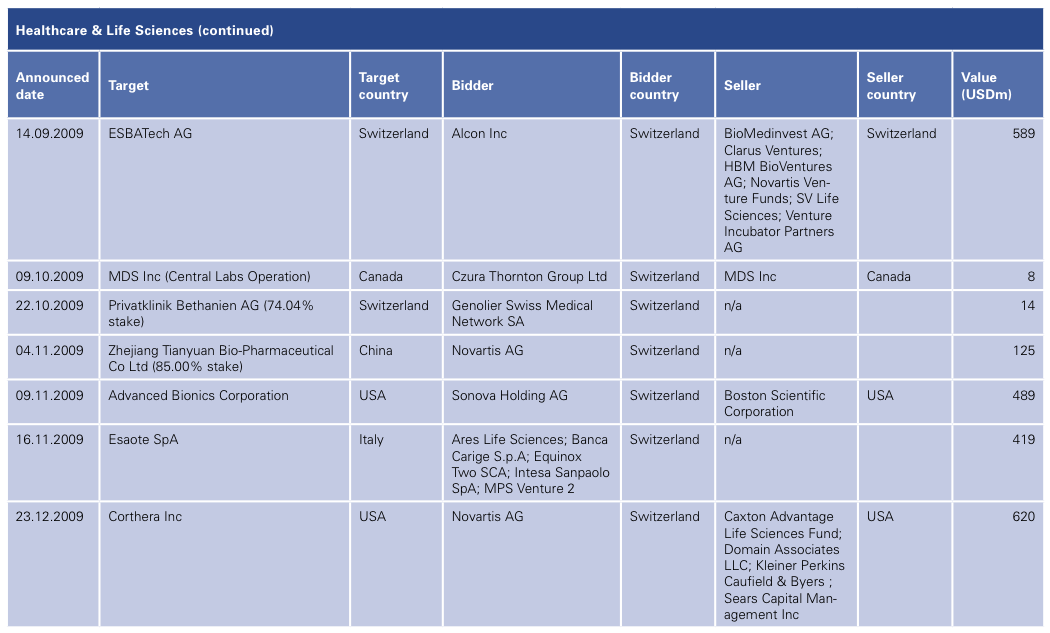

Big Healthcare and Life Sciences players in general are looking to expand and balance their portfolio offerings with Novartis moving further into the Asian market. There are also a number of attractive assets in Europe which could be acquired, including Mepha which has agreed to a take-over by US-based Cephalon Inc., and Germany based Ratiopharm. In terms of likely participants on the buy side, Novartis started the new year (2010) with the announcement of increasing its 25% stake in Alcon to 77% and the prospect of subsequently integrating Alcon, CIBA Vision and other selected ophthalmics into a new Novartis eyecare division. In a related deal, it is interesting to note that Novartis Bioventures, the venture capital arm of Novartis, was part of a consortium of investors that sold ESBATech to Alcon Laboratories in September 2009 for USD 589 million.

The Industrials sector has seen brisk dealmaking with the mid-market space dominating. Not one large-cap transaction was announced last year, a clear sign of the lack of funding available to firms in Switzerland and in the wider economy. The largest such deal was valued at USD 349 million with Schweiter Technologies acquiring Alcan Composites from Rio Tinto. Further consolidation around the textile machinery space is likely and could be driven by Asian bidders with Chinese and Indian firms currently actively eyeing assets.

The financial crisis has also brought about a fundamental shift in the way private equity firms are operating. Unsurprisingly, buyout and exit activity has been hit hard by the difficult debt financing environment, with the majority of the deals in the lower end of the market. Financial investors continue to look at opportunities, but concerns around value preservation at portfolio company level, a lack of attractive targets and competition from cash-rich corporates, have served to depress activity. Furthermore, vendors that are in a position to delay a sale are generally doing so in the hope that valuations will begin to trend upwards in the coming months.

While the Swiss M&A market has begun to show signs of recovery, there is still a significant level of uncertainty. Financial investors continue to be hamstrung by scarce funding and many corporates are unwilling to broker deals, preferring to take a cautious approach and rebuild their balance sheets. Dealmaking conditions can only further improve and M&A will continue to return to corporate agendas in 2010. However, the recovery will be slow and unsteady and it will take time for market confidence to completely return. (Tobias Valk, Partner, Head Transaction Services and Patrik Kerler, Partner, Head Mergers & Acquisitions)

Healthcare & Life Sciences

The global financial crisis has of course had an impact on the companies operating in the Healthcare and Life Sciences space. However, the robust nature of the large pharmaceutical players in this sector has meant that M&A activity has held up relatively well. Such cash-rich firms have been able to execute deals throughout the downturn due to their strong balance sheets, which also means the banks are willing to lend them money in this otherwise austere debt financing environment. In contrast, the biotechnology segment of this sector has struggled from a shortage of credit, making some of them targets for the larger pharmaceutical players.

Indeed, 2009 was a surprisingly strong year for dealmaking in the Swiss Healthcare & Life Sciences space. Compared to 2008 numbers, deal volume increased by over 25% while 2009 aggregate values amounted to USD 49.3 billion, an increase of nearly four times the value of announced deals witnessed over the previous 12 month period. However this pronounced uptick in valuations must be solely attributable to a single blockbuster transaction which saw Roche acquire the remaining 44.2% stake in United States based biotechnology leader Genentech at the height of the financial crisis in January 2009. This was one of three global megamergers seen during the 2009, the others being Pfizer and Wyeth, and Merck & Co. and Schering Plough.

Wider deal flow in the sector continues to be driven in response to overcoming four key challenges that players face. The first major challenge that pharmaceutical companies have to deal with is the increasing number of patents that are expiring which in turn cut off valuable revenue streams. Secondly, the growth of generic drug sales is placing pressure on manufacturers of patent protected active pharmaceutical ingredients (API). Shrinking new drug pipelines provides the third challenge to the industry, a development which means pharmaceutical companies can no longer solely rely on organic growth. Finally, regulations are becoming increasingly stricter and continue to lengthen the time to market for new drugs. All of these challenges can be met through M&A and this is a strategy that many players have pursued and will continue to do so in 2010.

Looking forward into 2010, the big question is whether the megamergers of 2009 will put pressure on other large pharmaceutical and biotechnology companies to react with megamergers of their own. Many large industry players have distanced themselves from making such a move, pointing towards smaller strategic acquisitions. We would see three obvious trends in this regard.

Firstly, an increased number of generic manufacturers will likely be acquired by big pharma players. There is already a precedent here in Switzerland with the second quarter of 2009 seeing Norvatis acquire the specialty generic injectables business of Austrian firm EBEWE Pharma for a cash consideration of USD 1.3 billion. Elsewhere, Sanofi-Aventis also moved to acquire Helvepharm, the Swiss generic drugs distributor, for an undisclosed sum in July 2009. A press release at the time of the deal stated that Helvepharm has a portfolio of more than 59 drugs and a market share of 5.4% in the Swiss generics market and the acquisition will specifically strengthen and expand Sanofi-Aventis’s product line.

Secondly, an increasing number of biotech companies will also attract the attention of the larger pharmaceutical players. A case in point in this regard is Alcon Laboratories’ third quarter, USD 589 million buy of ESBATech, the Swiss biotech company that develops single-chain antibody fragment therapeutics, from its shareholders. In its statement announcing the acquisition, Alcon Laboratories commented that the deal would establish a sustainable platform for ongoing biologics development.

Finally, we see a continuing trend of large pharmaceutical companies making bolt- on acquisitions to expand their business in emerging markets. Novartis’s recent acquisition of a majority stake in the Chinese human vaccines business, Zhejiang Tianyuan, is a good example of this.

On the flip side, inbound interest from Asia and particularly India’s Ranbaxy Laboratories and China’s Wuxi Pharmatech is increasing as such firms look to expand into the European market. However, it remains to be seen whether such acquisitive interest will translate into announced deal flow in the Swiss market over the coming months. (Joshua Martin, Director, Transaction Services)

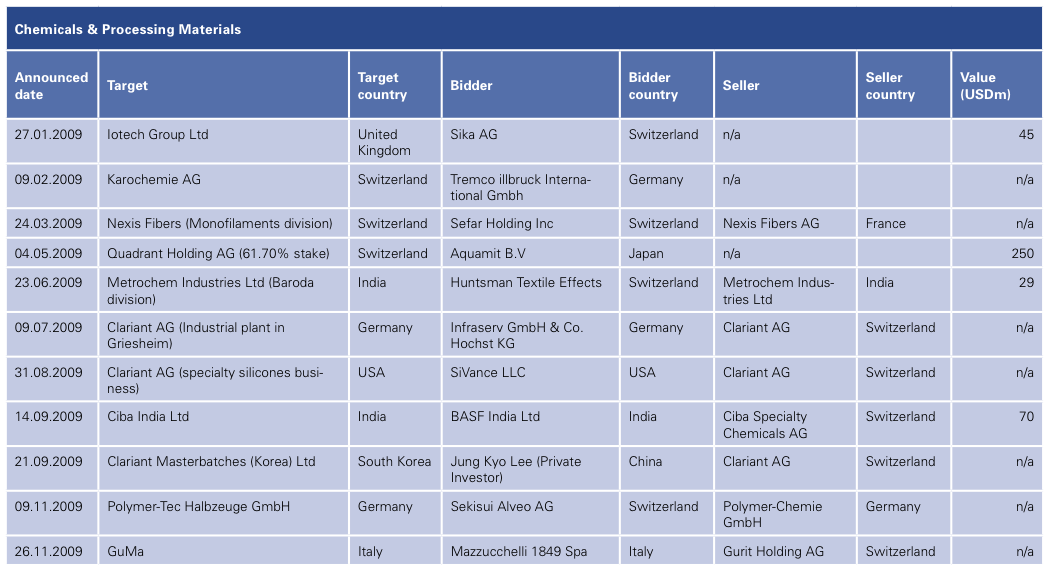

Chemicals & Processing Materials

While there are a number of large Chemicals & Processing Materials businesses in Switzerland and the number of deals has remained consistent, the overall value of deals is spectacularly lower. Indeed, just 11 such transactions worth USD 394 million came to the market in 2009, compared to 11 deals worth USD 5.3 billion over the previous 12 months period. The top deal saw Aquamit, the Netherlands based investment holding company created by the management and Mitsubishi Plastics, move to acquire a 61.7% stake in Quadrant Holding, the provider of semi-finished and finished polymer material.

Looking ahead to 2010, there is an expectation that deal flow could pick up. A number of chemical firms made it through the worst of the downturn in 2009 by implementing cost cutting measures. However, many of these businesses operate in markets which are still being affected by the economic downturn and this could lead to further distressed asset sales in the coming months. On the buy side, some of the better performing chemicals companies could step up and play a consolidator role.

M&A activity in Switzerland and, indeed, Europe could also be strengthened by an influx of Middle Eastern and Far Eastern buyers. One example is the rising number of well-established Japanese and Chinese players interested in buying niche-chemicals providers in Switzerland. Many of them are cash rich and have therefore not been impacted by the difficulties in obtaining financing from banks.

Notably, the Swiss chemicals space also faces a number of significant challenges. Similar to other industries, differing valuations on the buy and sell side are hindering deal flow. To overcome this, companies could look to undertake buy and build strategies in order to increase the overall value of the business.

A further challenge to M&A activity in the Chemicals & Processing Materials sector is the sheer complexity of businesses operating in the space. Chemicals businesses are generally highly integrated, which makes carving out individual operations extremely difficult.

A further feature of Swiss M&A activity in the sector has been the sharp decline of private equity involvement. While private equity deal flow has taken a beating the world over in the aftermath of the financial crisis, the chemicals space has always been challenging for financial investors. The above mentioned high levels of integration within a business often means that a conglomerate approach is more appropriate. Furthermore, the complex nature of businesses necessitates a high level of sector know how which private equity players are not always able to bring to the table. Such obstacles will remain over the course of 2010 with financial investor activity set to remain subdued. (Pablo Ljaskowsky, Partner, Transaction Services)

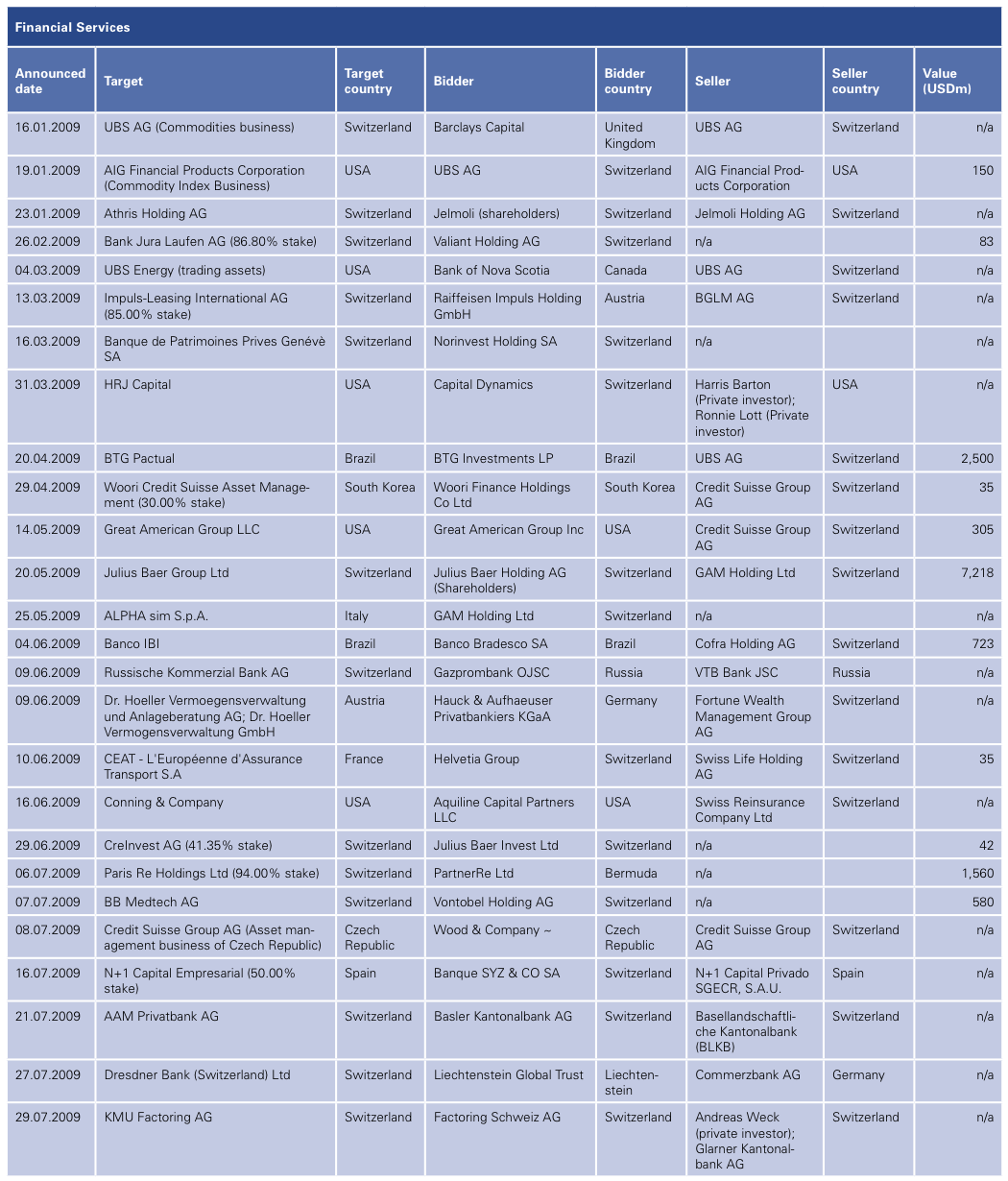

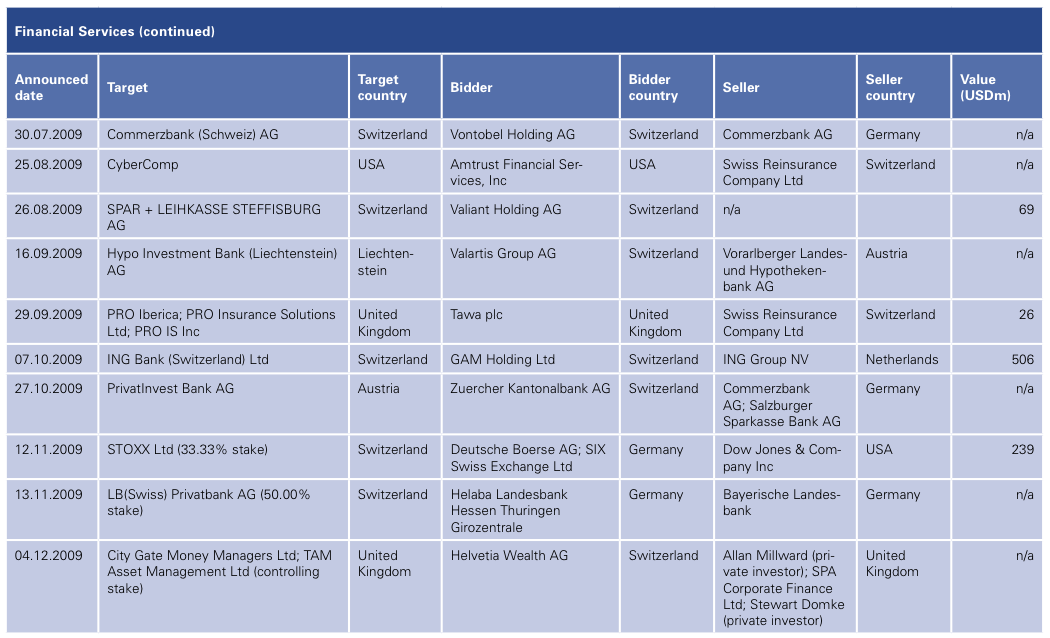

Financial Services

In comparison to other Western European markets, the Swiss Financial Services industry proved to be relatively resilient to the effects of the global financial crisis. That said, the impact of the downturn on the Swiss market and its leading financial companies has, nevertheless, been profound.

When looking at financial industry’s biggest players, UBS stands out as the most prominent victim of the crisis, being one of the country’s largest banks. In the autumn of 2008, UBS received state bailout funds of USD 5.9 billion after writing down a large portfolio of toxic assets, which the Swiss government sold profitably in 2009. UBS was the sole Swiss institution to receive state aid, but other large Swiss financial institutions have also felt the after effects to varying degrees.

Indeed, M&A activity in the Financial Services industry in 2009 was in part driven by non-core divestments as firms moved to shore up their capital positions. The largest such disposal saw UBS sell Brazilian investment bank Banco UBS Pactual to BTG Investments, the Brazilian investment firm founded by Andre Esteves, for USD 2.5 billion in April. Overall, Financial Services deal activity totalled 35 transactions, compared to 41 in 2008, although aggregate valuations rose robustly by nearly one third to USD 14 billion.

The boost in aggregate deal value is largely owed to the USD 7.2 billion demerger of Julius Baer Holdings into two separate, listed entities. The company spun off its private banking business into a new company, Julius Baer Group Ltd, in a transaction that ranked as the largest Financial Services deal of 2009. Welcomed by shareholders, the demerger effectively shelters Julius Baer’s private banking activities from its asset management operations.

Looking forward, private banking remains the area set to witness the greatest amount of M&A activities, spurred by impending changes to the offshore banking model. Switzerland, the world’s largest offshore banking centre, has come under mounting pressure from the likes of the OECD, United States, Germany and Italy for greater disclosure and transparency in the private banking segment.

The pressure on the offshore banking model will lead to further consolidation, with Commerzbank, Dresdner Bank and ING having already divested their respective Swiss private banking subsidiaries. Interestingly, these troubled banks also received state aid in the wake of the financial crisis, raising the question as to whether institutions, now partly controlled by the very governments that are demanding greater transparency from the Swiss private banking segment, should have interests in this market.

With 16% of the Swiss private banking segment owned by foreign companies, further divestments are likely to come to the market. While there is some interest in private banking assets, it remains a relatively small universe of potential buyers which includes some large and mid-sized Swiss private banks, as well as foreign players and financial investors. In addition to this, the Belgian financial group KBC has also announced its restructuring plans, which includes the proposed sale of its KBL European Private Bankers division, which has some operations in Switzerland.

Despite buy side interest in private banking assets, there is still significant uncertainty and risk around the future of the offshore banking sector and any potential acquirer need to have an intricate understanding of the private banks they intend to acquire. More broadly, M&A activity may be driven by some portfolio clean up with the larger players continuing to dispose of non-core operations, as well as the sale of smaller players, which are lacking the critical size in the new world of private banking. Bolt-on opportunities will be relatively abundant with some of the larger players. (Christian Hintermann, Partner, Transaction Services Financial Services)

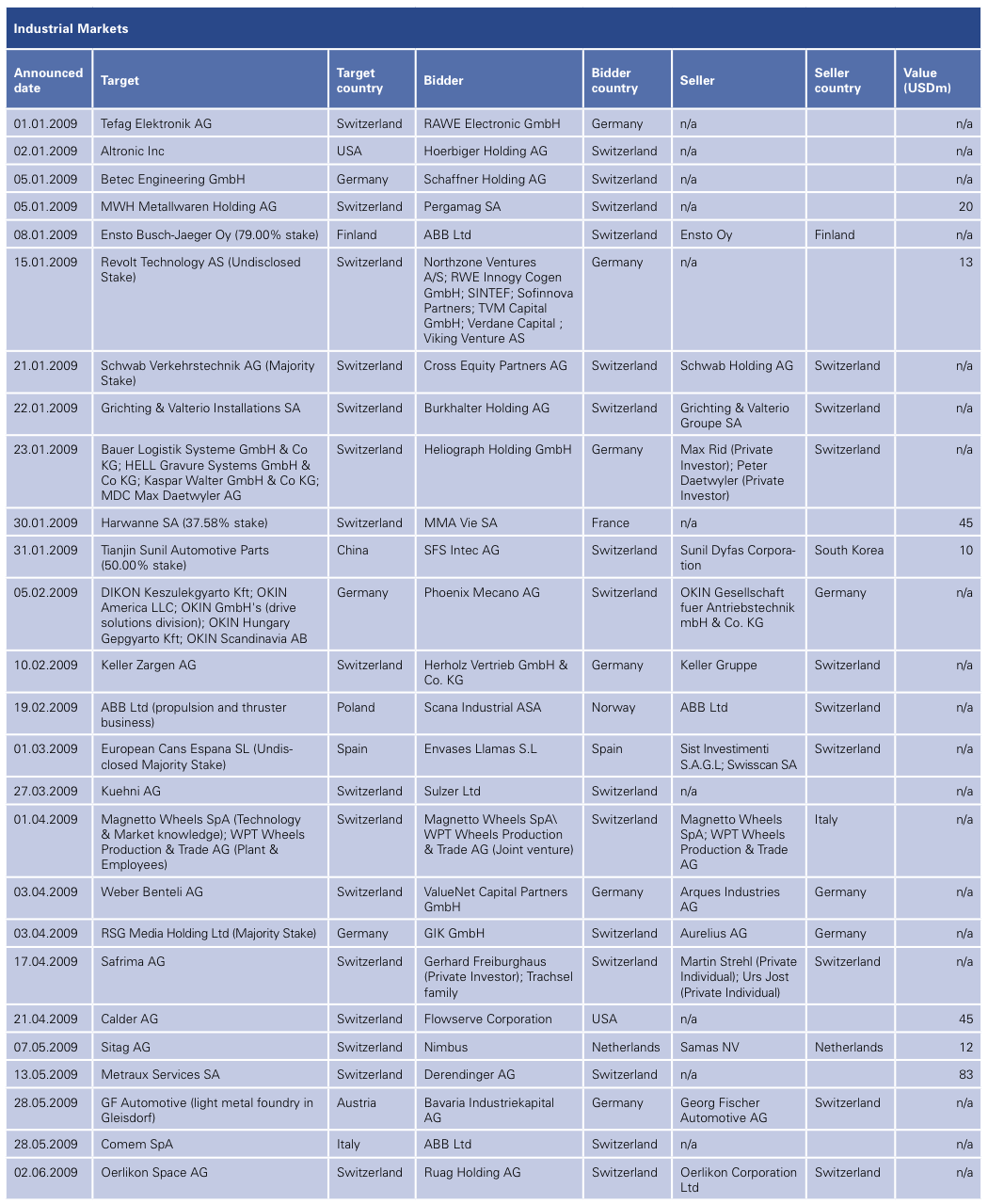

Industrial Markets

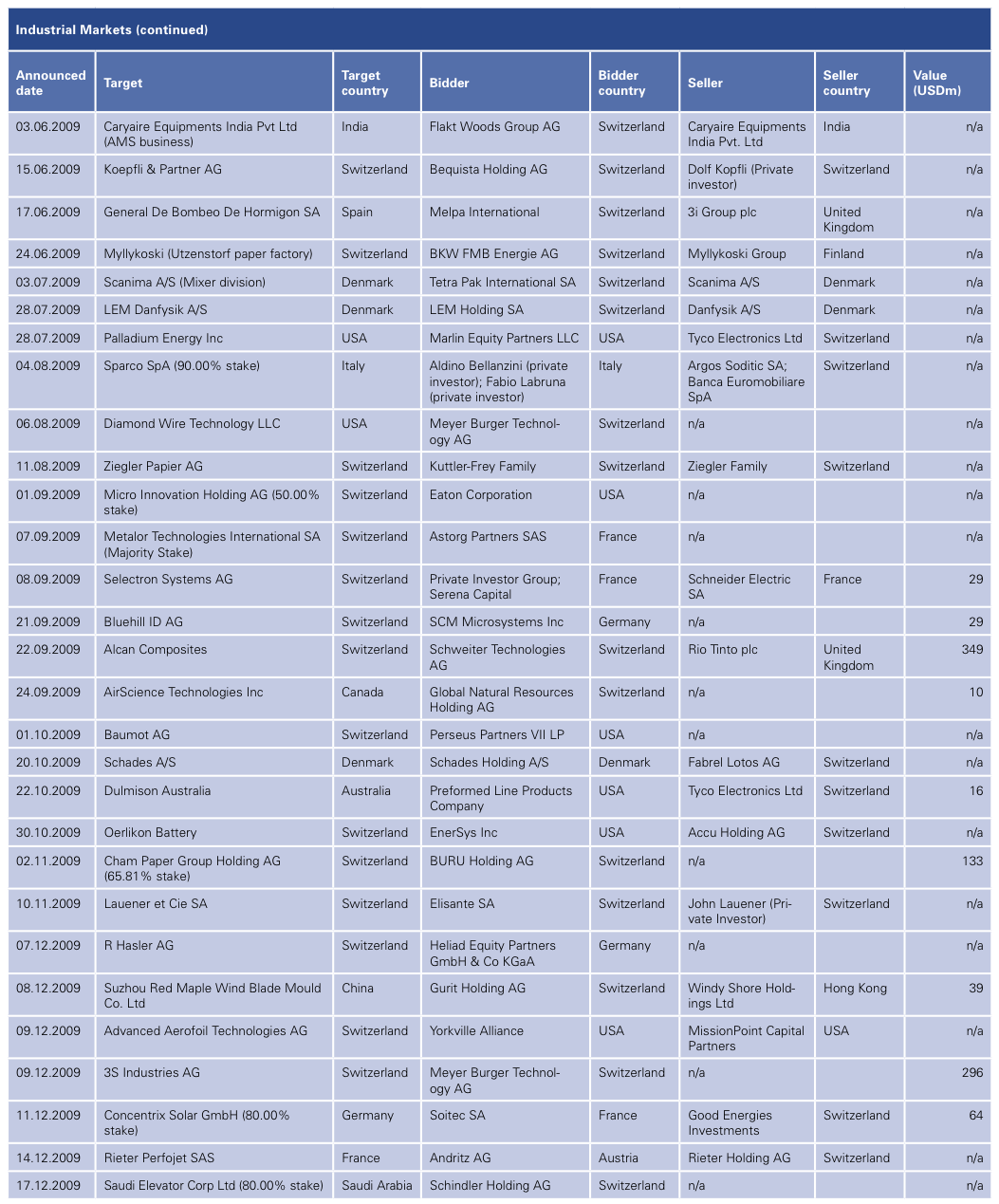

M&A activity in the Industrial Markets niche remained subdued over the course of 2009 with announced transactions collectively valued at USD 1.2 billion. Even compared to 2008 activity, this represents a marked decline in both volume and value terms with price dislocation remaining the principal impediment to dealmaking. Acquirers continue to be sceptical of the potential target companies’ business plans.

Looking at activity in 2009, the top deal was the Schweiter Technologies’ acquisition of Alcan Composites from Rio Tinto for a consideration of USD 349 million. Notably, this transaction is not necessarily representative of wider M&A activity in the sector as it was driven by specific strategic issues. Indeed, in addition to the sale of Ismeca Automation to Komax in 2005, Schweiter had moved to dispose of Satisloh, the manufacturer of optical machinery and lenses, to French firm Essilor International for USD 526 million in June 2008.

Schweiter thus had ample cash on its balance sheet to add Alcan Composites operations proving to be an attractive asset complementing existing divisions and seemingly satisfying key criteria in terms of global market leadership, autonomy and growth opportunities. On the sell side, the deal was driven by Rio Tinto’s strategy of divesting downstream assets.

Notwithstanding the abovementioned deal, the majority of M&A activity in the sector has been driven by the effects of the global economic downturn. In this regard, Oerlikon is a case in point with the specialised equipment manufacturer moving to refocus on core operations, leading to the sale of Oerlikon Space to Ruag Holding in June 2009. Oerlikon, the Switzerland based manufacturer of textile machinery, transmission systems and surface technology acquired Saurer at the top of the M&A cycle in 2006 and has since faced significant problems with sales and orders markedly down since the acute onset of the financial crisis.

The wider textiles industry has also suffered of late, exacerbated by the fact that it is a cyclical industry, which, at the bottom of the cycle, is also facing the worst trading environment in years. This has hastened a flurry of corporate restructurings and forced sales with interest on the buy side among others coming from Europe and China. However, this interest has not necessarily translated into revived deal activity, although there is an opportunity for cash-rich corporates to acquire at the bottom of the market and then benefit on the upward swing of the recovery.

Elsewhere, given the state of the automotive segment, it is somewhat unsurprising that Swiss suppliers to the industry are facing intense pressures with some firms seeing corrections of 40 – 60% in their order intake. Going forward, these problems could prove to be insurmountable and may drive consolidation.

Private equity houses have been relatively inactive in the Industrial Markets space of late, a circumstance that has to be attributed to price dislocation and the availability and cost of debt financing. Indeed, the largest private equity-related deal of 2009 was worth just USD 29 million and saw Serena Capital and a group of private investors back the management buyout of Selectron Systems, the manufacturer of rail automation solutions, from French company Schneider Electric.

Looking ahead to 2010, M&A volumes in the sector are expected to increase, although deal valuations will remain depressed, primarily due to the austere financing environment. Industrial Markets firms are now beginning to think more strategically with M&A slowly returning to the corporate agenda. This increased emphasis on growth could drive consolidation, although disagreements over price will continue to be a large obstacle to dealmaking. However, firms are now looking at viable opportunities and the renewed interest in M&A suggests that buy and sell side parties will begin to converge over valuations. One company to look out for is ABB, which is cash rich and reportedly, “open to bolt-on acquisitions”, according to the Handelszeitung of 6 January 2010. (Sean Peyer, Partner, Transaction Services, and Andreas Poellen, Senior Manager, Mergers & Acquisitions)

Consumer Markets

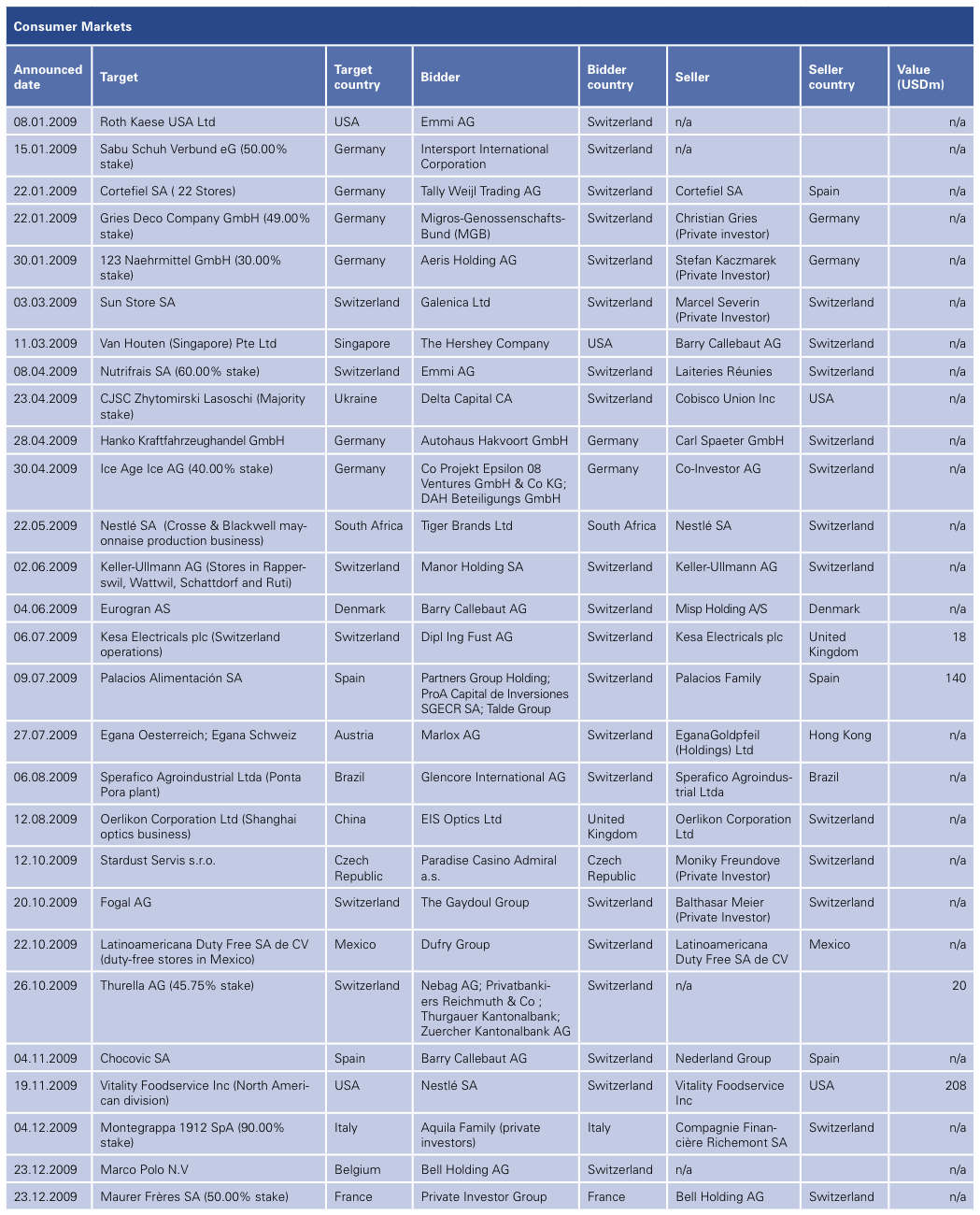

In the first weeks of 2010 the European Consumer sector has decided to free itself from the gloom of the financial crisis with a big bang in the form of Kraft Foods’ imminent acquisition of Cadbury, the UK based manufacturer of beverages and confectionary products, and Nestlé’s announced intention to acquire the Kraft Frozen Pizza business. Kraft’s consolidation play is undoubtedly an encouraging sign for M&A in the Consumer space and could lead to other ‘long rumoured’ deals coming to the market. Indeed, Nestlé has a very strong balance sheet with almost USD 11 billion in operating cash flow and it will likely look to broker significant acquisitions in the coming months. The sheer scale of the Kraft/Cadbury tie up is likely to provide an impetus to M&A activity across all key markets and geographies.

Looking at announced activity over the past 12 months, the Swiss Consumer sector has undoubtedly encountered significant obstacles to dealmaking. M&A activity continued to decline in both volume and value terms with just 28 transactions brokered. The second largest such deal involving a Switzerland based firm was valued at USD 140 million and saw a consortium of investors including listed asset management firm Partners Group Holding back the management buyout of Palacios Alimentación, the Spanish chilled foods company, from the Palacios Family. Elsewhere, the top deal involving a trade acquirer was valued at just USD 18 million with retailer Dipl Ing Fust/Jelmoli moving to acquire the Swiss operations of Kesa Electricals, the listed UK based electrical retailing group.

Going forward into 2010 and beyond, it is likely that the landscape of the Consumer sector will continue to change. Given the continued challenges around financing M&A, an increasing number of paper deals are expected to come to the market, either in pure form or involving a large paper element, the latter can be seen in Kraft’s approach to Cadbury. However, buyers with sufficient cash might prefer to do cash deals instead of using their potentially undervalued shares. In keeping with other sectors, many of the larger players in the Consumer space have used the economic downturn to re-evaluate their strategy. As the markets continue to show signs of recovery, such firms are well placed to act on acquisition opportunities in a well prepared and considered manner. Nevertheless, Swiss players in the Consumer space remain comparatively conservative when it comes to undertaking M&A transactions.

Aside from Nestlé, luxury goods conglomerate Richemont is one such Swiss Consumer firm that is likely to be acquisitive in 2010. It is reported that Richemont’s chief executive Norbert Platt has stated that the company would consider doing deals although corporate valuations and antitrust issues are set to provide significant challenges. Indeed, such obstacles are impacting upon other large players in the luxury segment and will likely hinder dealmaking. In terms of potential acquisition targets in 2010, chocolatier Lindt & Sprüngli is a well established player that would give a prospective acquirer strong access to the top end of the international chocolate market. (Patrik Kerler, Partner, Mergers & Acquisitions)

Information, Communication & Entertainment

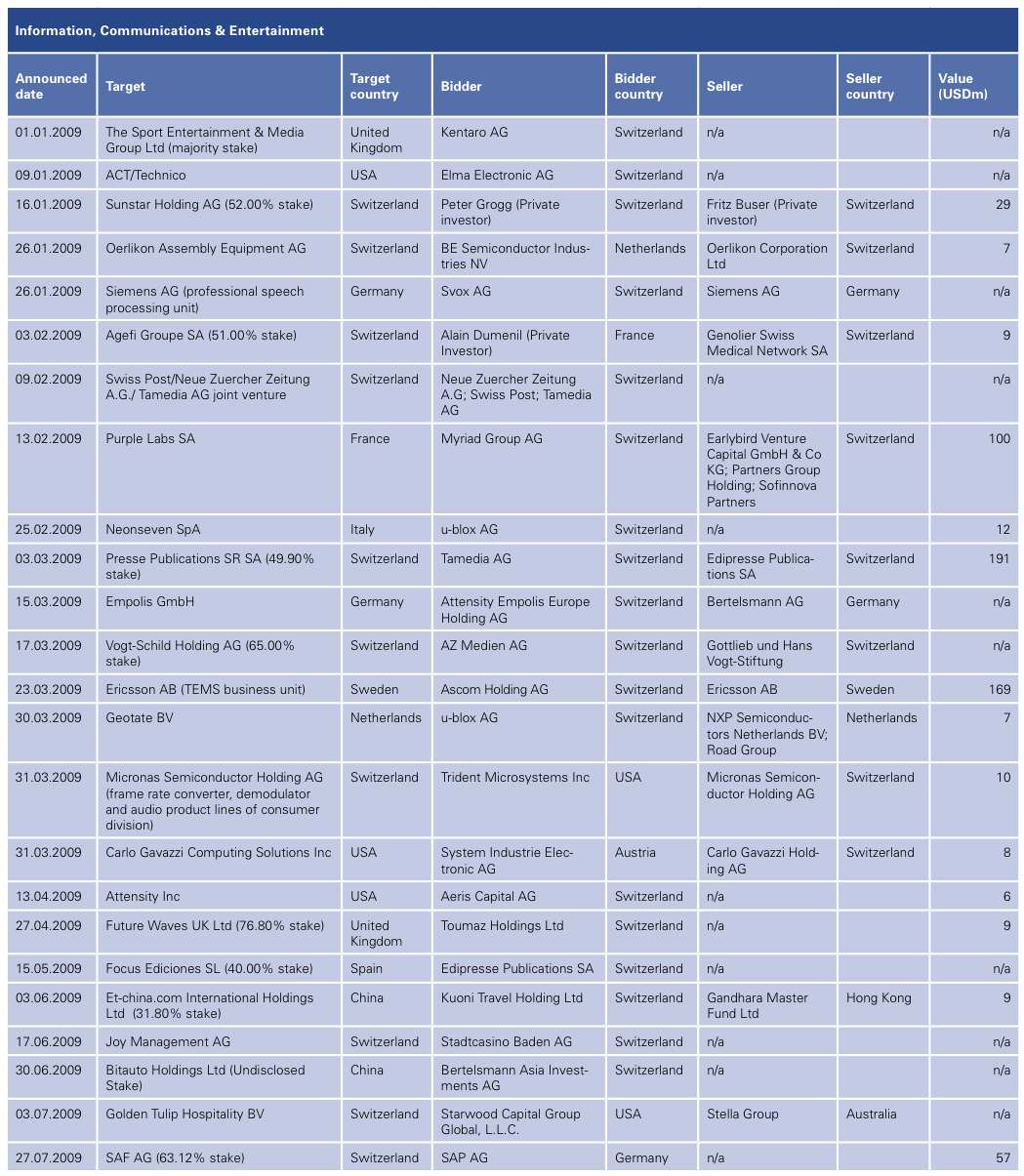

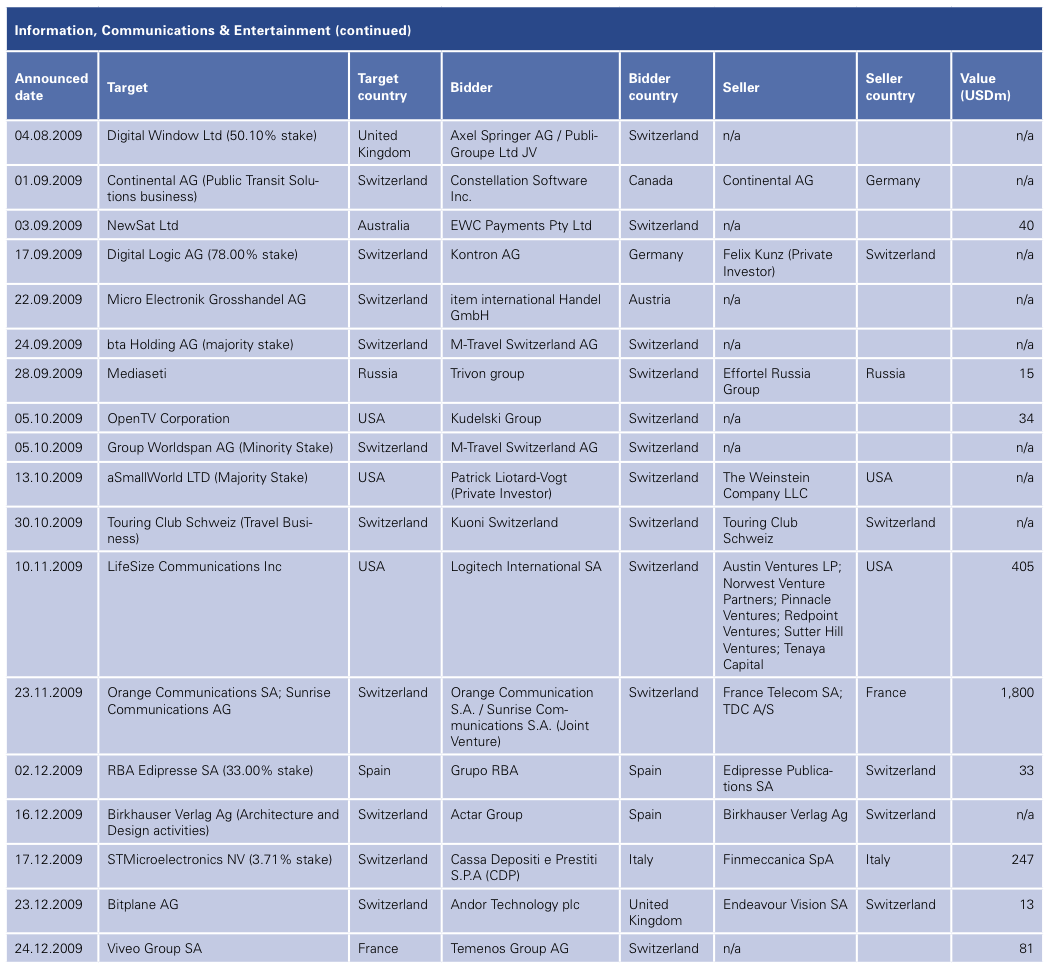

In 2009, Switzerland’s Information, Communications & Entertainment (ICE) M&A market witnessed a slowdown in transaction activity with deal sizes moving firmly into the lower end value range. Comparatively, ICE deal volume fell by around 5% while aggregate valuations rose by nearly 15% in 2009, against a 14% volume and a 50% value decline in the overall Swiss M&A market.

Looking at activity from 2009, several distinctive deal trends within different ICE market segments have emerged. In the media niche, for instance, deal activity has been driven by ongoing consolidation in the highly competitive Swiss media market and the tough stance taken by some media houses. A prime example is the announced tie up of Tamedia and Edipresse, which will see the two firms completely merged by 2013, becoming one of the country’s biggest media groups with enhanced competitive advantages and operational synergies.

In the Communications segment, the tough financing environment has not proved to be a significant problem for the larger telecoms players, as they have focused on smaller bolt-on acquisitions to improve product offer or distribution capability (aside from the Orange – Sunrise merger mentioned below). Vendors in the Swiss ICE sector have, for the most part, not been forced to sell due to financing pressures. This has led to longer sales processes and an ability to wait for improved market conditions.

The most notable transaction in the niche was announced in the fourth quarter with TDC, the Danish telecoms firm, and France Telecom revealing plans to merge their Swiss subsidiaries, Sunrise and Orange Switzerland respectively. Under the terms of the agreement, France Telecom will pay around USD 2.5 billion for 75% of the combined company, while TDC will retain 25%. The merger of Orange Switzerland and Sunrise, already the second largest operator, will create a more viable competitor to Swisscom, the state majority-owned market leader.

Outside of this blockbuster deal, M&A in the Communications space has been augmented by non-core disposals and niche transactions undertaken by the larger players. In this respect, it is noteworthy that Swisscom divested its facility management business, Swisscom Immobilien, for an undisclosed consideration to trade buyer Johnson Controls before brokering two bolt-on acquisitions in June through its IT services subsidiary. These included the acquisition of Resource Group, an SAP focussed IT company, and a 60% stake in Sourcag, the service provider to financial institutions, both for undisclosed valuations. Both assets are in line with Swisscom’s aim of expanding its services portfolio.

Elsewhere, M&A among the technology based ICE firms has been harder hit by the fallout from the financial crisis. Indeed, a slowdown in demand, the tight financing environment and disagreement over valuations have hindered deal flow in the niche. And while some transactions were brokered in 2009, these were driven by a combination of highly strategic reasons and compelling valuations. The former factor led to the acquisition of Ericsson’s TEMS business unit, a developer of mobile network optimisation products, by Ascom Holdings, the Swiss telecoms equipment maker, for USD 169 million. The TEMS business will be merged with Ascom’s Mobile Test Solutions early in 2010, making the group a global leader in the mobile testing and benchmarking space.

Across all ICE market segments, strategic players dominated the M&A landscape with private equity houses remaining largely inactive. Indeed, the most notable deal involving the asset class was in fact an exit to a Swiss trade buyer. In the deal, Logitech International, the listed Swiss manufacturer of computer peripherals, agreed to acquire LifeSize Communications, the US based video communications firm, from a consortium of six US private equity investors for USD 405 million. The acquisition will allow Logitech to benefit from enhanced video communications expertise, LifeSize’s extensive R&D as well as operational and supply-chain synergies.

The semiconductor segment which has been active in recent years saw very little activity, as many Swiss firms are reorganising their activities – such as Micronas and Oerlikon – while u-Blox strengthened its product portfolio with the acquisition of Italian firm Neonseven. In the software segment, the most notable transaction was the merger of Esmertec and Purple Labs (now Myriad Group) to create a stronger mobile application platform provider.

Looking forward to 2010, further consolidation in the ICE markets remains likely, particularly in the Media niche and among mid-sized IT firms. Elsewhere, there may be revived interest in early stage finance opportunities from venture capital and private equity investors. Smaller firms in the sector will continue to be unable to access bank debt on accessible terms and could look to secure financing for higher growth opportunities from financial investors. Meanwhile, some of the main players and large conglomerates in the ICE markets may also look to reshuffle their portfolio and non-core asset disposals will also likely boost deal flow in 2010. (James Carter, Director, Transaction Services)

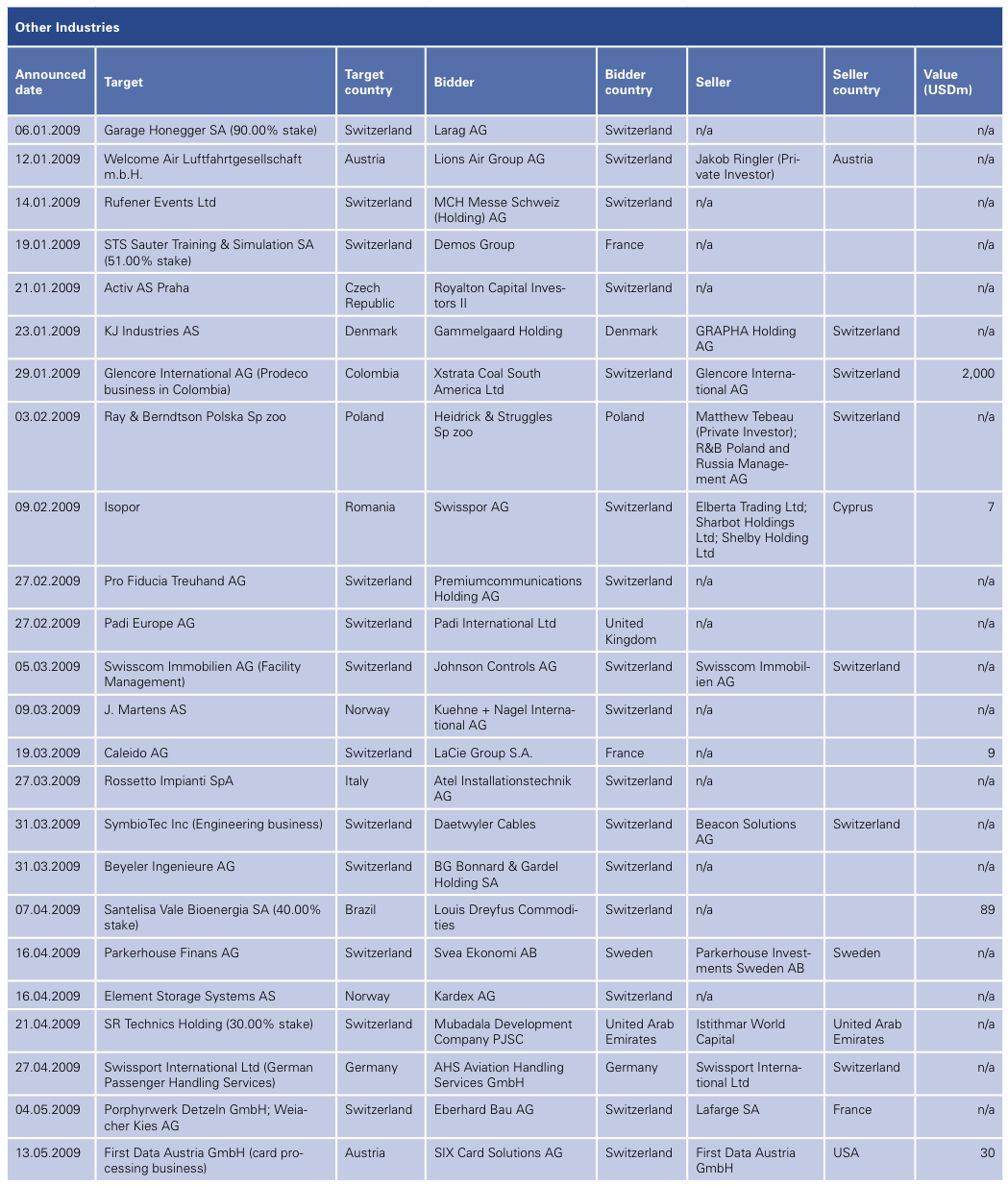

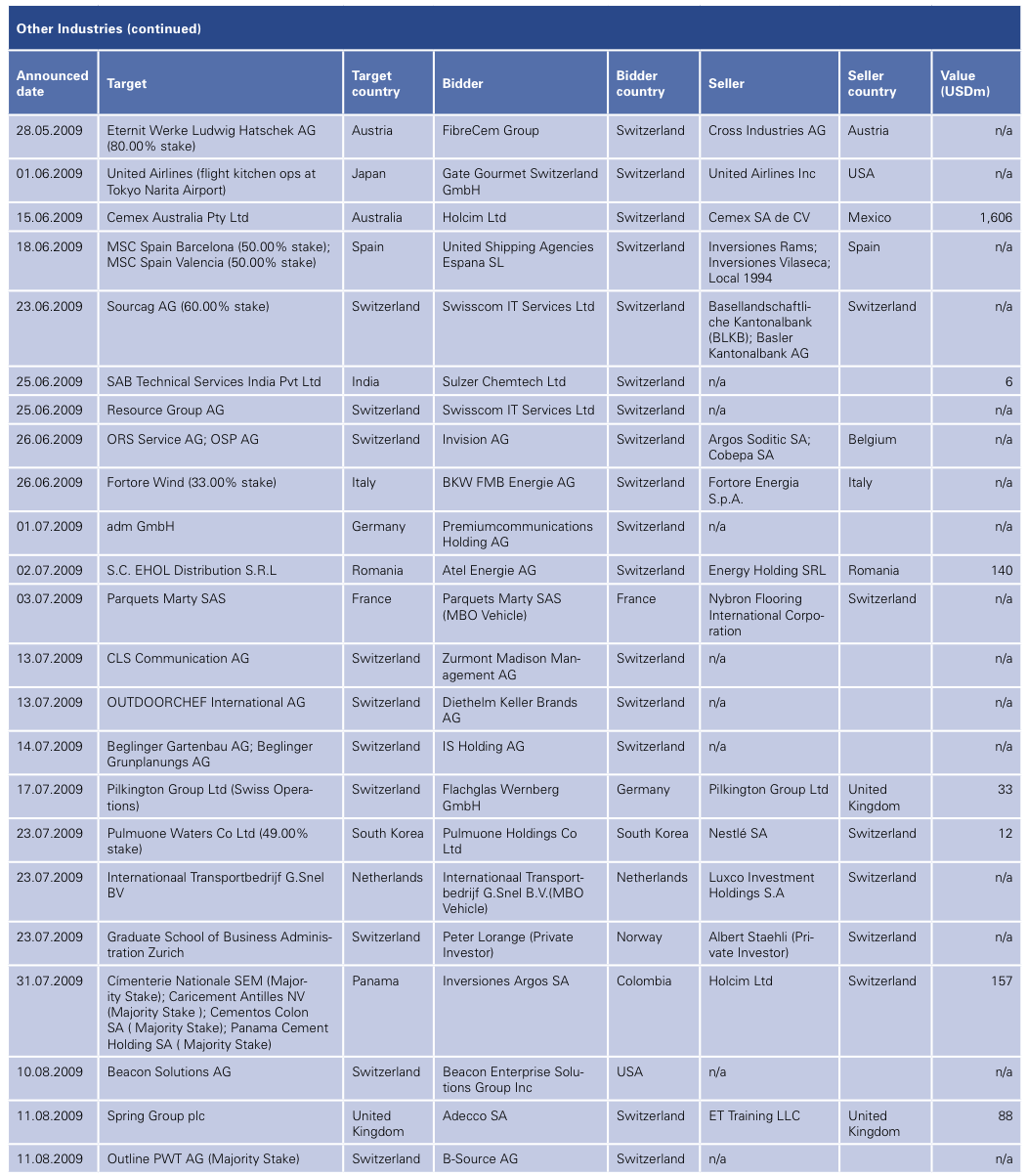

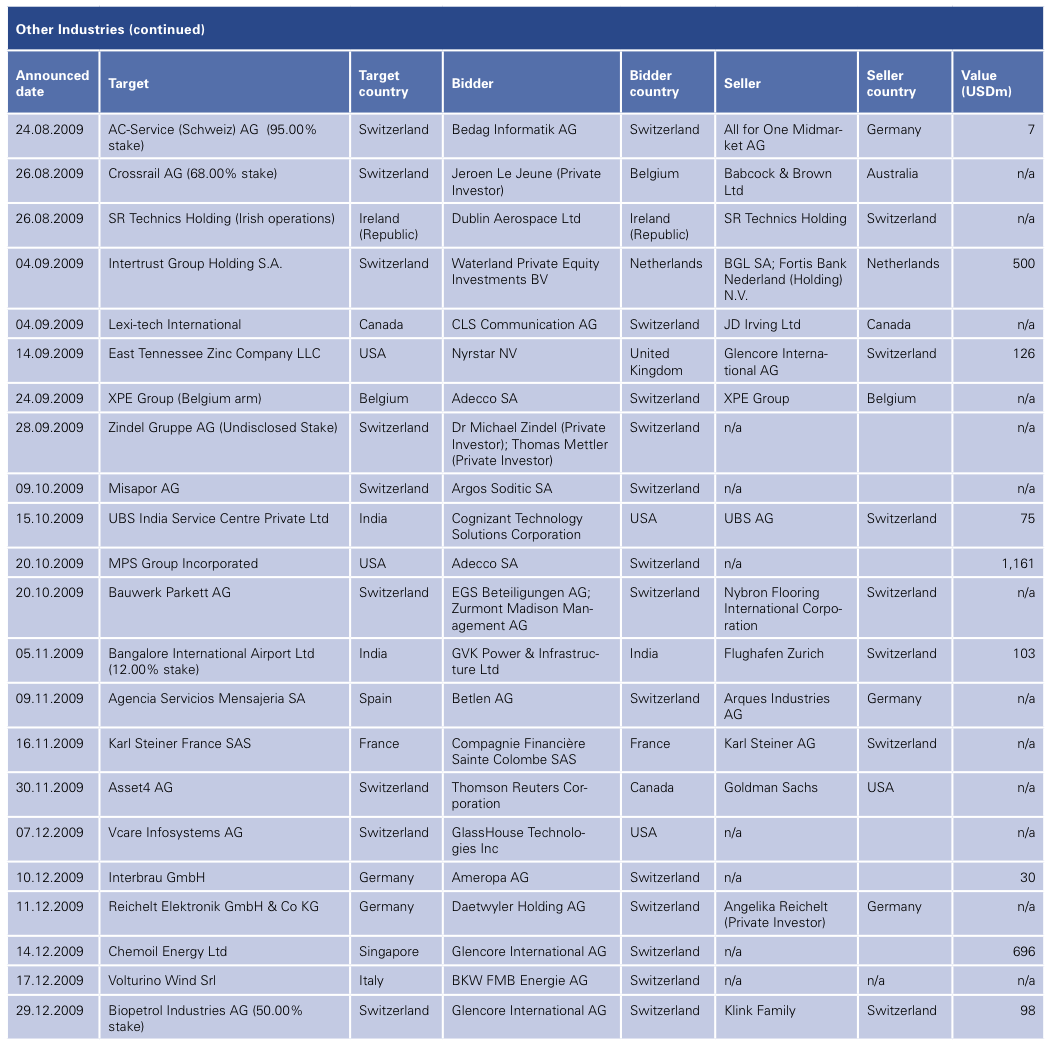

Other Industries

Among the other industries, the most interesting is arguably the Swiss energy segment. This segment is set for increased levels of M&A activity in 2010 as buy side interest continues to pick up. However, while the energy segment has seen robust deal flow in recent years, activity in 2009 was somewhat subdued with just three transactions announced, worth a collective USD 229 million.

The largest such deal was a mid-market play and saw energy services provider Atel (Aare-Tessin Ltd for Electricity), a company of Alpiq Holding Ltd, acquire SC EHOL Distribution, the Romania based energy supplier, for USD 140 million. Interestingly, there was Swiss involvement on the sell side of the deal with the vendor being Energy Holding, a Romanian subsidiary company of Société Bancaire Privée. In stark contrast, the mining niche witnessed the top deal of the year with Xstrata Coal South America, the Switzerland based investment holding company and a subsidiary of Xstrata, agreeing to acquire the Prodeco business of Glencore International for a cash consideration of USD 2 billion. It will be interesting to see if Glencore or First Reserve, its new investor, reacquires these coal assets from Xstrala.

Over the coming months, it is likely that Swiss energy companies will predominately look towards renewable energy targets in Western Europe, mainly in the shape of offshore assets in the North Sea and Baltic Sea. The segment is also of key interest to Asian players, particularly Chinese and Indian firms, although this should not impact upon Swiss players’ ability to execute deals. Indeed, energy is only ‘transportable’ for certain distances and with Swiss firms almost entirely focussed on renewable energy, expansion plans will not come into conflict with those of Chinese or Indian companies. Such Asian players continue to be primarily interested in traditional energy forms such as coal, an area which is largely eschewed by Switzerland based companies.

A further driver of energy segment M&A is a possible push to reduce the amount of nuclear-derived energy. Switzerland could move to reduce the percentage of nuclear-derived energy from the current level of 40%. If the plans go ahead, this will increase pressure on its alternative energy suppliers and such companies could look to expand their capacity via strategic M&A activity.

A key challenge that many smaller, local operators face is the fact that the Swiss energy market is not yet fully liberalised. However, after seeing the effects of a fully liberalised market elsewhere, many people are uncertain and reluctant for Switzerland to go down this route. If liberalisation does indeed occur, there could be significant M&A opportunities with smaller players being ripe for acquisition by larger groups. Nevertheless, maintaining and increasing the level of competition in the market is key to ensuring that the larger plays are kept in check and consumer interests are preserved.

Outside of the energy segment, it is noteworthy that the construction and mining niches have also witnessed significant M&A transactions. While many of the larger mining deals – including the abovementioned Xstrata buy – often involve a Swiss element, this is largely attributable to the fact that many of the larger players are headquartered in Switzerland. Such transactions in fact often have no tangible impact on Switzerland.

The construction space saw, with Holcim acquiring the Australian operations of Cemex, the second largest transaction in Other Industries worth USD 1.6 billion.

Adecco, the Swiss based global market leader in Human Resource solutions continued its growth strategy with the USD 1.2 billion acquisition of US based MPS Group Inc. (Rolf Langenegger, Director, Valuation Services)

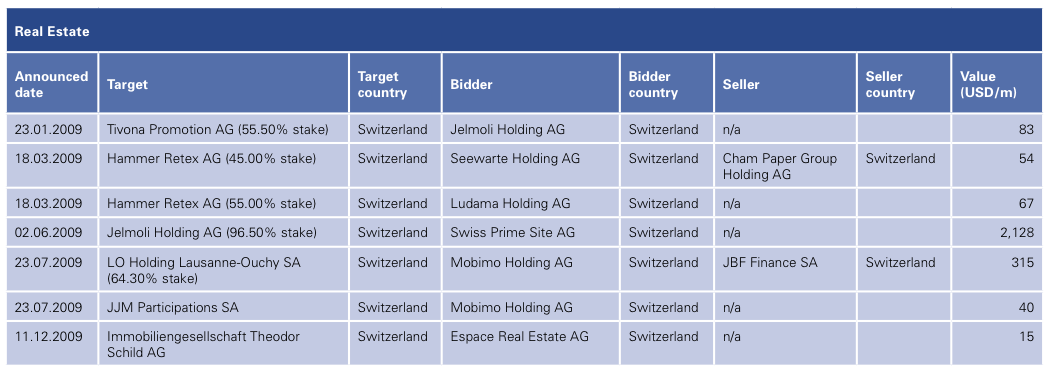

Real Estate

Compared to other markets in Europe and beyond, the Swiss Real Estate segment has fared relatively well throughout the global economic downturn. The lessons learnt when the domestic real estate bubble burst in the 1990s were harsh and lenders have since become increasingly conservative with regard to the provision of leverage in the market. Tax regulations have also served to prevent the quick flips of property, deterring many foreign investors from entering the market. As a result, real estate valuations have generally been stable with institutional investors also helping to ensure the long term value orientation of the segment.

PSP Swiss Property and Swiss Prime Site (SPS) continue to dominate the domestic market with the latter being involved in the largest real estate M&A transaction of 2009 when it acquired a 96.5% stake in rival Jelmoli Holding for USD 2.1 billion. The acquisition marked the end of a tumultuous period for Jelmoli, which started when Israeli firm Delek Global Real Estate moved to acquire a portfolio of 88 properties from the company at the height of the buyout boom in 2007. However, Delek attempted to reduce the offer, before ultimately walking away from the transaction amid a deteriorating debt financing environment.

Delek’s failed takeover was then followed by Jelmoli moving to spin off its investment operations into a new publicly traded company called Athris Holding. The demerger was partly engineered by Jelmoli shareholder Georg von Opel whose company Hansa Aktiengesellschaft took majority control of Athris via its subsidiary Pelham Investments. Von Opel and Pelham Investments then sold a 30% stake in Jelmoli Holding to SPS as part of the abovementioned USD 2.1 billion acquisition.

In terms of the wider real estate M&A market in Switzerland, the Jelmoli deal is something of a one off situation with all other announced activity residing in the mid-market and below. Dealmaking over the course of 2009 has been brisk, surpassing activity witnessed in recent years with a total of seven large and numerous mid-size transactions coming to the market.

The second largest M&A deal of 2009 was also a purely domestic play and saw Mobimo Holding launch a tender offer to acquire a 64.3% stake in developer LO Holding Lausanne-Ouchy. The lack of foreign investment in the Swiss Real Estate segment is reinforced by the fact that each of the top five deals of 2009 involved Swiss based firms on both the buy and sell side.

Continued robust deal flow is anticipated over the course of 2010 with the mid-market continuing to witness the bulk of activity. The lack of leverage in the wider M&A market is not as significant an obstacle with deals in the segment generally exhibiting low debt-to-equity ratios. On the buy side, activity will likely be driven by the larger players in the niche as well as institutional investors such as insurance companies and pension funds. Institutional investors already hold a substantial share of the domestic real estate market and could look to broker further deals with investment decisions continuing to be based on future cash- flows and sustainable yield expectations rather than upon speculative value trends.

Significant investment from private equity funds is not expected as the lower yields in the Swiss market are only attractive for funds that are interested in long-term and stable income. While prices are high due to the size of the market, they are relatively stable and this will continue to be the case going forward. There have been examples, such as Orascom, backing the construction of new ski resorts with such players exhibiting a high risk/high reward profile. Nevertheless, overall buyout activity will more than likely be subdued with established segment players dominating real estate M&A activity in the coming months. (Ulrich Prien, Partner, Real Estate)

Private Equity

The impact of the financial crisis on the overall M&A market has been significant. However, as an asset class, private equity has arguably suffered more than most in recent times. Of course this has also been felt in Switzerland which saw a marked decline in both buyout and exit activity over the last 12 months.

A total of 47 private equity-related deals came to the market in Switzerland in 2009, worth a collective USD 3.8 billion. While this level of buyout and exit activity is by no means insignificant, it is notably down on previous years. Indeed, 2008 witnessed 57 such transactions totalling USD 6.4 billion, with a further USD 15.6 billion worth of deals announced at the height of the buyout boom in 2007.

Nevertheless, the asset class has brokered several noteworthy transactions in 2009 with the largest deal seeing a consortium of financial investors including Novartis Bioventures exiting their investment in the biotech company ESBATech. In a deal valued at USD 589 million, the consortium sold out to the abovementioned Alcon Laboratories.

Not long ago, private equity houses were virtually undefeatable in auctions and prided themselves on being able to deliver above market returns. Funds have made lucrative returns over the last five years although it is certainly no secret that the ability to do deals and achieve stellar returns has largely hinged on the availability of cheap credit, something that has become a scarce resource in the post-financial crisis era.

Despite the relative dearth of recent financial investor activity, private equity as an asset class is still undoubtedly valuable to the wider market. Buyout houses are set to adopt a ‘back to basics’ approach with increased focus on improving operational efficiencies at portfolio company level rather than deal origination and financial engineering. Significantly, the asset class has a proven track record of adapting to changing market conditions and activity in 2010 may well increase, particularly over the second half of the year.

In terms of financing options, while it is difficult to obtain leverage for transactions, it is by no means impossible. Leverage of up to 3xEBITDA is available but private equity houses will have to talk to a number of banks before being able to agree a debt syndicate. In turn, this is lengthening the timeframe of transactions and as a result, an increasing number of funds are now taking an initial 100% equity stake in an investment with a view to refinancing the debt when conditions improve. Such an approach is beneficial as it enables private equity houses to act with relative speed when there are attractive opportunities in the market.

However, the limited availability of suitable targets has been a further challenge to private equity besides the debt financing environment. Indeed, many companies that would make attractive targets for financial investors are opting not to sell due to depressed valuations while, compared to its European neighbours, there is also a relative lack of distressed assets in Switzerland. The lack of willingness to sell on the part of many vendors could be a major source of frustration for private equity given that the Swiss market offers a number of very attractive targets. While many such targets are relatively small in terms of size, they are often key players in their field. Further, such firms are generally cash rich with a strong balance sheet, making them an attractive play for private equity funds.

It would appear however that there is light at the end of the tunnel for the asset class in Switzerland in the form of a generation shift. This is also being seen in several other European countries such as Germany with the issue of succession placing attractive businesses within reach of investors. In terms of individual segments, the Machinery, Tool Manufacturing and Healthcare sectors will all likely experience an uptick in buyout activity in the coming months. (Tobias Valk, Partner, Head Transaction Services)

IPOs

Last year’s financial crisis effectively put an end to the market for initial public offerings (IPO) the world over. However, there are tentative signs of recovery. Reports are emerging that Blackstone is planning to list a number of its portfolio companies in 2010. These claims are widely being treated as ‘canaries in the coalmine’ and there is an expectation that if these IPOs are a success, an increasing number of companies will consider public listings and other capital markets instruments.

This is also true for the Swiss market, which saw very few IPOs in 2009. One of them was the listing of the airline catering business, Gategroup, in May 2009. The move was aimed at growing its shareholder base and allowing it to raise capital to expand.

One of the key drivers in the expected resurgence of the IPO market must surely be that it offers an attractive alternative route to exit from portfolio assets held by private equity owners. As pressure mounts on private equity firms to redistribute capital to their limited partner investors, listing the business in an increasingly buoyant equity environment could secure investors strong returns – particularly as exit multiples in trade sales might remain depressed.

The list of prospective public equity offerings by Swiss companies in the short term provides hopeful signs for the eventual revitalisation of the IPO market. A larger listing is rumoured to be Swiss Commodity Holding (SCH), an almost unheard of holding company that owns mining assets worth close to USD 800 billion.

Elsewhere, numerous private equity-backed companies are also being lined up for possible listings. There is, for example, Montana Tech Components (MTC), an Austro-Swiss industrial holding company backed by private equity outfit Austrian Global Equity Partners, which could come to market in early 2010. Stadler, the Swiss rail company in which Capvis holds a minority stake, could yet be another IPO candidate. A further potential situation is Nycomed, the Swiss pharma group owned by a group of four private equity investors. The firm is being tipped to list over the near to medium term after it failed in its bid to acquire Solvay Pharmaceuticals. Glencore, the resources group, is yet another candidate, approaching the equity market by having sold convertible bonds worth USD 2.2 billion to a consortium of investors led by the energy-focused private equity house, First Reserve. This small selection of possible stock exchange debutants in 2010 underlines the theory that IPOs in 2010 will mainly be driven by private equity funds wishing to exit their investments in a lucrative manner.

To ensure strong returns when businesses are listed, private equity funds often engage in buy-and-build strategies. A recent example of this strategy is BC Partners back-to-back acquisition of Austrian FutureLab Holding for EUR 333 million alongside a 40% stake buy in Germany’s Synlab. Both companies are laboratory service providers and BC Partners aims to merge the two businesses towards the end of the year. It would be feasible for BC Partners to further bulk up its offering in this space before exiting the merged business with an IPO on any one of the European markets in 2010. While this is not a Swiss example, it is fair to expect private equity players to pursue this strategy in Switzerland as well, particularly as there are many smaller players in Switzerland engaged in distinctly different but related fields. A buy-and-build play would therefore allow a private equity player to piece together a larger offering which would be attractive for a variety of trade players or an IPO in the long run. (Patrik Kerler, Partner, Mergers & Acquisitions)

Legislative, Regulatory & Fiscal Aspects

1. Specifications of the Swiss Takeover Board (TOB) on the new Takeover Ordinance (UEV)

The Federal Act on the Swiss Financial Market Supervisory Authority (FINMASA) brought about changes in the Stock Market Act as well as a revision of the Takeover Ordinance (UEV), which came into force on 1 January 2009. The revisions not only deal with regulations governing the procedure in a public takeover situation, but also include changes to the publication and notification duties and additional restrictions in connection with offer conditions and defence measures.

1.1 Impact on the Swiss TOB

The fact that the provisions set forth in the Federal Act on Administrative Procedure are now applicable to the proceedings before the TOB is surely an important change. It means, among other things, that the TOB is in a position to issue formal decisions as opposed to the so-called ‘recommendations’ under the earlier regime. This not only strengthens the position of the TOB as one of the key stakeholders in a public M&A transaction but also the position of those offer recipients, holding at least 2% in the target company, since they now have the possibility to claim a position as party in the procedures before the TOB, which means that they have certain additional rights.

1.2 Impact on the parties

The changes of the publication and notification duties include, among other things, the obligation of the parties to provide daily updates throughout the course of the offers with details of each single transaction in the equity securities of the target company and – as the case may be – in the securities offered in exchange. All these notifications will then immediately be published on the website of the TOB. These changes mean a considerable improvement of the transparency as far as dealings with the shares in the target company are concerned.

The revised Takeover Ordinance sets forth that (i) offer conditions will only be permitted if the offeror can show a reasonable interest in the target and explicitly states that (ii) transactions with own equity securities and securities offered in exchange, if any, belong to the prohibited defence measures of the target company and are only allowed in exceptional circumstances.

1.3 Examples

In the course of 2009, the TOB had the opportunity to decide on a number of deals brought before it. While the specifications of the TOB on the existing practice as well as on the new Takeover Ordinance brought about some relief for the offeror and the takeover process, it confirmed in two important areas the protection of the public or minority shareholders.

Examples for decisions belonging to the first group are the decision on Esmertec AG, in which it was established that tag along and drag along clauses in shareholder agreements do not as such lead to a common control of the company by such shareholders. This means that such shareholders do not form a group obliged to make an offer. The TOB also granted relief to the offeror in connection with conditions, by allowing, for example, in the decision on Jelmoli, a condition which served the purpose of hedging the legal assessment of facts relevant to the offer.

Decisions which improved the protection of the public or the minority shareholders concern the application of takeover law and the liquidity of securities. The TOB has confirmed in two decisions its former practice to apply takeover law to non-listed shares where the offer refers to listed shares from an economic point of view (Hammer Retex; JJM Participations SA). As far as liquidity is concerned, the TOB and, after appeal, the Swiss Financial Market Supervisory Authority (FINMA) declared shares of a target company to be illiquid due to a low trading volume and lack of financial information although such shares had been traded on more than 30 days prior to the publication of the offer. The decisions of the TOB and the FINMA are based on the grounds that the regulations of the Takeover Ordinance do not protect the liquidity as such but the exit price of the minority shareholders which means that the minimum price in the offer must be determined on a solid basis. If there are doubts about the minimum price the shares have to be considered illiquid even if they were traded during the period stipulated by the Takeover Ordinance (Harwanne). (Joerg Kilchmann, Partner, M&A Legal)

2. Changes to the Swiss Tax Environment

The new Swiss VAT Act coming into force on 1 January 2010 includes far-reaching changes and also opportunities for companies.

2.1 Input VAT deduction on transaction costs for M&A projects

Going forward, expenses incurred in relation to acquisitions or sales of investments or in connection with restructurings will generally not be subject to a reduction of the allowable input VAT deduction, as long as these costs are incurred in the course of the business activity and relate to a subsidiary generating at least partially a taxable turnover. Investments have to be distinguished from securities sales which result in a reduced input VAT deduction.

2.2 Changes for holding companies

Today’s problem of holding companies is that they either are not considered as subject to VAT or have to suffer an input VAT reduction due to the receipt of dividends and sales of investments. This will change since the acquisition, holding and sale of investments shall be considered as business activities and a holding company will be regarded as subject to VAT, irrespective of its further activities.

Dividend income will, in most cases, no longer result in a reduction of the input tax deduction. In addition, a holding company can take the business activities of its subsidiaries into account in order to determine its own input VAT relief. This rule shall serve as a simplification for the calculation of the input VAT and has a high potential to optimise the input VAT quota. The practical application of this new rule by the tax authorities, however, is not clear yet.

2.3 Limitation of liability for VAT group members leaving the group

A company leaving a VAT group will no longer have the joint and several liability for VAT liabilities of other companies in that VAT group, but only for the tax liabilities arising from its own business activities. This therefore reduces the risk of an acquirer of a company which is a member of a Swiss VAT group.

2.4 Changes for the notification procedure

Certain restructurings or related party transactions can be declared in a notification procedure rather than paying the VAT and claiming input VAT in order to avoid a cash out for the involved parties. The rules will be partly extended under the new law.

2.5 Changes in the procedural law

One important change in the procedural law is the introduction of the right to request a tax audit which has to be performed within two years. This enables an acquirer to gain security on the VAT risks of the acquired group in a reasonable time frame and, for example, request an escrow amount from the seller in the meantime. The effective date for this new rule will be determined by the Swiss government at a later stage. (Peter Uebelhart, Partner, M&A Tax)

Appendix

Stay up to date with M&A news!

Subscribe to our newsletter