The third quarter of 2010 showed an improvement in the Swiss M&A market as the number of transactions as well as deal volume increased significantly. While economic uncertainties continue to persist, the general conditions for M&A transactions are assumed to become more favorable as debt availability and investor sentiment eased and interest rates are expected to remain low well into 2011.

Swiss M&A Market Q3 2010 and Outlook for 2010/2011

M&A Market Q3 2010

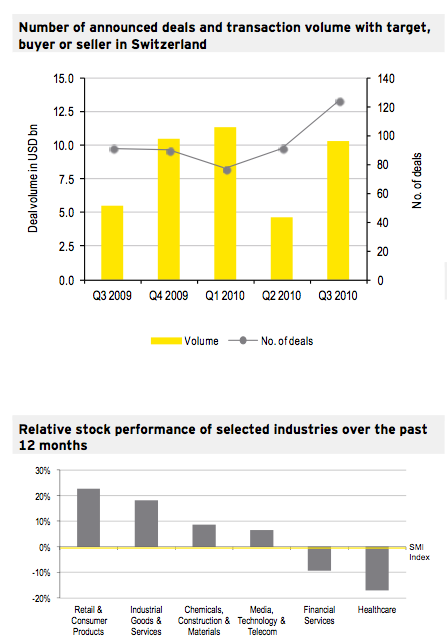

The Swiss M&A market showed signs of improvement during the third quarter of 2010. The number of transactions increased by over 35% with deal volume rising significantly by over 85% year-over-year in the third quarter of 2010.

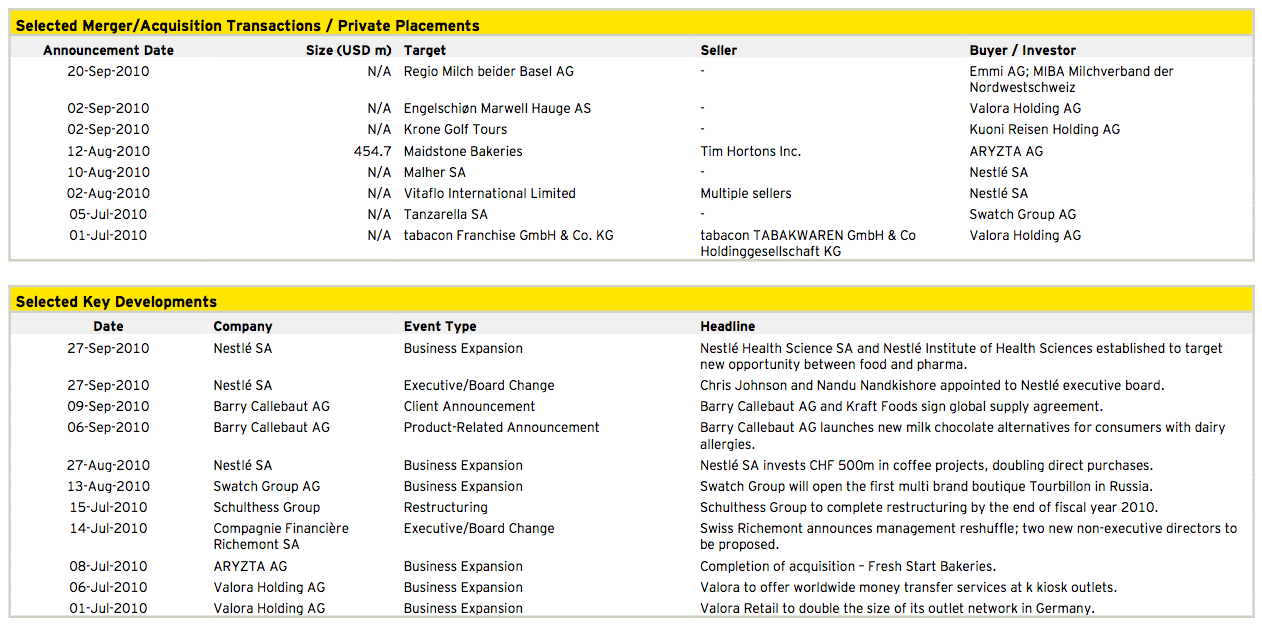

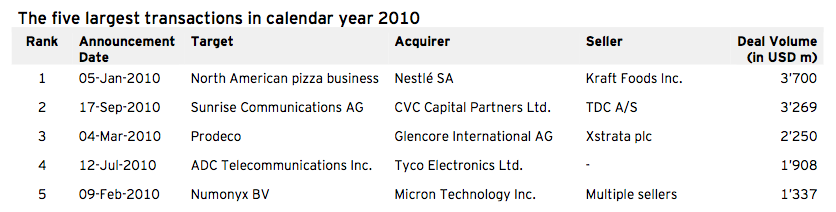

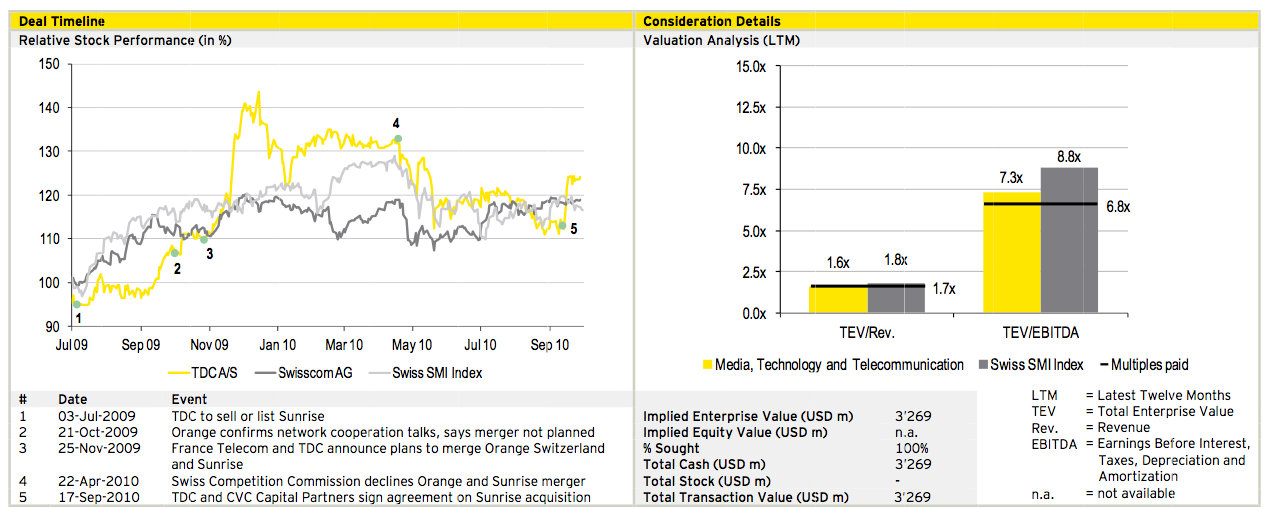

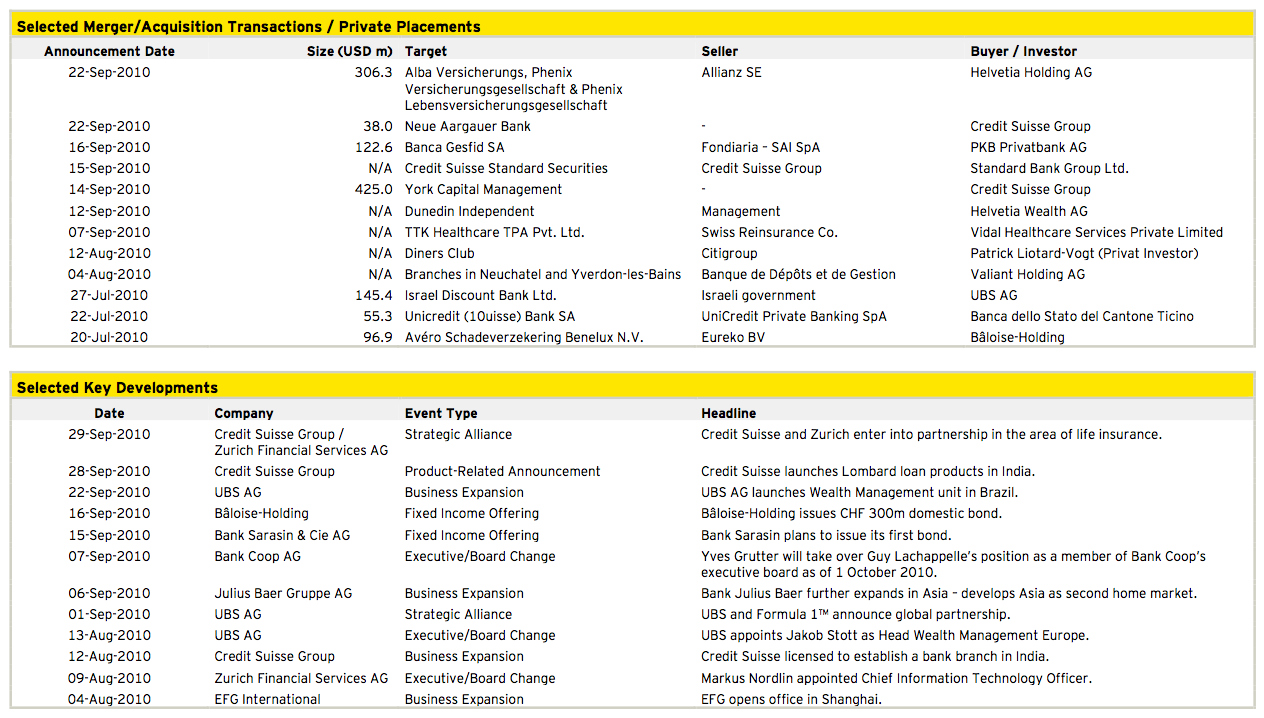

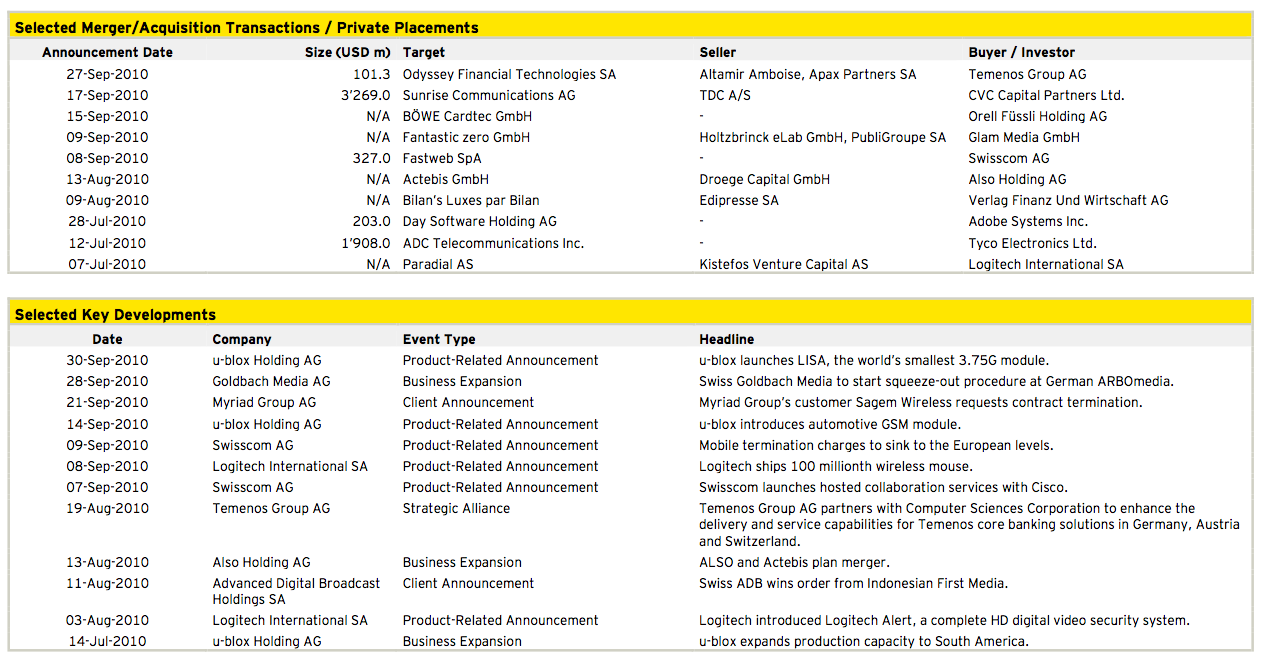

In September 2010, the second largest transaction of the current year was announced. Sunrise Communications AG will be acquired by CVC Capital Partners Ltd., a private equity firm headquartered in Luxembourg, for USD 3’269m. The transaction was announced on the heels of the Swiss Competition Commission blocking the proposed merger of Sunrise with Orange Communications SA in Q2 2010. It also illustrates that financial buyers are reemerging as acquirers in large M&A transactions.

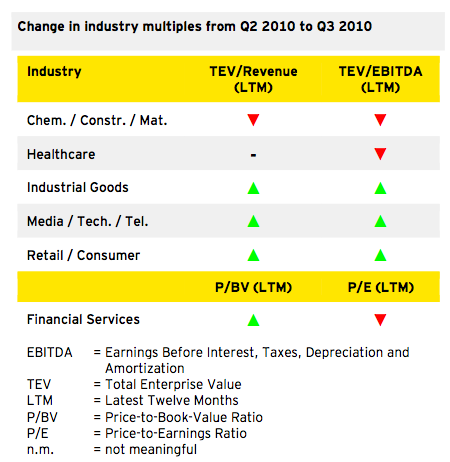

Over the past four quarters, the Swiss SMI index trended sideways and ended the third quarter of 2010 on the same level as twelve months prior. The strongest industries in terms of stock performance over the past twelve months were retail and consumer products as well as industrial goods and services, as both sectors rose by approximately 20%. Healthcare and financial services companies underperformed the overall stock market over this period.

Transactions by industry and size

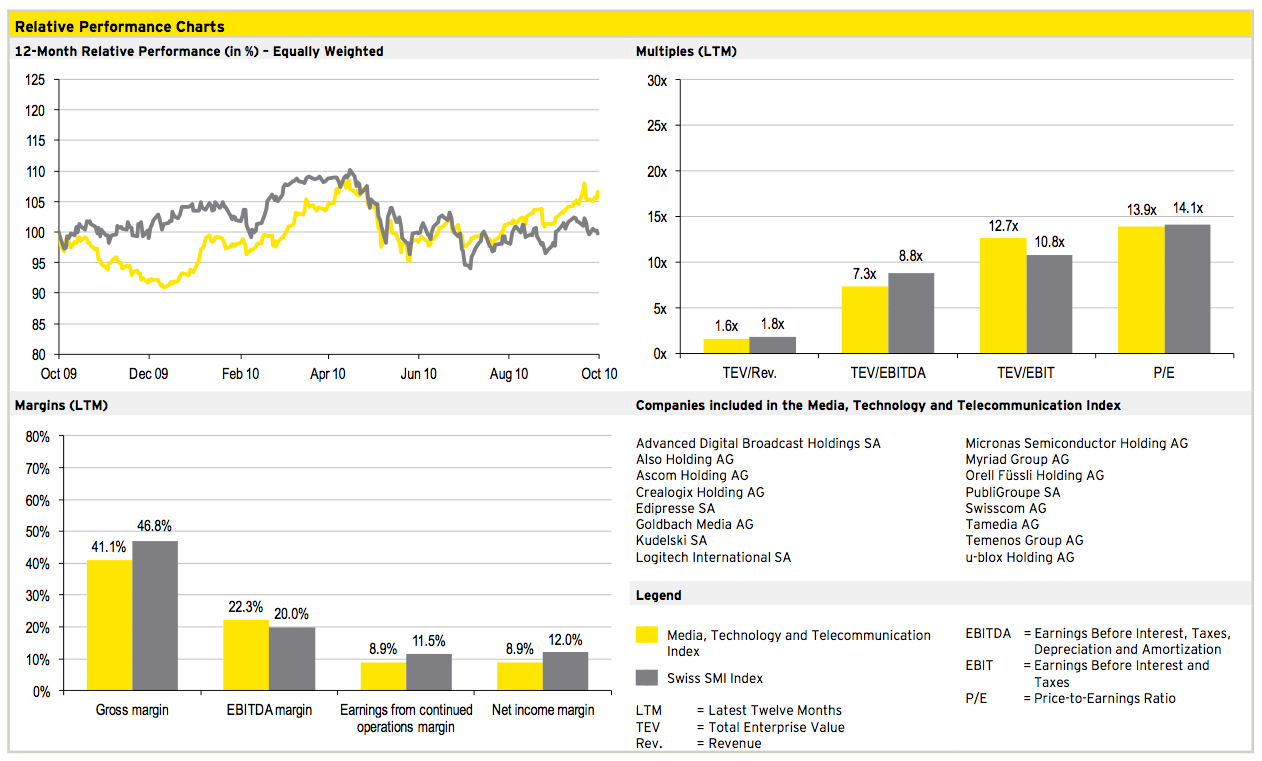

The retail and consumer products sector has not only achieved the strongest stock performance over the past twelve months, it was also the most active industry in terms of transactions during the third quarter of 2010, accounting for 23% of all Swiss M&A transactions. As in the previous quarter, 18% of all Q3 2010 transactions were in the media, technology and telecommunication industry, thus remaining one of the most active sectors.

As for the retail and consumer products sector, Aryzta, a Swiss-based specialty bakery company, has continued to expand its business through strategic acquisitions in the third quarter of 2010. The company agreed to acquire the remaining 50% stake in Maidstone Bakeries from Tim Hortons Inc. for approximately USD 455m. Aryzta had previously already announced the acquisitions of Fresh Start Bakeries Inc. and Great Kitchen Inc. for USD 1.1bn in June 2010.

The media, technology and telecommunication sector accounted for another large transaction besides the sale of Sunrise. Schaffhausen-based Tyco Electronics Ltd. acquired ADC Telecommunications Inc. for USD 1’908m, positioning Tyco Electronics‘ Network Solutions segment as a leading global provider of broadband connectivity products to carrier and enterprise networks around the world.

The third quarter of 2010 showed a significant improvement in the number of large M&A transactions valued above USD 250m. Nine M&A deals were valued above USD 250m during the most recent quarter compared to only four large transactions in the previous quarter. The number of medium-sized deals remained stable compared to Q2 2010.

Outlook 2010/2011

The Swiss State Secretariat for Economic Affairs (SECO) raised its GDP growth outlook for 2010 from 1.8% to 2.7% in September 2010. However, SECO reduced its expectations for 2011, lowering the projected GDP growth to 1.2%. SECO expects that the currently strong Swiss Franc will have a negative impact on the economy’s growth as the strong local currency will hurt exporters. As the economy is rather expected to weaken than gaining momentum, Swiss M&A activity is anticipated to improve only moderately.

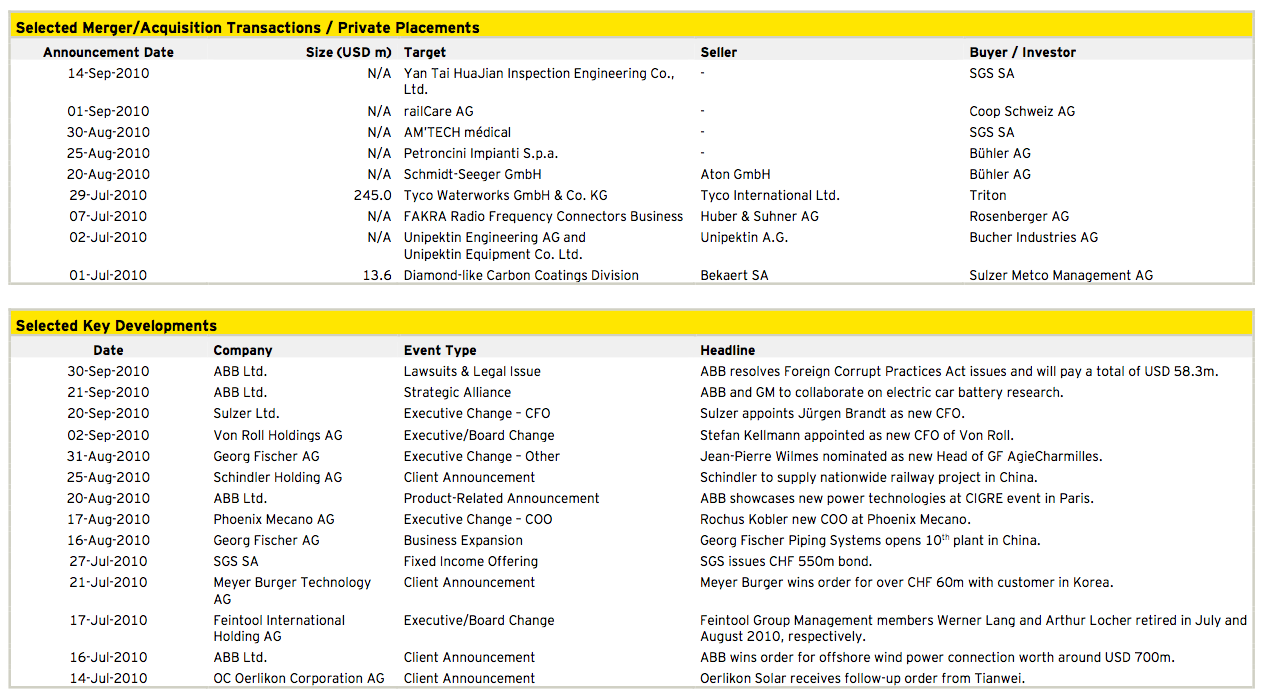

The availability of debt has improved considerably in recent months. Banks are increasingly ready to finance large acquisitions. This summer, the Australian mining firm BHP Billiton Limited bid for the Canadian Potash Corporation. BHP was able to secure debt financing from several banks for a total value of approximately USD 45bn within days. As debt financing becomes easier, more companies are anticipated to consider acquisitions. However, Swiss firms are generally more disciplined buyers focusing on strong balance sheets. In June 2010, ABB Ltd. Offered to buy Chloride Group PLC, but Emerson Electric Co. outbid ABB by approximately 15%. Instead of initiating a ‘bidding war’, ABB withdrew from the proposed transaction.

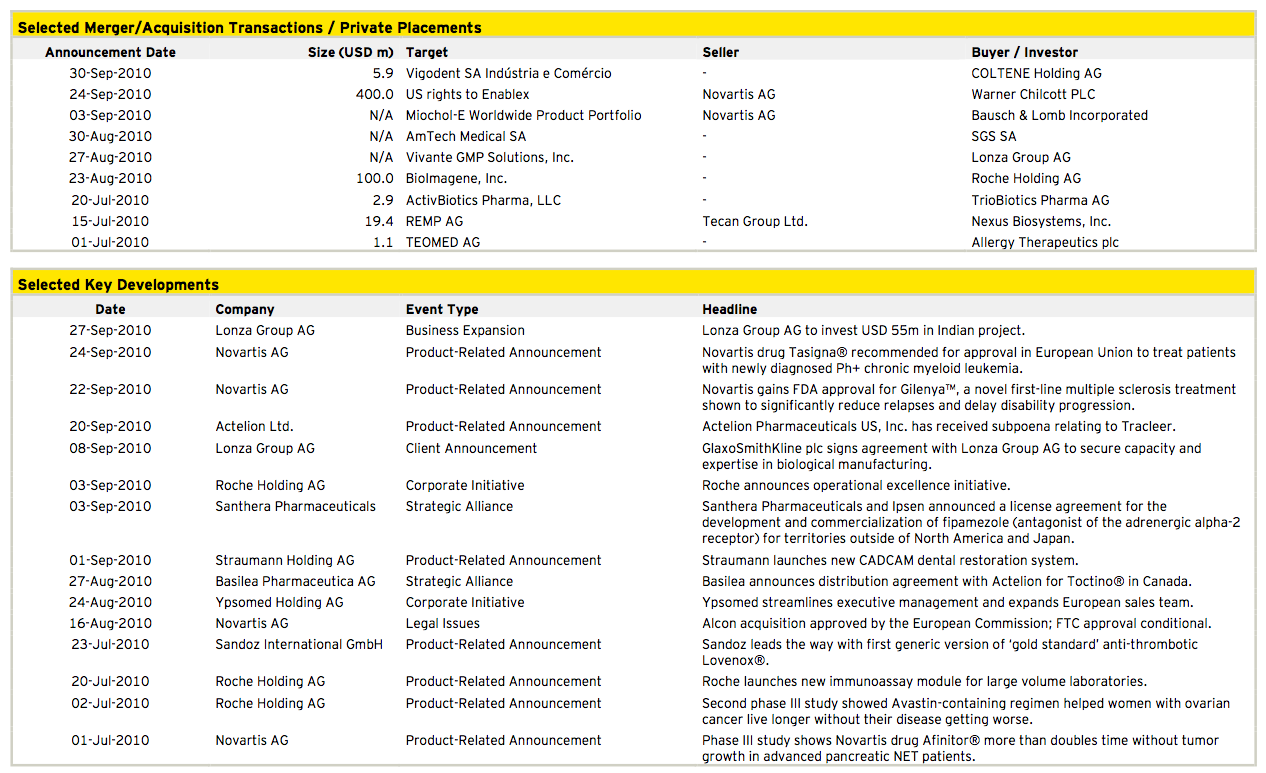

In terms of industry, the retail and consumer goods as well as technology sector are expected to remain among the most active areas for M&A transactions as companies are consolidating and looking for attractive returns. M&A activity in the healthcare industry is also expected to increase as valuation multiples have decreased throughout 2010. In addition, healthcare firms are looking to improve their product pipeline through acquisitions.

Apart from the moderate economic outlook, the current M&A environment is quite favorable. Company valuations are, from a historical perspective, still attractive. Swiss firms tend to have strong balance sheets and cash reserves available for investments. Companies are also looking for more profitable endeavors through external growth rather than generating interest on cash reserves.

Deal of the quarter

Deal Summary

In this edition, our deal of the quarter features the acquisition of Sunrise Communications AG by CVC Capital Partners Ltd. from TDC A/S for CHF 3.3bn. The approval of Swiss antitrust and relevant regulatory authorities was obtained in mid October 2010. The acquisition is expected to be financed by approximately one-third in cash and two-thirds in borrowed funds.

Sunrise has approximately 2.9 million customers which use its services in the areas of mobile telephony, fixed network and the internet.

Deal Rationale

► With the divestment of Sunrise, TDC is further focusing on the Nordic communications market.

► Under its new ownership, Sunrise is expected to continue its current challenger strategy while maintaining its high level of investment in infrastructure and distribution.

► With CVC Capital Partners, Sunrise is expected to be backed by a strong financial partner which supports the company’s plan to drive investment in both network and customer service.

► CVC Capital Partners sees an IPO of Sunrise as a potential future strategic option.

Industry overview

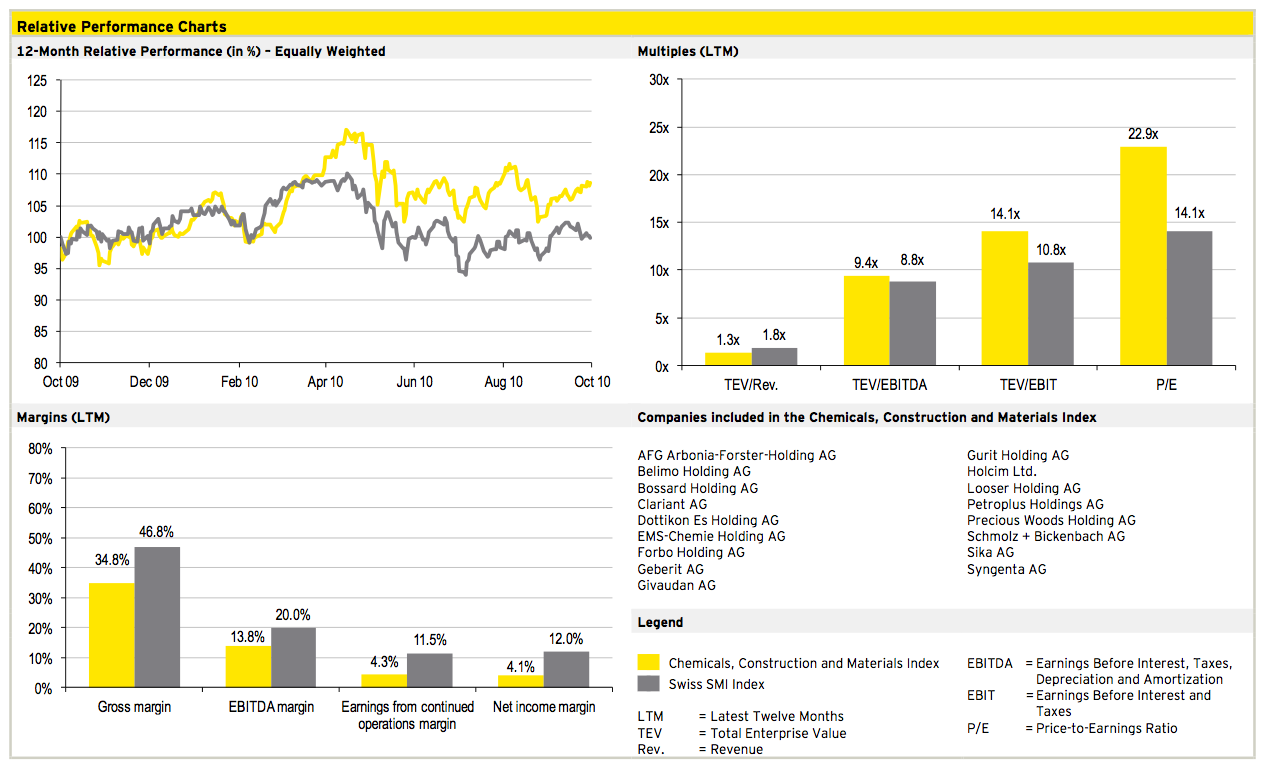

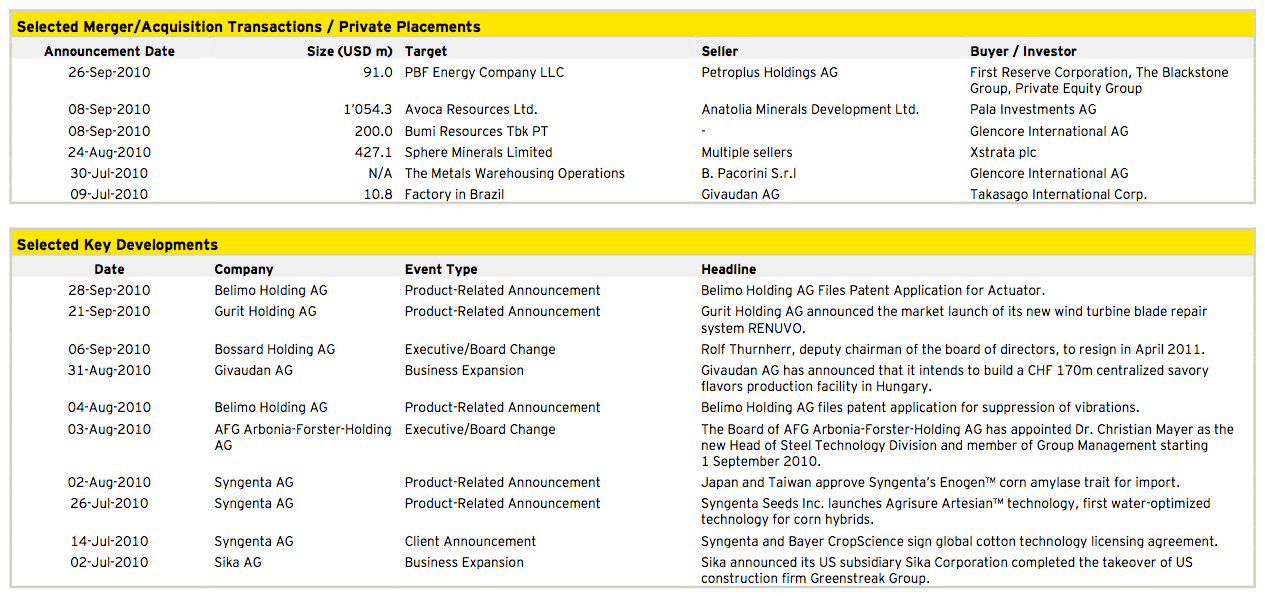

Chemicals, Construction and Materials

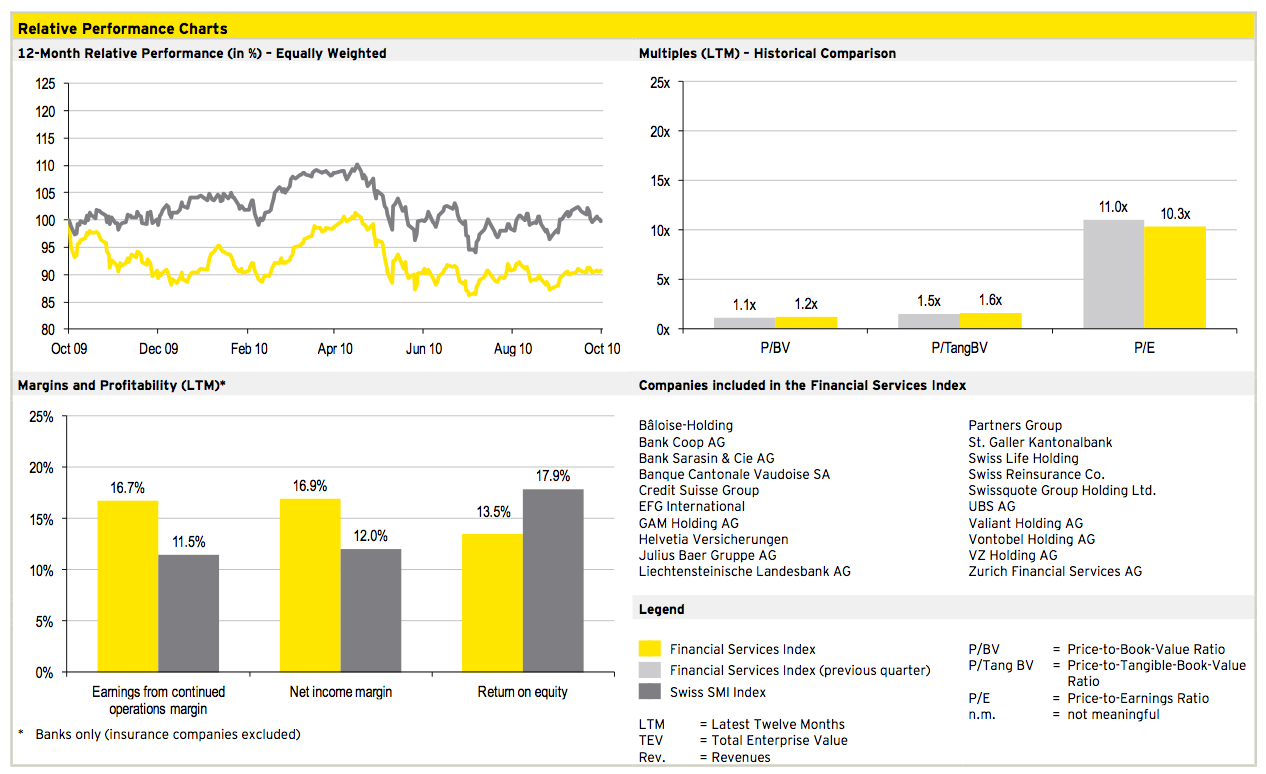

Financial Services

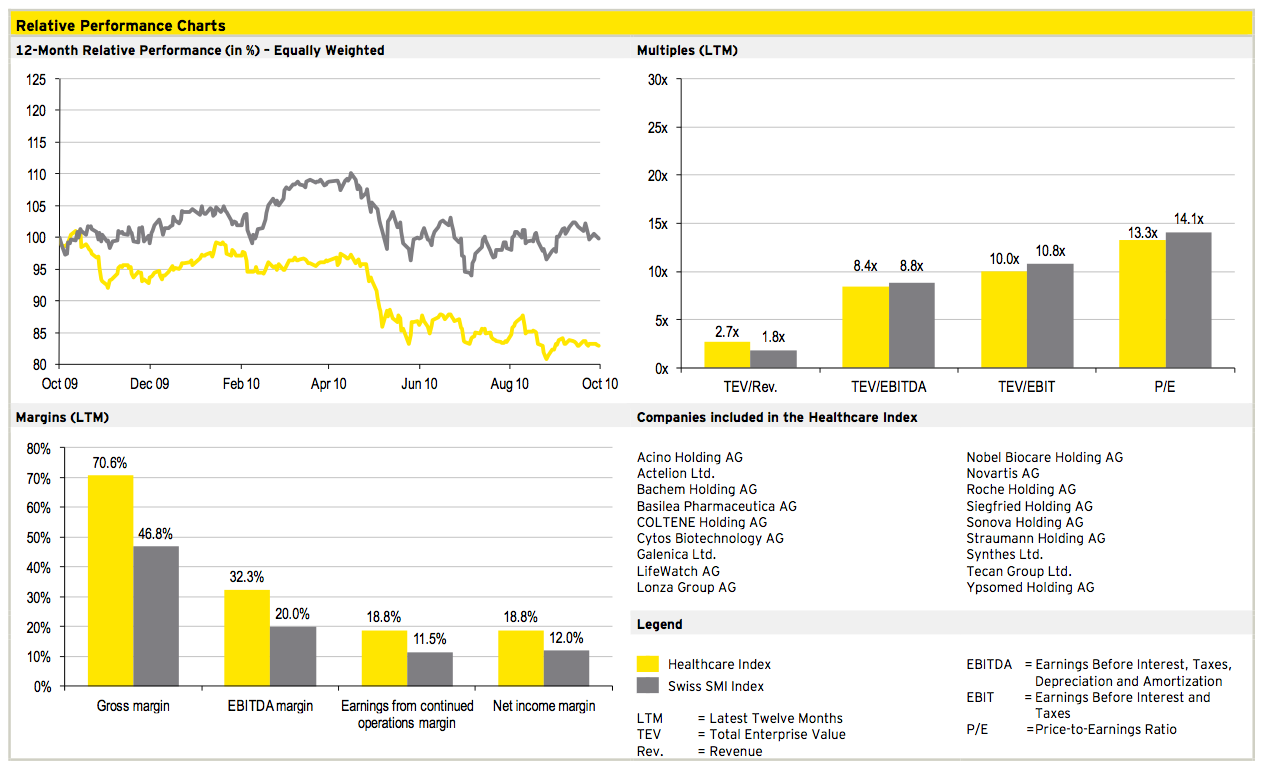

Healthcare

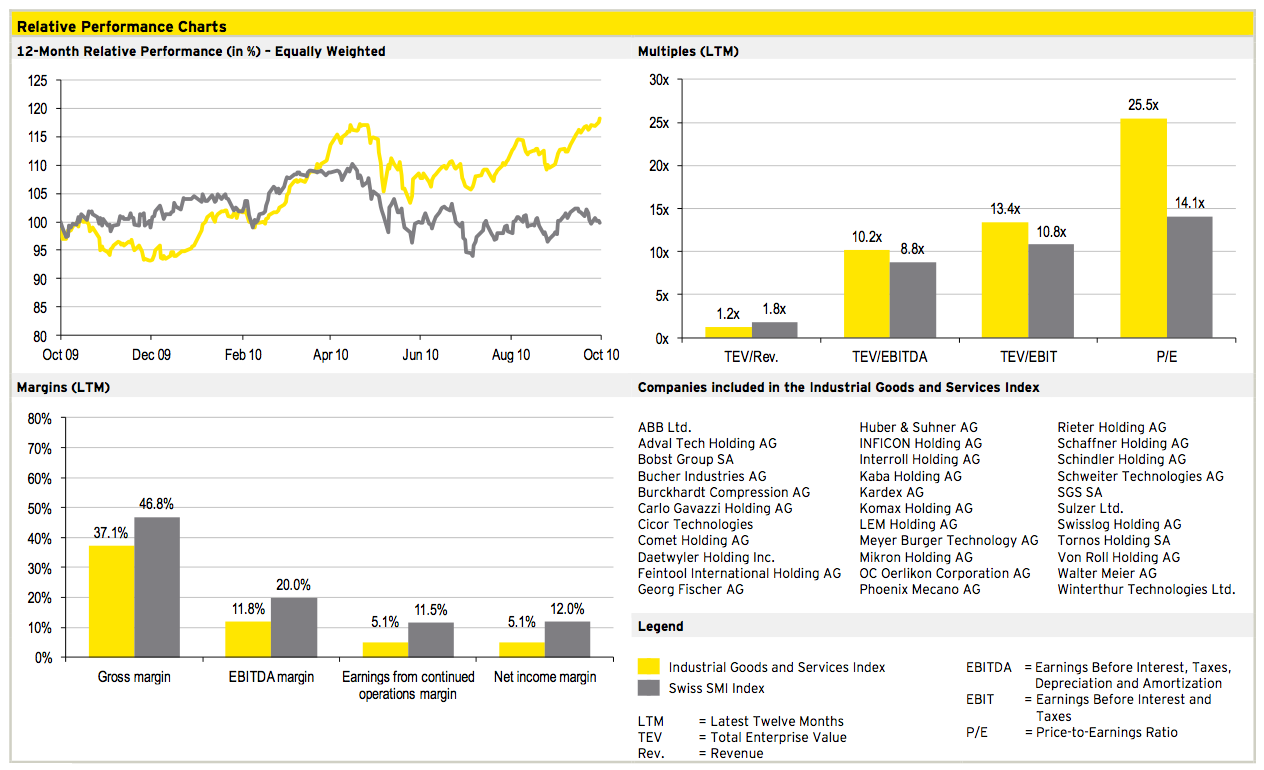

Industrial Goods and Services

Media, Technology and Telecommunications

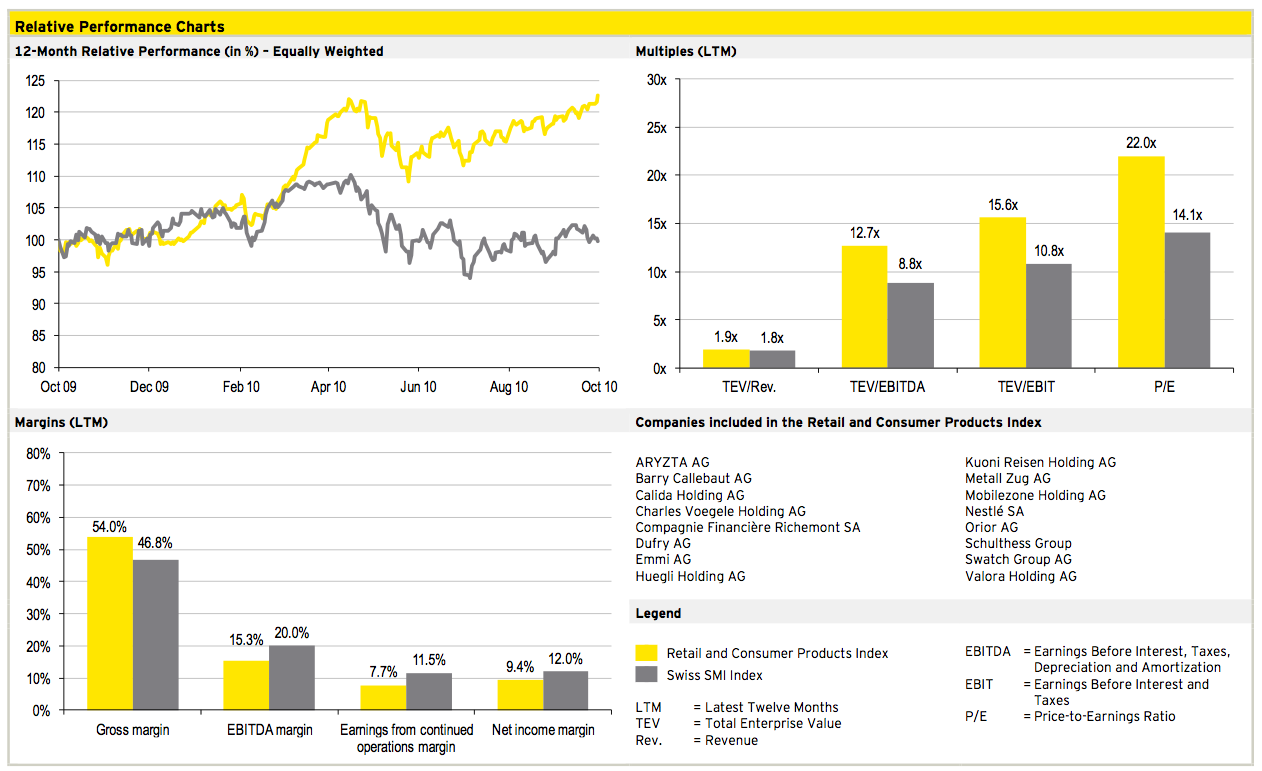

Retail and Consumer Products