By Pip McCrostie – Ernst & Young

Companies embrace sustainable M&A as deal markets generate renewed growth

The 13th edition of our Global Capital Confidence Barometer finds companies pursuing deals at a rate not seen this decade. As 2015 global M&A value approaches record highs, executives’ long-term growth considerations outweigh short-term concerns about market volatility.

With deal intentions at a six-year peak, executives’ economic optimism is steadfast, and companies are pursuing bolder, more innovative growth strategies.

In 2015 we have seen continued volatility in commodities and currencies, intense swings in equity markets and decelerating growth in several key emerging economies. Despite these challenges, companies remain confident about dealmaking in the current macroeconomic environment.

Almost half of companies are now looking at acquisitions beyond their traditional industry boundaries, fueled by innovative disruption and changing customer preferences. Cross-border as well as cross-sector deals will also be a big part of the M&A story. The majority of potential acquirers are looking beyond their own national borders – with intentions around deals in the eurozone strengthening.

With all signs in the deal market pointing upward, some analysts raise the prospect of a market overheating. However, executives are proceeding judiciously as they look to M&A for growth. They are conducting more thorough due diligence, including new levels of cyber risk scrutiny. And they are prepared to walk away from transactions that do not meet their strategic goals.

In short, M&A is back as an essential mechanism for generating long-term value. With global macroeconomic growth tempered and their industries perpetually challenged, executives are searching for more than organic growth. In government and global leadership circles, “sustainability” has long been a buzzword for big-picture thinking about the interdependence of nations and resources to support development worldwide. In their way, executives are pursuing their own form of corporate sustainability, reimagining their businesses to both safeguard the last decade’s cost-reduction rigor and build the next decade’s platform for growth.

Key M&A findings

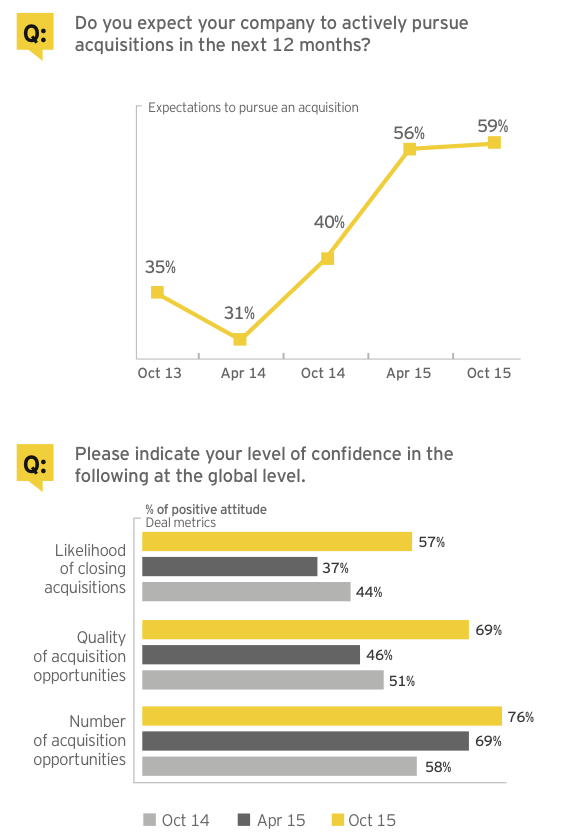

59% of companies expect to actively pursue acquisitions in the next 12 months

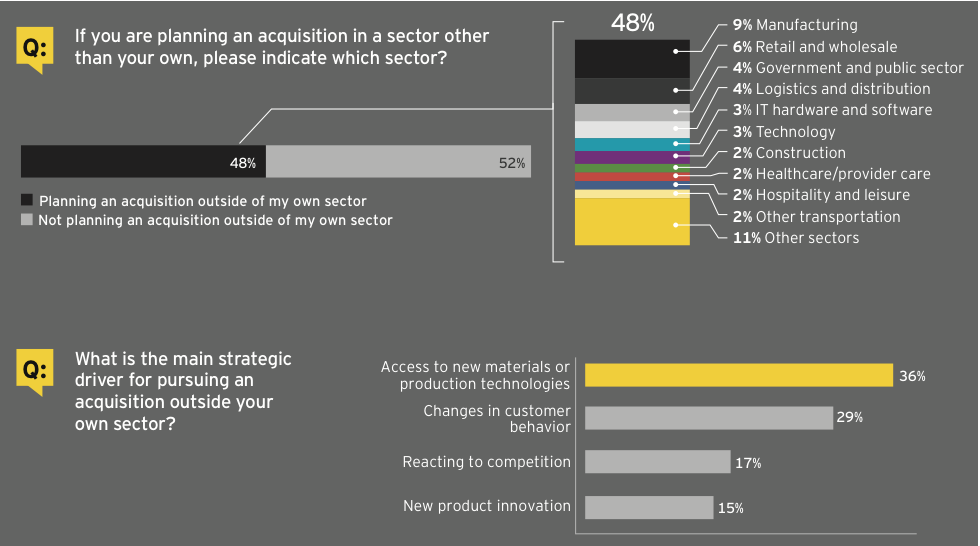

48% of companies intend to pursue acquisitions outside their own sector

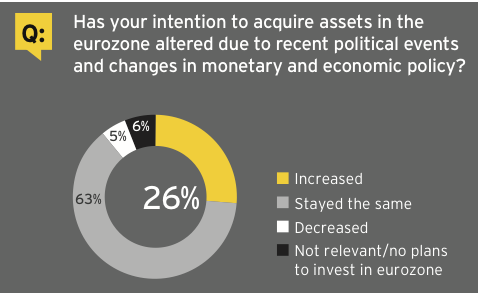

26% of companies have increased their intention to acquire in the eurozone

24% increase in appetite for upper-middle-market deals

55% of companies currently have three or more deals in their pipelines

Sectors with the highest appetite to acquire

69% Oil and gas

67% Consumer products and retail

67% Mining and metals

66% Diversified industrial products

65% Power and utilities

Top investment destinations

1. United States

2. United Kingdom

3. China

4. India

5. Germany

Macroeconomic environment

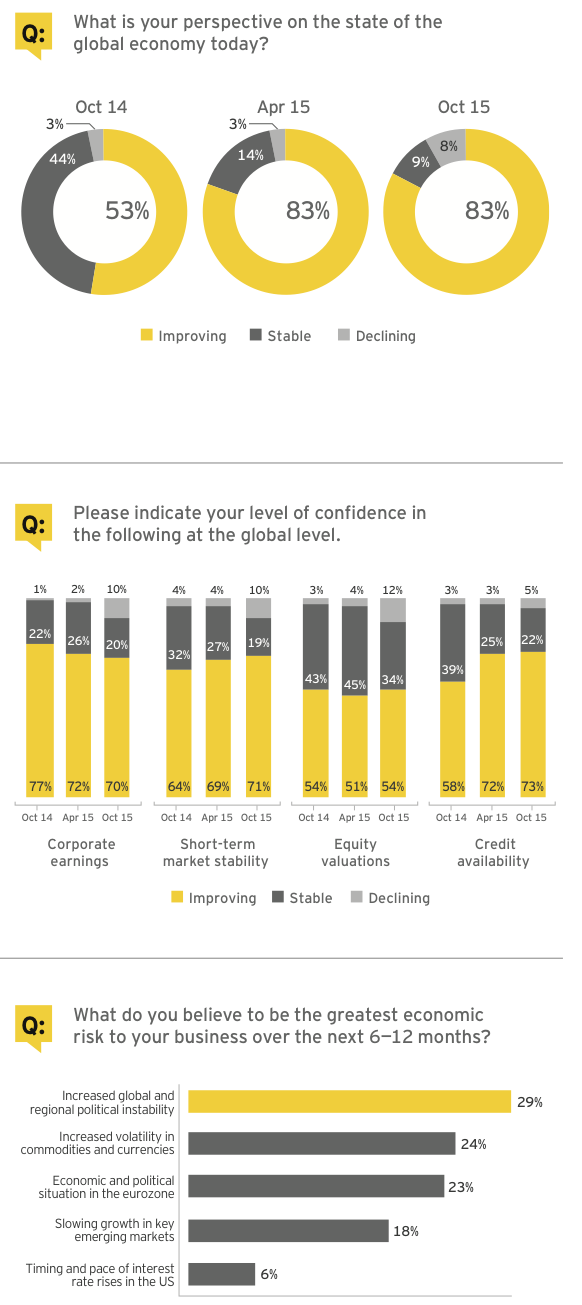

Despite significant market volatility during the survey period, companies remain confident about dealmaking in the current macroeconomic environment.

83% of executives are resilient in their economic outlook

• Executives are resilient in the face of short-term macro volatility

Having acclimatized to low growth globally, executives remain resilient about the economic big picture. Corporate leaders, whose investment decisions have impacts that span years or even decades, generally do not overreact to short-term volatility. Executives have become less sensitive to daily speculation around such issues as an emerging market slowdown or the potential timing of a US interest rate hike.

While downside risks to the global economy persist, executives remain confident that conditions are improving across many regions and countries. The vast majority of respondents anticipate some form of global economic improvement.

• Corporate earnings and other leading market indicators remain positive

Executives are looking beyond recent volatility and taking a balanced long-term view of capital markets. Notwithstanding a potential rise in US interest rates, they expect credit availability to continue to be boosted by quantitative easing programs in the eurozone and Japan, as well as policy shifts in China. If and when the US Federal Reserve begins to raise interest rates, most analysts believe it will be gradual and data-dependent, taking global economic conditions into account.

As for corporate earnings and other leading market indicators, executives are bullish. This is consistent with actual performance seen so far in 2015, as corporate earnings have generally exceeded analyst expectations. Even with recent currency fluctuations, the outlook for earnings remains positive.

• Political instability, currency and commodity volatility are key economic risks

No single outstanding issue is tainting executives’ overall macro view. Ongoing geopolitical tension in Eastern Europe, the Middle East and Southeast Asia ranks as executives’ top concern, but no issue significantly dents executive sentiment around economic confidence overall.

Currency and commodity shifts are a more immediate concern. Continued volatility in commodities challenges companies’ long-term planning assumptions. For companies reporting in US dollars, currency shifts may directly affect near-term earnings, potentially leading to negative investor impressions.

Eurozone stability remains an ever-present, evolving issue. Recent negotiations over Greek debt and the ongoing refugee crisis point to political unrest in the region, which undermines confidence in the long-term stability of the wider eurozone project.

Finally, the emerging market slowdown and anticipated changes in US monetary policy are more muted concerns, reinforcing that executives are able to see beyond short-term global volatility.

Corporate strategy

Executives are pursuing bolder investments to get ahead of the next wave of innovation.

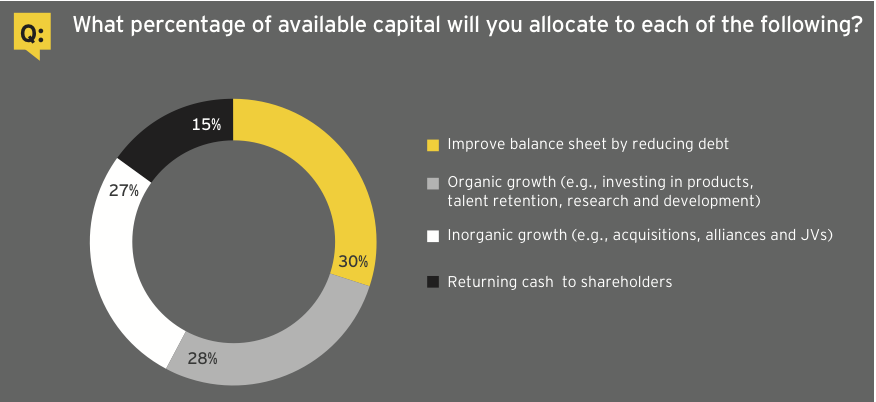

55% of available capital is allocated to support growth strategies

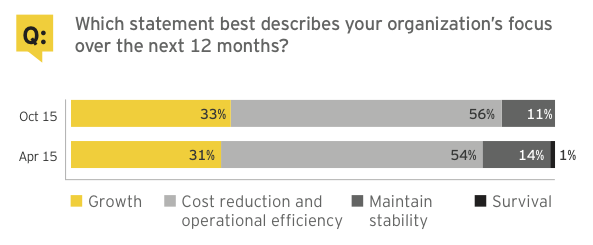

• Balancing act between growth and efficiency is here to stay

As in prior Barometers, cost efficiencies remain a permanent feature of the boardroom agenda. However, we also see a slight increase over the last six months in those focused on growth.

As acquisition activity has increased over the past year, more companies are focusing on the operational rigor required to integrate acquired businesses. Executives have learned from past upturns that timely integration of these assets leads to more efficient value creation.

With survival now clearly in the rearview mirror, executives are pursuing both growth and cost efficiency concurrently as they progress on the road to normal-state business operations.

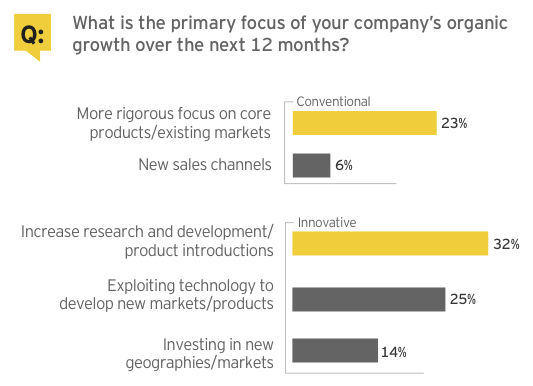

• Organic investment focus shifting to meet disruptive challenges

Executives are preparing to shift their attention toward innovative organic growth strategies. The Barometer finds that increases in R&D and exploiting technology to develop new markets and products rank highest in organic growth focus. However, executives are not losing sight of their current operations, with nearly a quarter choosing more rigorous focus on core products and existing markets as their primary growth strategy.

This somewhat more active pursuit of new products and services provides evidence of executives’ boldness in an increasingly complex marketplace. Even those companies not using M&A as a means of countering disruptive forces are moving to develop technologies and expertise that will enable them to remain competitive.

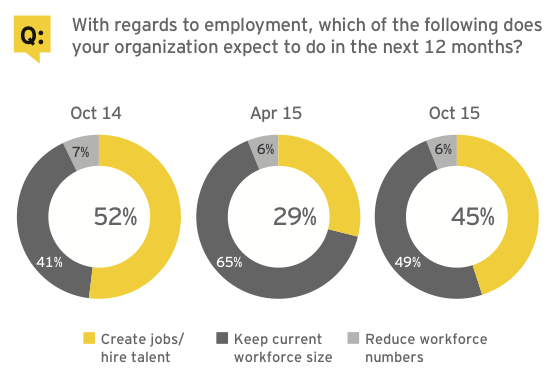

• Companies remain focused on talent retention, but positive hiring intentions rebound

Executives’ confidence in the outlook for the global economy is driving most companies to retain or grow their workforce. This finding is consistent with reported employment growth in the US and UK and an improving situation in the eurozone.

This Barometer also finds that, somewhat contrary to popular belief, corporate emphasis on digital evolution can coexist with positive sentiment on job creation. Technology opens up new business segments and revenue opportunities, which can counteract the side of digital evolution that undermines employment.

Capital allocation: Fundamental global changes reshaping corporate strategies

• Companies are considering a full range of opportunities for allocating available capital

The effective allocation of capital is a senior management team’s most fundamental responsibility. In a time of modest global economic growth, executives are taking extra care to balance their allocations to support long-term strategic goals. A typical capital allocation strategy also strikes a balance between long-range planning and shorter-term imperatives.

In the years immediately after the global financial crisis, many companies pursued share buybacks and other short-term measures, in many cases under pressure from large or institutional investors. While these maneuvers satisfied various constituencies at a time of market challenge, executives were reminded of a perennial truth: A focus on short-term tactics can be at odds with building long-term value.

• Balance and frequency are key to successful allocation

In this Barometer, we find executives beyond the financial-crisis mindset and employing a full range of available allocation tools. They are balancing financial prudence (reducing debt), rewarding existing shareholders (returning cash), and growing the business for the long term (organic and inorganic growth).

Research consistently shows that those companies with the most active capital allocation processes will outperform and ultimately achieve higher returns than those with more passive or infrequent allocation approaches. In the new-normal environment of tempered global growth, continual reassessment of where to deploy and recycle capital is how companies sustain their growth trajectory and maximize value.

Companies with the most active capital allocation processes are consistently shown to outperform those with more passive or infrequent allocation approaches.

Boardroom agenda: Low-growth, low-inflation environment compelling boardroom discipline

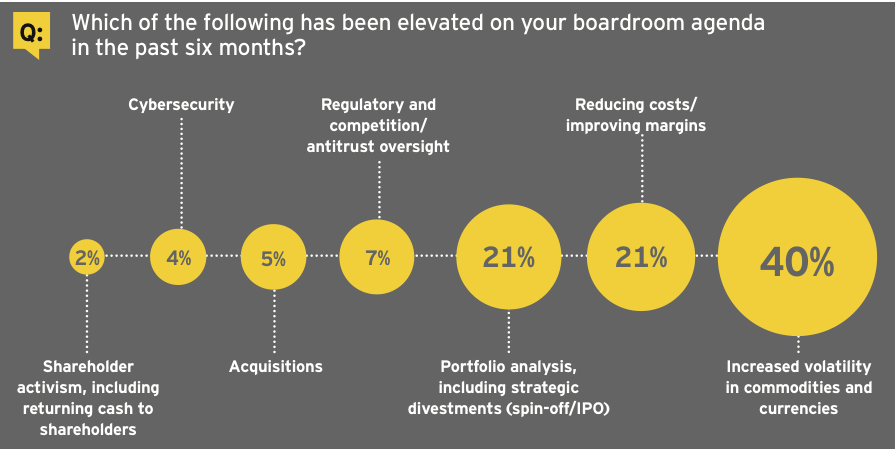

Executives have accepted the reality of a low-growth global economy and the impact of this environment on their current operations. Greater currency volatility and fluctuations in commodity pricing are causing many to allocate their valuable boardroom time to protecting the bottom-line achievements generated over the last half-decade.

Strategic divestment and related portfolio strategies are moving higher on the boardroom agenda, due in part to the ongoing influence of shareholder activism. Interestingly, activism has become so deeply entrenched a feature of the corporate agenda that it is now drawing minimal direct boardroom focus. According to data from S&P Capital IQ, more than 95% of companies in the S&P 500 have activists on their share register. In the UK, more than half of FTSE 100 companies have activist shareholders onboard, and for companies on the German DAX the total is more than one-third. Similarly, over the past few years, acquisitions have become a mainstay of boardroom considerations.

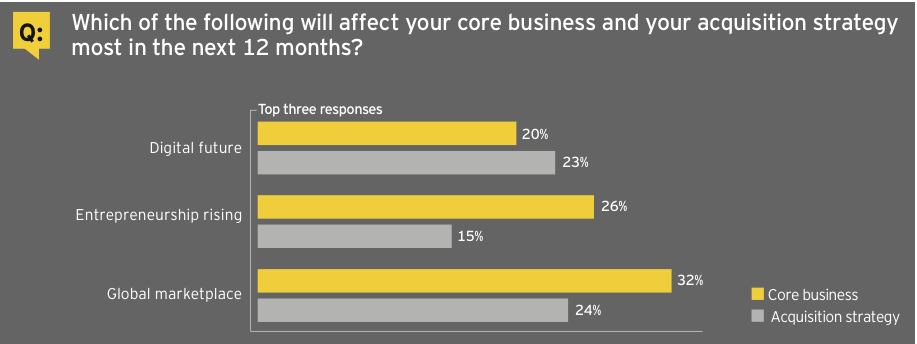

Globalization, entrepreneurship and digital have greatest near-term impact

Among the megatrends affecting companies’ core business and acquisition strategies in the near term, the growth in economic influence of China, India and the wider Asian economy is expected to have the greatest impact. Additionally, the emergence of a more decentralized, entrepreneurial working world is having impacts executives are only beginning to grapple with.

Fueled by the convergence of social, mobile, cloud and big data technologies, as well as growing demand for anytime–anywhere access, the digitalization of the enterprise is disrupting all areas of corporate strategy.

M&A outlook

Deal intentions, pipeline depth and deal size are all growing as companies take advantage of robust dealmaking conditions — but the new M&A market is led by companies intent on strategic fit and focused on execution.

59% of companies intend to pursue acquisitions in the next 12 months

• Highest appetite to acquire in six years…

After a record increase six months ago, the number of executives planning to pursue acquisitions not only holds its gain but rises slightly, remaining well above the Barometer’s long-term average. While the rate of increase has moderated, the continued upward trend indicates a sustained appetite for dealmaking.

• …but prudence prevails

Deal fundamentals are also up across the board, with particularly strong increases in the number and quality of acquisition opportunities and the likelihood of closing deals.

What distinguishes this market from prior M&A booms is its judiciousness. Executives are not pursuing deals without a strong strategic rationale, and they are prepared to walk away from those that do not have one. We see further evidence of this discipline in the deal metrics, which, while high, are not yet at levels seen in previous market upturns.

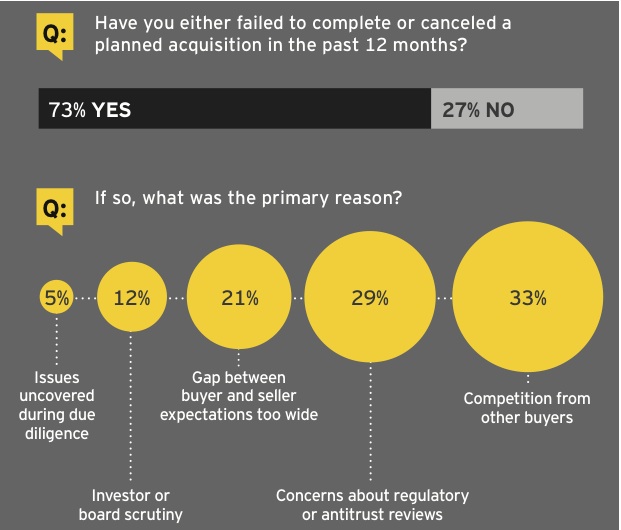

Prepared to walk away

• Executives’ willingness to withdraw from an acquisition underscores maturity and stability of M&A market

Current levels of M&A activity are prompting concern for an overheating deal market. Lessons have clearly been learned from prior M&A cycles. Companies in our survey report a strong willingness to withdraw from deals that are not fully aligned with their strategy. This is a sign of a market that is sustainable.

Heated buyer competition is the top cause for walking away from deals. Companies are prepared to withdraw rather than overpay for assets. Concern over regulatory scrutiny ranks a close second, as we see the effect of increased intervention by antitrust regulators. There has been an increase in the number and the complexity of antitrust reviews. It has also become standard procedure for acquiring companies to assure markets of limited competitive impact or plans for mitigating via divestment of selected assets.

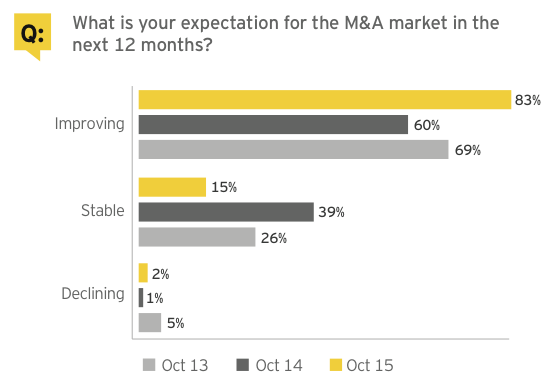

• Changing market dynamics encourage dealmaking sentiments

Our current survey shows positive deal-market sentiment accelerating, with a particular shift in the past 12 months from those expecting stability to those anticipating greater activity. This dovetails with other market trends highlighted in this Barometer. The disruption of business models, the blurring of sector boundaries and the drive toward sector consolidation in search of growth are all combining to lift dealmaking at or above record highs.

The vast majority of executives predict the global M&A market will thrive in the next 12 months. This sentiment is driven by executives’ positive outlook regarding the global economy and their resilience in the face of a persistently low-growth environment.

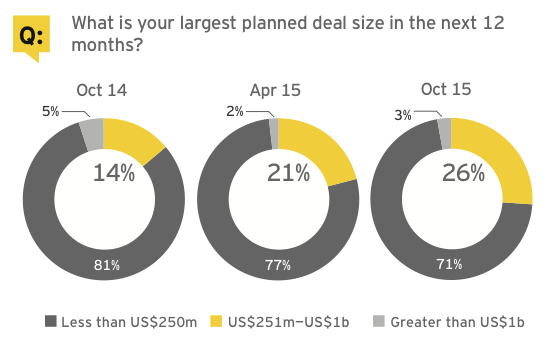

• The real action is in medium-size deals, but megadeals remain prominent

The vast majority of planned investments are forecast to be in the lower middle market. However, the trend since 2014 has been toward more upper-middle-market deals (between US$250 million and US$1 billion), which now make up more than a quarter of planned M&A. This trend corresponds with the direction of the 2015 year-to-date M&A market: We have seen an increased number of deals across all value ranges, except those below US$50 million.

Deals valued at more than US$1 billion dominate current M&A headlines. But while these megadeals are a vital component of total M&A transacted value, they make up a small proportion of the total population of deals. Executives do expect more of these megadeals over the next 12 months, even as only a small percentage of companies plan to pursue them.

Pipelines continue to grow

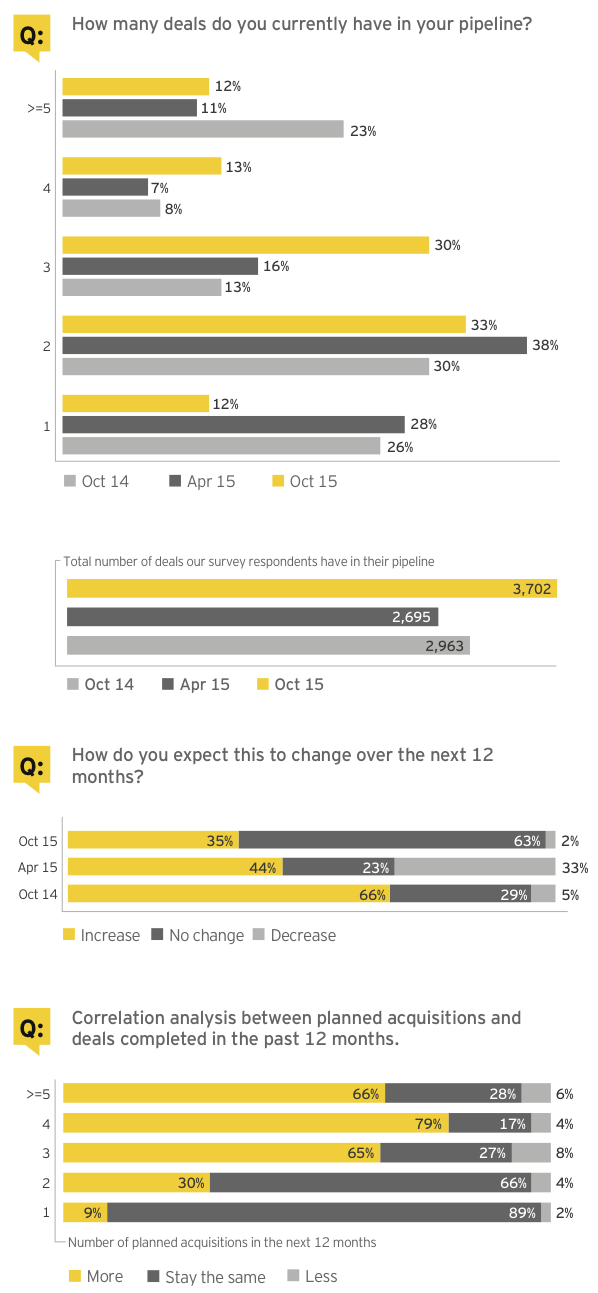

• Growth in deal pipelines mirrors improved M&A sentiment

The past 12 months have brought an upward shift in the quantity of deals companies are considering, with three- and four-deal pipelines up strongly from a year ago. The number of companies with more than five deals in their pipeline has also increased.

Looking ahead, we find a majority of companies expecting no change in deal pipelines, likely due to their already robust activity.

• Companies that have returned to dealmaking accelerate activity

The prior Barometer showed a large number of companies returning to dealmaking after spending much of the post– financial crisis years on the sidelines.

The correlation analysis below maps planned acquisitions against deals completed in the past 12 months. It reveals that those companies that recently returned to dealmaking are continuing, and even accelerating, their activity.

As we move deeper into a sustained deal-market upturn, executives are more comfortable with M&A as a driver of growth. We see strong evidence of companies planning to pursue more transactions in the next 12 months than they completed in the prior year.

Executives are more comfortable with M&A as a driver of growth.

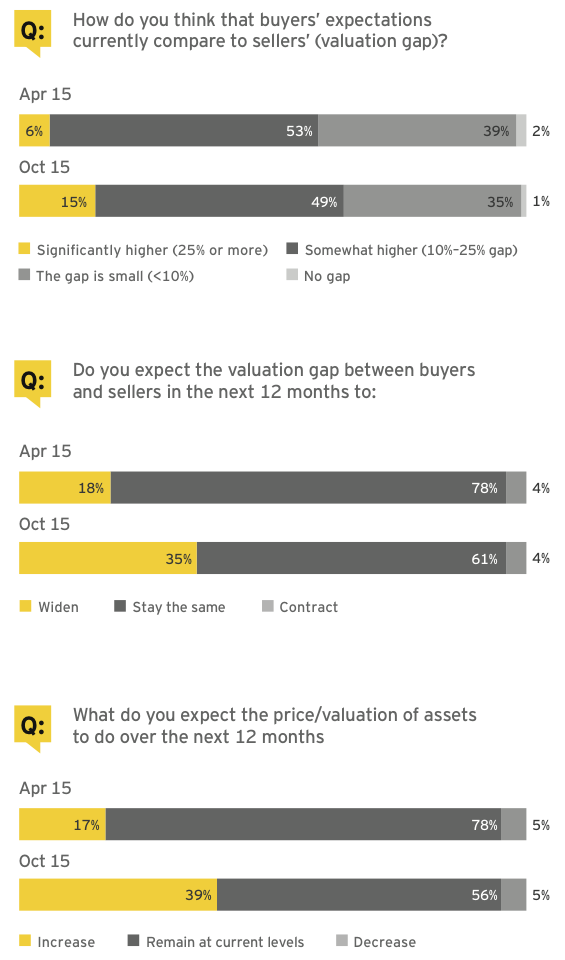

Manageable valuation gap supports dealmaking

When asked how buyers’ expectations compare with sellers’ view of asset valuations in the current market, most respondents see a sizable gap. Nearly two-thirds see the valuation gap as greater than 10%. However, that response is consistent with that of our previous Barometer.

Executives see beyond near-term volatility

As might be expected in an active deal market, asset valuation multiples are elevated compared with historic levels. But they are not yet at the peaks seen in previous M&A highs. Executives appear to be maintaining a relatively confident attitude toward asset valuations. Most see the recent correction in global stocks as temporary, and they expect asset prices to revert to levels seen in early 2015.

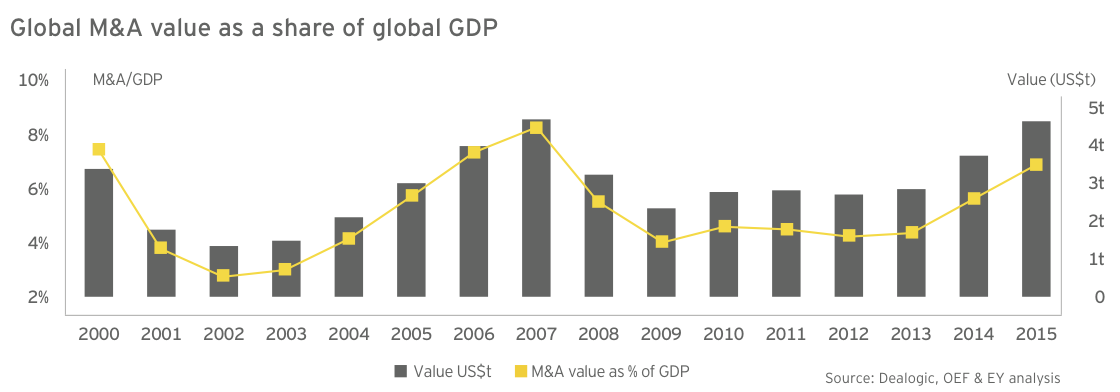

Similarly, EY analysis demonstrates a strong relationship between M&A value and gross domestic product and finds headroom in this current cycle (see below). That is particularly true if the eurozone returns to previous levels of dealmaking and China fulfills its potential. In short, as with the global economy, executives are able to see beyond near-term volatility, and this deal market still has some way to run.

Global macro trends affect asset values

One area that may have a deeper impact on valuations is the timing and pace of rate normalization by the US Federal Reserve, which will have a direct impact on the cost of capital. Even here, executives believe rate increases will be gradual, data-dependent and reflective of global economic conditions.

Valuations also differ widely by geography and sector, differences that may spur share-based deals and bring new opportunities to the table. In the eurozone, while rising valuations are a drag on M&A, other stimulus in the region, particularly the current program of quantitative easing, should offset this. Similarly, headwinds in emerging markets, especially a slowing China, coupled with downward pressure on commodity pricing will likely be more than offset by attractive asset valuations in those markets.

Deal challenges and risks: Significant challenges still pose risks to deal success

• Integration and poor cost assumptions are biggest challenges

Companies are increasingly buying assets outside of their core business. As a result, they are often acquiring assets that may be difficult to fit into their current operations. Integrating a new acquisition into optimized structures to realize cost synergies is a delicate exercise. This may require unbundling of key processes and rebundling to fit a buyer’s operating model. Companies can exploit revenue-based synergies if the merging businesses either find they can command a price premium via enhanced capabilities (such as product innovation or time to market) or they boost sales volume through increased market coverage (by geographic or product-line extension). However, these same synergies can be undermined if the integration is rushed or insensitive to the acquired company’s market and culture. For example, sufficient time must be spent on preserving acquired brand value and customer relationships.

Poor operating cost assumptions rank highly among the factors leading to deals not meeting expectations. Companies are often challenged in estimating the future run rate for an integrated asset, with overreliance on benchmarks as a foundation for cost modeling.

• Integration faces further digital challenges

As companies increasingly acquire digital assets with different cultural and operational models, integration becomes even more challenging. The need to retain acquired talent and expertise is paramount. Integration considerations have long needed to be part of the front-end deal strategy – now more than ever in an increasingly digital world.

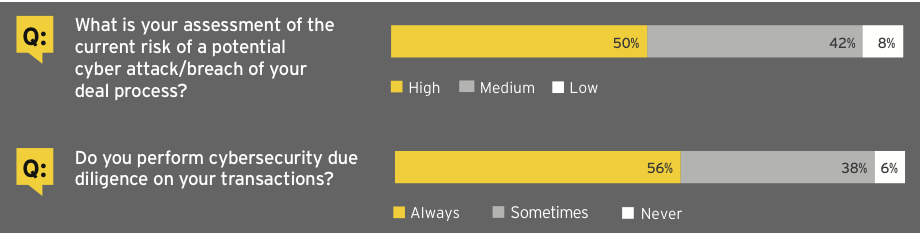

• Cyber attack fears impact dealmaking

Heightened media attention and greater corporate awareness of cyber risk are contributing to increased scrutiny at the C-suite and board level. More than 90% of executives view cybersecurity as a significant risk, either medium or high, to their deal process. A majority of companies perform cybersecurity due diligence as a standard procedure. They are increasing their focus outside of IT when considering cybersecurity risks integration diligence opportunities no impact to transactions. Areas of focus include business relationships such as customers and vendors, as well as joint ventures and affiliates of the target company.

Sector outlook: Strong deal sentiment across many sectors

Commodity price volatility providing impetus to pursue acquisitions in sectors with greatest exposure

Percentages reflect those who intend to actively pursue acquisitions in the next 12 months.

69 % Oil and gas

The sharp fall in oil prices during 2014 put pressure on those producers who invested heavily during the last commodity supercycle. With demand forecast to remain low and supply still abundant, many oil and gas executives are looking to strengthen their companies by focusing on financial, operational and portfolio resilience. M&A will play a major role in determining which companies survive the downturn in prices, especially in the oilfield services and midstream sub-sectors. Consolidation in these two areas has grown in 2015 and is expected to continue.

67% Mining and metals

The sector remains largely focused on portfolio management and capital returns instead of exploring options for growth. With weak commodity prices putting pressure on margins, earnings and debt serviceability, the sector continues to be cautious against countercyclical investment. Mining companies are now facing tougher scrutiny about their investment and funding decisions than ever. However, those companies that are cash-rich and with lower levels of debt are beginning to look at attractively priced assets, with a close eye on future growth potential. Private equity and other alternative investors are also looking to acquire in the sector while prices remain subdued.

65% Power and utilities

Innovations in both financing and technology are emerging drivers of transaction activity in the power industry, and utilities are responding by adapting their traditional business models. Spinoffs of conventional generation, trading, and exploration and production businesses highlight utilities’ willingness to change and to move toward growth opportunities. Institutional investors and private equity firms are also playing an increasingly important buyside role in the sector. Regulatory changes in Europe have created a challenging new operating environment for utilities. This has put divestment and redeployment of capital at the center of the utility agenda. Disruptive trends such as digitization, distributed energy and empowered customers will continue to influence deal activity and asset valuations.

67% Consumer products and retail

In the absence of ample growth avenues for mature brands, consumer products companies are focused on portfolio optimization as a critical theme. Companies have sharpened their focus on developed-market businesses, and large players are optimizing their brand portfolios and market exposure by disposing of non-core and lower-growth businesses. These companies are rechanneling investments into acquiring or expanding within faster-growth or higher-margin segments.

66% Diversified industrial products

As growth in industrials is typically tied to gross domestic product, M&A is often necessary to achieve above-market returns in this industry. Consolidation in high-end capital goods has been a significant trend, and we have also seen high demand for emergent technologies such as undersea mining equipment, especially from companies in China looking to move up the value chain. Given the low-growth environment, portfolio management will continue to be a major focus, especially for those industrials companies affected by recent volatility in energy prices. For these companies, cost reduction remains an imperative, due to pressure on topline growth.

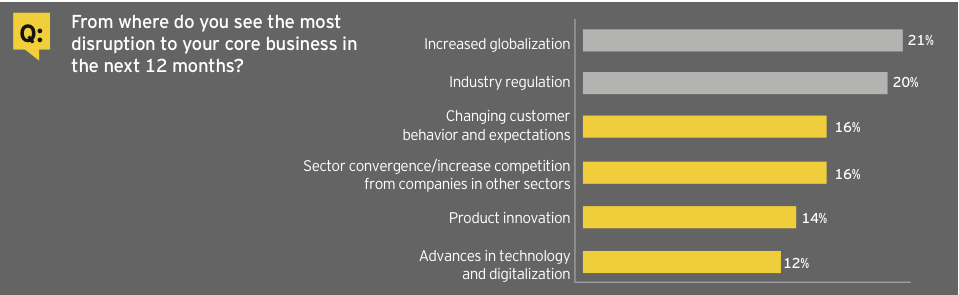

Sector disruption: Companies look for growth amid disruption

• Executives reassessing business models in response to changing customer behavior and evolving technology

As consumer preference and geographic shifts rewrite the rules in many sectors, executives find themselves working harder to stay ahead of their customers. They are also adapting and responding to technological and regulatory change. These trends have compelled many companies to cross sector lines, and M&A is often the easiest path to that objective.

• Convergence of industries spurs companies to consider cross-sector M&A

As traditional sector boundaries blur, particularly around technology and industrial processes, it is not surprising that nearly half of the executives we surveyed are considering acquisitions outside their own sector. Acquisitions into manufacturing segments were the most cited. Second was retail and wholesale, followed by government and public services acquisitions, which are often achieved through privatizations and public–private partnerships.

We also see strong demand to invest in technology and other intellectual property–driven sectors.

Accordingly, several factors are influencing companies to pursue those cross-sector acquisitions. Changes in customer behavior are shifting competitive dynamics within sectors, as are similar moves made by competitors. In these scenarios, companies use M&A as a mechanism to protect market share, or in response to evolution in 52% production elements or technologies.

Many companies looking further afield for deals

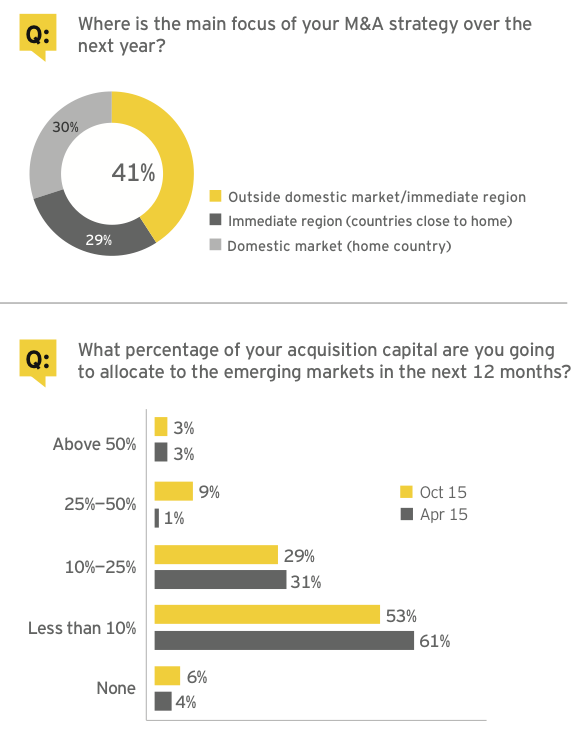

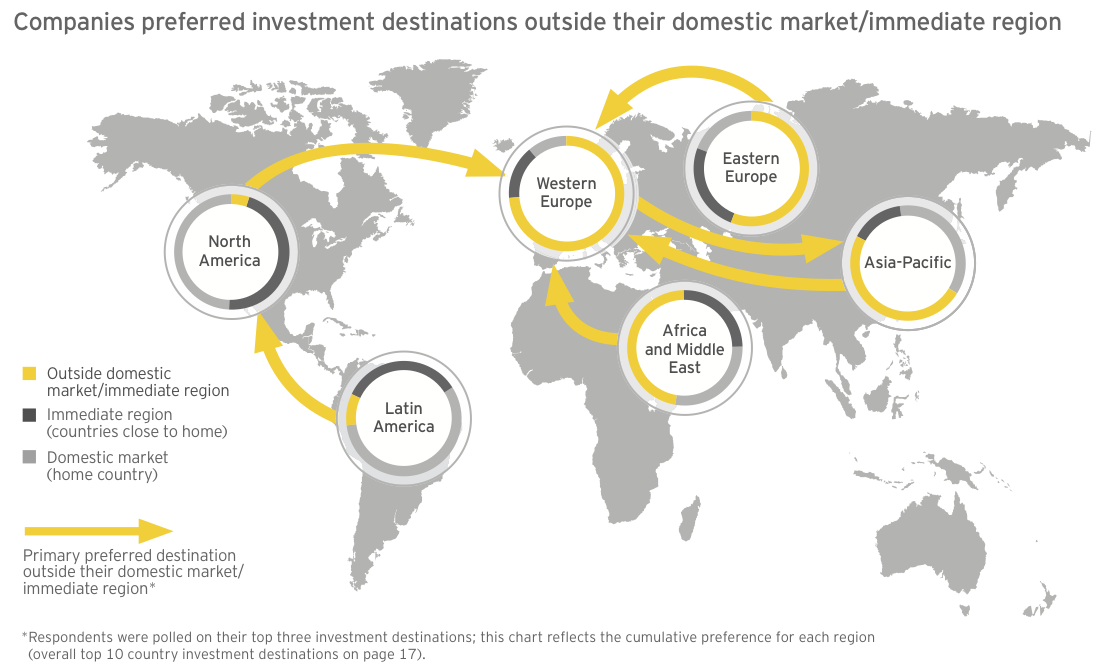

• Amid globalization, executives consider all locations for acquisitions

While one-third of companies are planning to acquire in their home country or domestic market, a larger number are looking not just across borders but outside of their immediate region entirely. This is unsurprising in a fast-moving and increasingly divergent global economy.

• Focus of allocation still on developed markets

The majority of allocation for global investment remains focused on developed markets. However, we still see a modest increase in appetite for higher-risk global investment.

Recent currency swings and lower equity valuations in emerging markets have raised concerns. However, from a valuation perspective, these changes have also made emerging market assets more attractive. A significant number of our respondents plan to allocate at least 10% of their acquisition capital to emerging markets — up six points from the last Barometer.

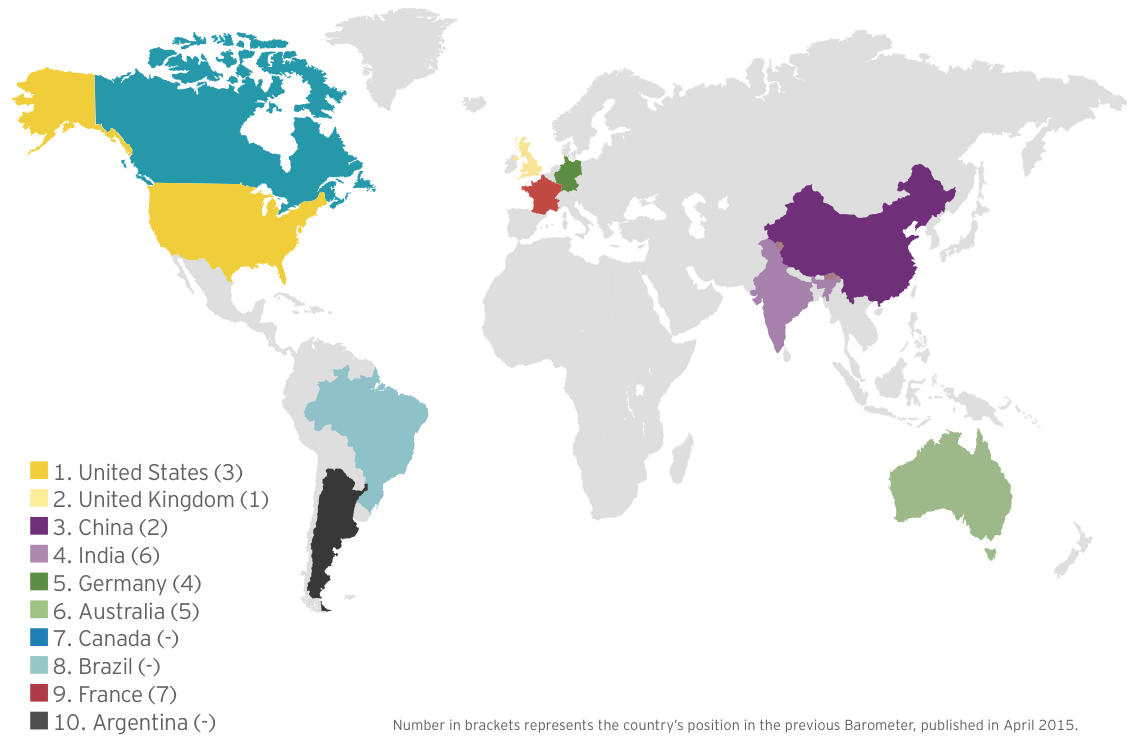

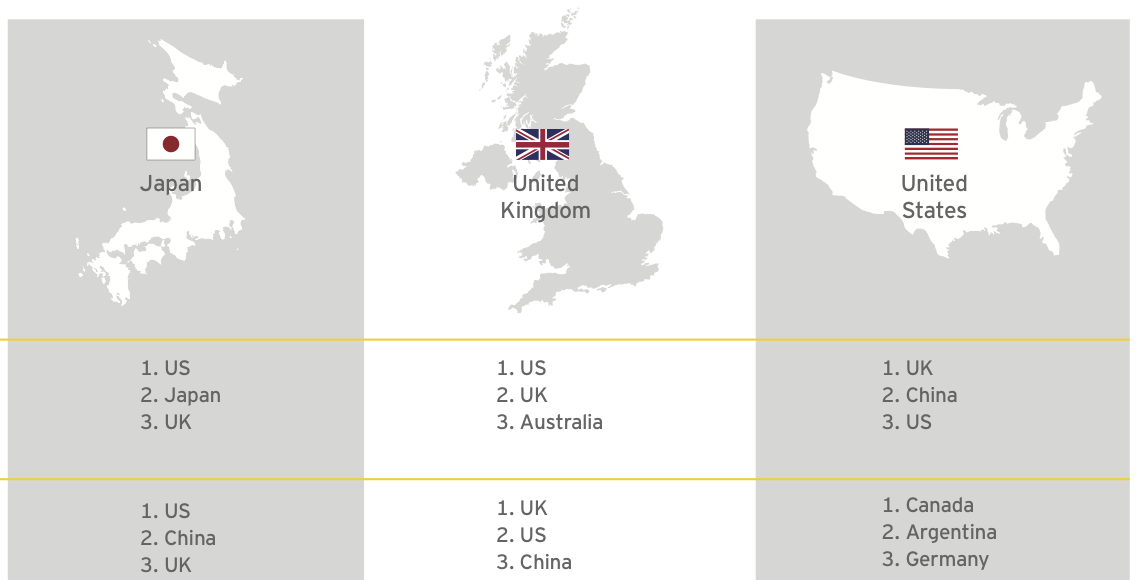

Top 10 investment destinations

Stronger growth in the United States and the United Kingdom and the attractiveness of high-quality assets in Germany are making these countries popular investment destinations. China and India also remain attractive destinations for investors, notwithstanding recent concerns about the wider Asia-Pacific region’s economic growth and stability.

Eurozone investment appetite increases

More than a quarter of executives have increased plans to acquire assets in the eurozone. This is in part due to companies “catching up” on planned acquisitions in the region following a period of instability, and attractive pricing due to currency fluctuations. The ongoing program of quantitative easing by the European Central Bank may also help improve dealmaking in the eurozone.

Strengthening growth across the area, together with changes in the euro exchange rate and local asset valuations, will make this a dynamic and fast-moving market for deals in the near term. We could see further inbound investment from China, the US and Japan.

While it may be the world’s largest single market, the eurozone’s wide range of economic conditions and business environments means investors are picking and choosing where to invest.

Top M&A markets and their key characteristics

Even amid headlines over its recent economic slowdown, mainland China retains its status as an attractive destination. This is due to levels of growth that remain very strong relative to the global economy. The Chinese Government now targets annual growth at about 7%, down from previous rates that ranged as high as 10%. With economic rebalancing a stated Chinese policy, further investment opportunities should arise for inbound investors. As for outbound investment, lower domestic growth, combined with increasingly assertive, cash-rich Chinese companies, should compel China-based enterprises to invest capital overseas. The government has also introduced a range of measures to encourage outbound acquisitions, particularly targeting companies with intellectual property assets in the industrial and technology sectors.

Top sectors

Technology

Diversified industrial products

Automotive

Germany continues to be the main bright spot within an otherwise depressed eurozone. Recent economic data points to slow but stable growth, with an acceleration in gross domestic product forecast for 2016. Germany’s high-quality corporate assets, especially in the industrials, chemicals and automotive sectors, are already attractive to foreign acquirers. Also, a weakening euro promises to make these assets relatively less expensive. The main competition for these assets is likely to come from China, Japan and the US. As for M&A from within Germany, acquisitions by German companies have historically focused on the domestic market. However, we are beginning to see an increase in cross-border acquisitions, especially investment in US assets.

Top sectors

Diversified industrial products

Automotive

Power and utilities

Even as the outlook for many emerging markets turns negative, investor sentiment toward India is seeing a significant recovery, with the country’s deal market expected to improve. The Indian Government’s pro-business stance and an increasingly promising economic outlook should foster a more benign investment landscape for inbound investment. Several positive macroeconomic factors are also burnishing India’s investment outlook. Low oil prices will help shrink the country’s import bill and narrow its current-account deficit. Easing inflation and looser monetary policy are expected to encourage consumer spending and investment. On the whole, India’s status among global investors as one of, if not the, most attractive emerging markets should also boost growth.

Top sectors

Technology

Consumer products and retail

Automotive

Japan continues to suffer from weak domestic economic growth combined with persistently low inflation. However, recent policy decisions by the Japanese Government and the Bank of Japan have reinforced policymakers’ determination to resolve the country’s economic malaise. While gross domestic product is expected to return to growth in 2016, Japan faces increased exposure to the slowdown in China, a key market for Japanese exports. In the deal markets, Japanese companies have increasingly shifted toward outbound acquisitions, especially in the financial services, industrials and consumer products sectors. This shift has been coupled with a small increase in inbound acquisitions into Japan, mainly by private equity investors but also in combinations involving US and Japanese companies in the technology and real estate sectors.

Top sectors

Diversified industrial products

Automotive

Technology

The United Kingdom has long been a favored destination for foreign firms accessing the wider European Union. With strong domestic growth in 2015, similar levels forecast through 2016 and a focus on reducing red tape, the UK should be able to maintain its unique status as a global M&A hub. Among leading UK sectors likely to engage in M&A, life sciences and technology companies are strong innovators, the financial services sector is robust, and consumer products companies are globally recognized. Companies in all of these sectors should be looking to make acquisitions both domestically and abroad and will be attractive to foreign acquirers. As for downside risks, the impending UK referendum on EU membership, as well as uncertainty regarding the timing of an expected interest rate increase, may check the deal markets.

Top sectors

Consumer products and retail

Diversified industrial products

Technology

The M&A market in the United States is expected to maintain its upward momentum and continues to be attractive to foreign investors. Positive US economic fundamentals, and low interest rates are all strengthening boardroom confidence. US companies continue to perform exceptionally: The majority of the S&P 500 beat earnings estimates in the first half of 2015. This has kept investor morale up and driven M&A. Additionally, the US dollar’s increasing value should make outbound deals appealing, especially those focused on the eurozone, where valuation and currency differentials are most apparent. The main potential downside for dealmakers in the US concerns the timing of the Federal Reserve’s first anticipated rate hike and the overall pace of a return to normalized interest rates; however, recent announcements by the Federal Reserve have pushed back the timing on such moves.

Top sectors

Power and utilities

Oil and gas

Financial services

About this survey

The Global Capital Confidence Barometer gauges corporate confidence in the economic outlook and identifies boardroom trends and practices in the way companies manage their Capital Agendas — EY’s framework for strategically managing capital.

It is a regular survey of senior executives from large companies around the world, conducted by the Economist Intelligence Unit (EIU). Our panel comprises select global EY clients and contacts and regular EIU contributors.

• In August and September, we surveyed a panel of more than 1,600 executives in 53 countries; more than 50% were CEOs, CFOs and other C-level executives.

• Respondents represented 19 sectors, including financial services, consumer products and retail, technology, life sciences, automotive and transportation, oil and gas, power and utilities, mining and metals, diversified industrial products, and construction and real estate.

• Surveyed companies’ annual global revenues were as follows: less than US$500m (14%); US$500m—US$999.9m (25%); US$1b—US$2.9b (24%); US$3b—US$4.9b (11%); and greater than US$5b (26%).

• Global company ownership was as follows: publicly listed (65%), privately owned (31%), family-owned (2%) and government/state owned (2%).

Stay up to date with M&A news!

Subscribe to our newsletter