By Pip McCrostie – Ernst & Young

Our 12th Global Capital Confidence Barometer finds the global M&A market maintaining the positive momentum that developed during 2014. For the first time in five years, more than half our respondents are planning acquisitions in the next 12 months, as deal pipelines continue to expand.

Executives express increasing optimism in the global economy, with much broader consistency across geographies than in 2014. This economic optimism, combined with steady confidence in corporate earnings and other leading market indicators, is fostering an environment where companies are preparing bolder moves, including M&A, to generate future value.

Our survey reveals three key reasons for the sharp increase in dealmaking intentions. First is the arrival of new entrants — both start-ups and companies returning to the market after staying on the sidelines for several years. Second, divergent economic conditions are accelerating cross-border M&A, as existing momentum in many developed markets is further fueled by falling oil prices and currency fluctuation. And third, disruptive innovation is driving dealmaking at every level of the enterprise.

Of course, challenges remain prominent on the boardroom agenda. Greater volatility in commodity and currency markets, geographic divergence in economic conditions and monetary policies, and lingering geopolitical concerns all present complexity. As well, rapid technological change is creating new risks such as cybersecurity, which has emerged as a core business issue that must be managed as part of the dealmaking process.

Notwithstanding these risks, the overall view in this Barometer is of a global M&A market on an upswing after years of crisis. Companies are learning to create opportunity and drive growth amid a more competitive economicand geopolitical landscape. After a half-decade of stagnation, we are seeing the bold beginnings of a new kind of M&A market — one marked by innovation, complexity and disruptive change.

Key M&A findings

56% of companies expect to pursue acquisitions in the next 12 months

73% of M&A activity will be innovative investment

50% increase in intent to pursue upper- middle-market deals

47% of companies intend to complete more deals than in the prior year

45% are proactively guarding against cyber breaches in their M&A process

Macroeconomic environment

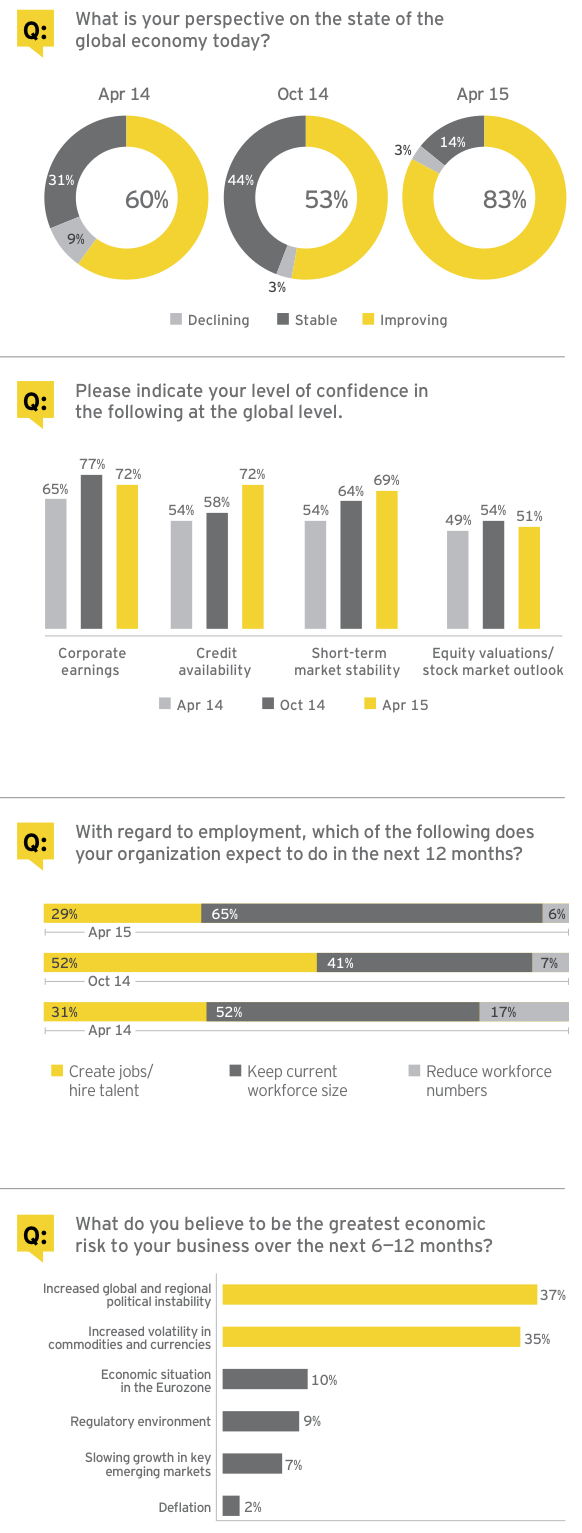

An overwhelmingly positive outlook for the global economy, and a continued robust outlook for corporate earnings and other leading market indicators, including credit availability, should combine to support a healthy M&A environment over the next 12 months.

83% of executives view the global economy as improving

• Executives see sustained momentum in broader global economy

The vast majority of executives now see the global economy as improving, up strongly from a year ago. Our survey shows broad-based confidence across all geographies. In 2014, only the US, UK and China were fueling economic optimism. In 2015, multiple engines are powering the global economy: a US economy moving from perceivable to unequivocal growth, China moderating but still growing, and a Eurozone economy moving past austerity in its stronger economies and managing risk elsewhere. While significant downside risks remain, executives are increasingly focused on capturing the potential upsides of global economic growth.

• Corporate earnings outlook and other leading market indicators remain positive

Our survey reflects some reduction in confidence in corporate earnings growth from last year but it still remains high. This sentiment may reflect a corporate environment entering a new phase. Many companies are experiencing diminishing returns from shorter-term cost-cutting and efficiency programs instigated at the outset of the global financial crisis. These companies may experience a lag in the realization of cost savings from longer-term structural transformation programs currently underway. So a short-term tempering of earnings growth is to be expected. In addition, the credit landscape is complicated but favorable overall. While US quantitative easing (QE) ends, the introduction of QE in Europe and its continuation in Japan should support a healthy availability of credit worldwide.

• Battle for talent heats up as companies look to recruit and retain

A new phase of the global employment picture appears to be at hand. Companies are not only growing their workforce but are also under pressure to retain the best talent. Nearly two-thirds of executives say they are maintaining their workforce size. Meanwhile, the number expecting to grow their workforce is down from six months earlier but remains nearly parallel with a year ago. The percentage of respondents anticipating workforce reduction is the lowest since the first Barometer in 2009. Strong US and UK employment growth and an improving Eurozone situation are compelling companies to keep one eye on acquiring talent as they simultaneously defend their workforce from competitive poaching.

• Geopolitical concerns persist, commodity and currency volatility rises

Unsurprisingly, when companies consider the major risks to their business, the largest number view the ongoing geopolitical issues — from Eastern Europe to the Middle East — as the greatest concern. What is perhaps surprising, and might have been unforeseen as recently as six months ago, is how the sharp fall in commodity prices and increasing volatility in currencies have grown as major concerns. These issues rank a strong second place to geopolitics among business risks. Going forward, divergent monetary policies may increase currency volatility, which, together with geopolitical concerns, hinders the ability of executives to plan ahead.

Corporate strategy

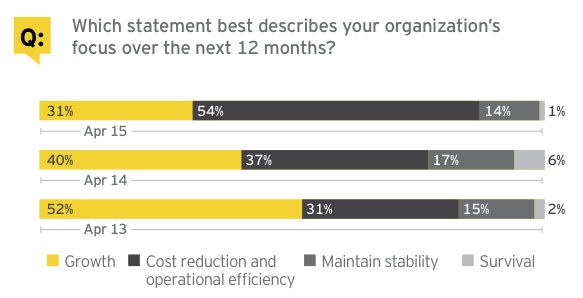

Cost reduction continues as a perennial focus, but in a fast-changing world, companies are pursuing innovative growth strategies to improve their market positioning.

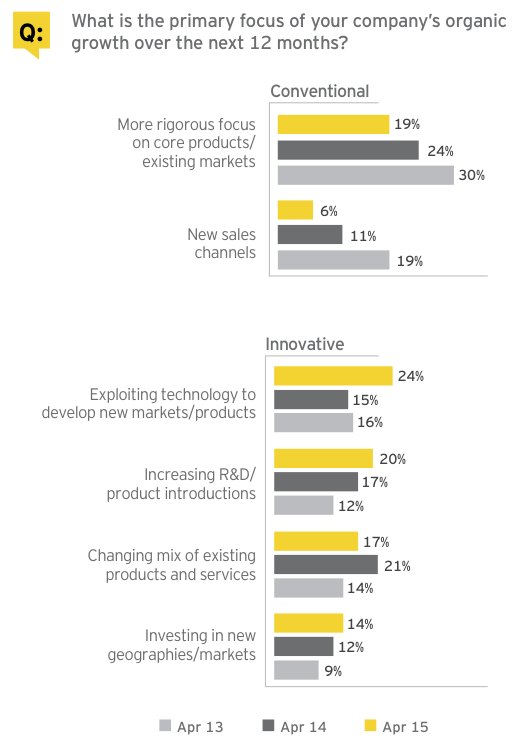

76% of companies are focused on innovative organic growth strategies

• Intense cost scrutiny now an everyday feature of corporate strategy

Cost discipline is now embedded in corporate DNA — even as the global economy moves past crisis mode. A low-growth, low-inflation environment compels executives to keep a tight rein on cost structure, as increased expenses cannot easily be passed on to customers. This cost focus is exacerbated in the short term by greater currency volatility and fluctuations in commodity pricing.

• Innovative organic strategies targeted to boost market footprint

Given the overwhelming view that the global economy is expected to improve — coupled with the disruptive forces affecting all industries — executives are now more likely to pursue innovative growth strategies. These strategies include entering new markets, considering new services, increasing R&D and exploiting technological change.

To be sure, focus on core operations remains a priority. However, the definition of “core” continues to evolve, as technological change and disruptive competitors continue to redefine the essence of a company’s business. Companies must protect and grow this ever-evolving core while accessing new opportunities, as they seek to expand their market footprint and protect their competitive position.

The definition of “core” operations continues to evolve. Technological change and disruptive competitors are redefining the essence of a company’s business.

Global megatrends: Fundamental global changes reshaping corporate strategies

Q: Which of the following will impact your core business and your acquisition strategy most in the next 12 months?

Global marketplace — Economic power shifts east and south, driving patterns of trade and investment

31% Core business

40% Acquisition strategy

Faster growth rates and favorable demographics in key emerging markets are expected to feature prominently over the next decade, as the gulf between developed and emerging countries continues to shrink and a new tier of emerging nations is driven by its own nascent middle classes. Increasingly, innovation is taking place in emerging markets, with Asia as a major hub. At the same time, the battle for talent will be increasingly fierce, driving greater workforce diversity to secure competitive advantage.

The world’s economies are expected to remain highly interdependent — via trade, investment and financial systems — driving the need for stronger policy coordination among nations and resilient supply chains for companies operating in this environment. At the same time, domestic interests will continue to compete with the forces of global integration. These trends will affect companies’ core business and acquisition strategies regardless of location, but executives nonetheless must consider not only what they do, but where they operate.

Entrepreneurship rising — Growth in global entrepreneur class will require more supportive ecosystems

38% Core business

11% Acquisition strategy

Entrepreneurs are the lifeblood of economic growth worldwide, both as employers and as producers of innovative products and services. They drive upstream and downstream value-chain activities. The growth and prosperity of all economies — developed and emerging — rely on robust entrepreneurial activity.

While some entrepreneurial activity is still motivated by necessity, “high-impact” entrepreneurship, once largely confined to mature markets, now drives emerging market expansion. Indeed, many emerging-market entrepreneurs are building scalable enterprises that capitalize on local needs and serve as business role models.

The rise of this entrepreneurial spirit is accelerating the introduction of new entrants to sectors that rely on intellectual property, such as consumer products, life sciences and technology. This means both challenges for existing players and opportunities as innovative start-ups attract M&A activity.

Digital future — Technology is disrupting all areas of enterprise, driving opportunities and challenges

21% Core business

12% Acquisition strategy

Fueled by the convergence of social, mobile, cloud and big data, and the growing demand for anytime, anywhere access, technology is disrupting all areas of the enterprise — across industries and geographies.

The evolution of the digital enterprise also presents significant challenges: new competition, changing customer engagement and business models, unprecedented transparency, privacy concerns and cybersecurity threats. Companies that seize the opportunities offered by digital advances stand to gain; those that cannot may lose everything. Relationships between companies are becoming more fluid, as partners in one channel become competitors in another.

In sum, all of these technology-driven changes make long-term corporate strategy and acquisition plans far more complex and yet require expedient decision-making.

Boardroom agenda: Operational efficiencies top boardrooms’ agendas

While costs and efficiencies are always a primary boardroom topic, the recent fluctuations of currencies and commodities have further elevated the prominence of cost reduction in the short term. Cost reduction is also at the heart of the shareholder activist agenda. In this Barometer, activist influence has not been elevated relative to other issues, because it was already at a very high level. Acquisitions are a continued focus of the boardroom agenda, as companies keep their eye on value-creating transactions.

Comparing responses on the boardroom agenda (above) with our survey results (below) on the Capital Agenda — EY’s framework for companies’ strategic decisions — we see a strong correlation. Optimization is the overwhelming capital priority, topping the agenda for well over half of executives. This reinforces that even as the global economic outlook improves, companies see a rigorously efficient portfolio as essential to remain competitive and protect corporate positions.

M&A outlook

The evolution of the M&A market in 2014 — from an emphasis on megadeals to late-breaking growth in the middle market — boosted the deal market to new, post-crisis highs. The market in 2015 has so far continued this trend, with companies continuing to transact, including start-ups and companies previously on the sidelines entering the fray.

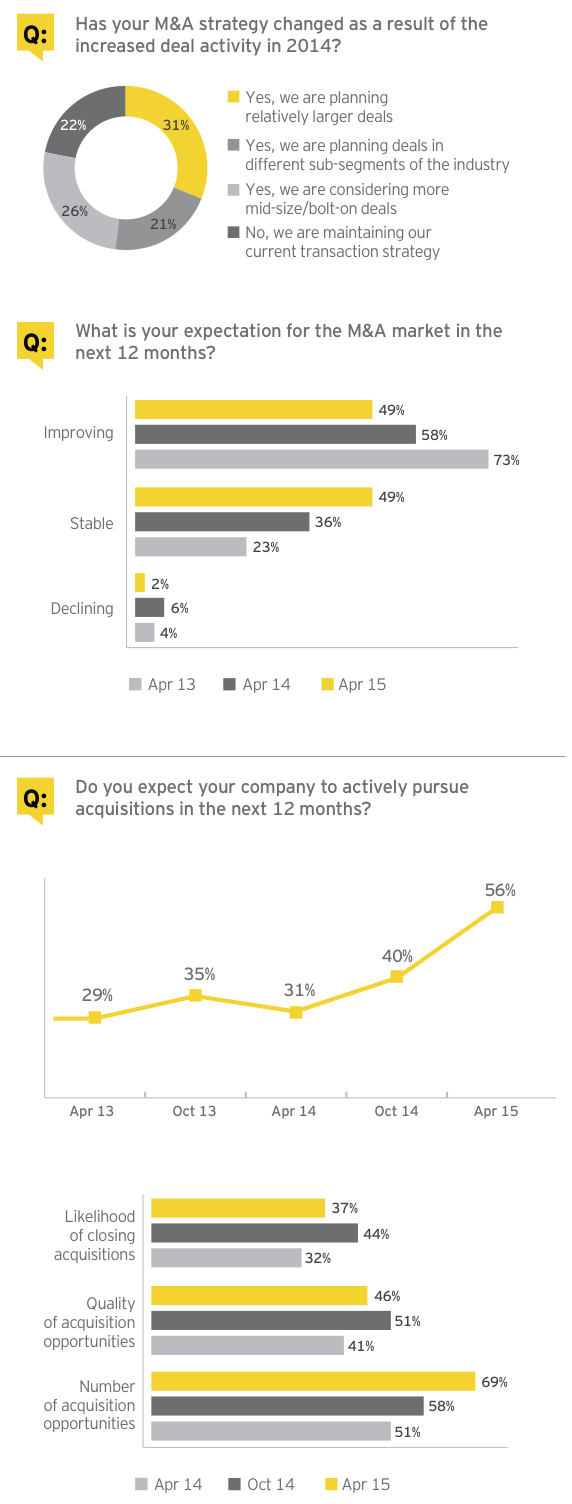

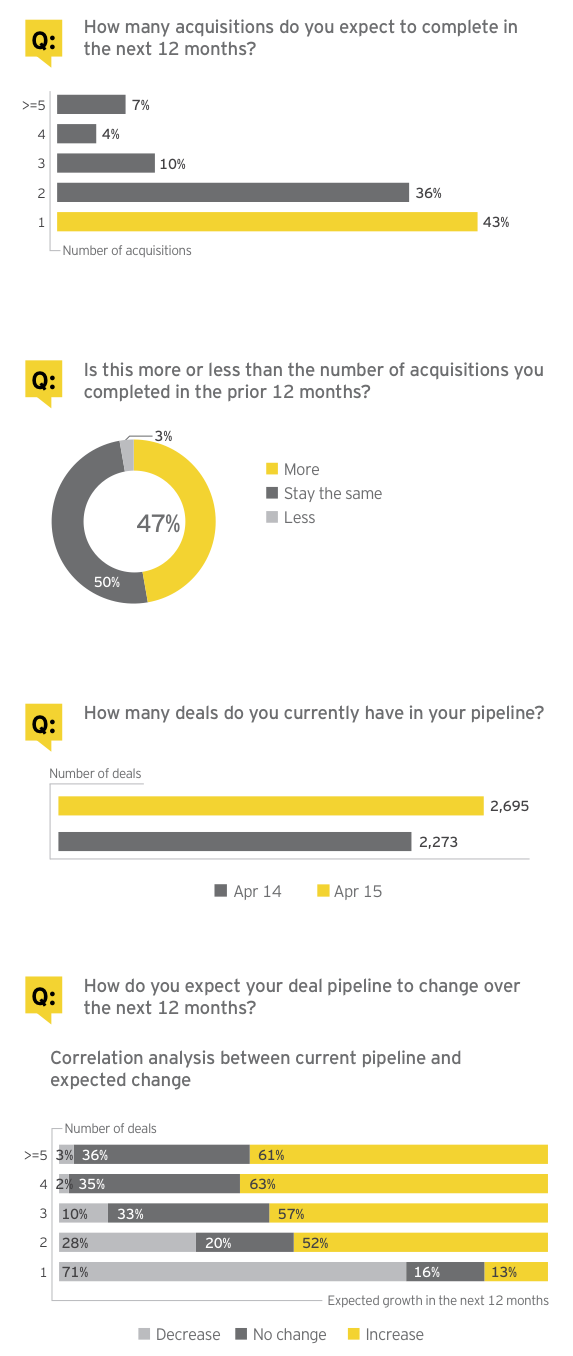

56% of companies expect to pursue acquisitions in the next 12 months

After 2014 gains, M&A intentions step up as market growth stabilizes

Last year witnessed the strongest increase in mergers and acquisitions since the global financial crisis. Growing confidence in the global economy will further support M&A in 2015. More than three-quarters of executives plan to boost their dealmaking in some fashion over the next 12 months. Moreover, while nearly one-third of executives are planning bigger deals, bolt-on and complementary deal intentions are also up.

With the market already at elevated levels, it is not surprising that a greater percentage of our respondents expect M&A activity to remain stable over the next 12 months — this response is now even with those expecting market improvement. Given the strength of deal intentions, greater stability should provide the foundation for sustainable growth in the M&A markets.

More than half of companies intend to acquire

For the first time since 2010, more than half of our respondents intend to make an acquisition in the next 12 months. With economic sentiment broadly supporting M&A, our survey reveals a number of reasons for this sharp increase in dealmaking intentions.

New entrants — both start-ups and companies returning to the market — are boosting deal volumes. Also, cross-border M&A has been accelerated by divergent global economic conditions. For example, QE will likely boost evaluation of companies in the Eurozone, even as a decline in the value of the euro and falling oil prices are making Eurozone-based assets far more attractive. In addition, disruptive innovation — such as increasing convergence and blurring of defined sector lines — is driving dealmaking at every level of the enterprise. Supply chains, channels to market and back-office infrastructure are all affected by innovation, and M&A is often the best route for maintaining or gaining competitive advantage.

Two other ingredients necessary for positive M&A sentiment are the improving quality and quantity of potential targets. The quantity or inventory of assets on the market is strong, supported by private equity finally divesting long-held assets and increased corporate carve-out activity.

The quality of targets is also relatively strong, driven by an improving business environment and ongoing cost-management and margin-improvement programs.

New market entrants accelerate pipeline growth

• Companies expect to complete more acquisitions

Almost half of executives expect to close more deals in the next 12 months than they did in the prior year. Most also say that their total number of deals will be relatively small, one or two acquisitions. Many of these dealmakers are likely new entrants or those returning after a break, based on analysis of forward-looking expectations and historic deal completions. These companies will help drive 2015’s increased deal activity, just as they did in 2014.

• M&A pipelines remain healthy as the pool of dealmakers expands

Deal pipelines are a key indicator of the state of the M&A market, offering context on how companies are thinking about opportunities and preparing for growth. In total, our respondents are considering some 2,695 deals — a notable 19% increase over the prior 12 months, signaling the fundamental health of the deal markets.

• Growth in larger pipelines is poised to resume

Companies with the largest pipelines today are the ones with the strongest intention to increase pipeline size in the next 12 months. As companies lean toward more innovative deals that shift the scope of their operations into adjacent or complementary businesses, they will naturally consider a greater number of potential targets.

As companies lean toward innovative deals that shift their scope into adjacent or complementary businesses, they naturally consider a greater number of targets.

Valuations support continued dealmaking

• Potential upside pressures on asset prices, but M&A market expected to persevere

Record-high equity markets, strengthening M&A markets and an improving global economy have all increased competition for assets. Given this environment, it is unsurprising that most executives see the valuation gap widening. However, a clear majority see that gap as only somewhat higher — a sign that the deal markets are healthy but not overheated. Most important, overwhelming majorities expect both the valuation gap and the price of assets to remain stable in the next 12 months, creating conditions conducive to dealmaking.

One region where valuations will likely increase is the Eurozone, due to its new quantitative easing program. However, while some upward pressure on valuations is expected there, other factors, such as exchange rates and lower oil prices, should mitigate any significant negative effect on M&A.

Overwhelming majorities expect both the valuation gap and the price of assets to remain stable in the next 12 months, creating conditions conducive for dealmaking.

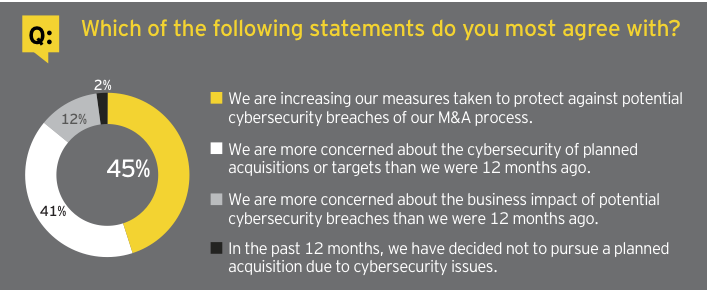

Cybersecurity: Cyber attacks a growing risk to rebounding M&A market

Transactions are a prime target for cyber attacks. The M&A market rebound, coupled with heavy reliance on technology and digital assets in today’s transaction environment, is a recipe for increased cyber attack risk. More than ever, a strong process for mitigating cyber threats is imperative for all companies. Cyber attacks are a fundamental business risk, not simply a concern for the IT department.

Implications of a cyber attack

Potential business risks of a cyber attack include theft of R&D and intellectual property, financial fraud and reputational damage. The disruption caused by an attack may extend beyond the company itself to the industry and the broader market.

In the case of M&A specifically, companies’ systems can be hacked or compromised during the deal process, with the intent to gain insider information. One obvious risk is manipulation of the stock price and the deal process. A less obvious but equally significant risk is the potential to gain strategic information that could be used to disrupt the company’s core business and competitive position.

Identifying the risk is the key step in managing it

The M&A process centralizes an organization’s strategy and information on all of its functions in one repository. This presents a unique cyber risk situation that must be managed.

One of the most important ways to manage cyber risk during the M&A process is to proactively determine who may be targeting the organization — and which information they might want to steal. While identifying these threats, companies should consider not only potential attackers from outside the organization but also entities with authorized access, such as supply- and distribution-chain vendors as well as other business partners. Even the target company in an M&A transaction could pose a threat, because any weakness in its security program could be exploited. Once these risks are identified, preventive steps can be taken to alleviate them.

Dealmakers pointed toward innovation

• Disruptive forces driving deals

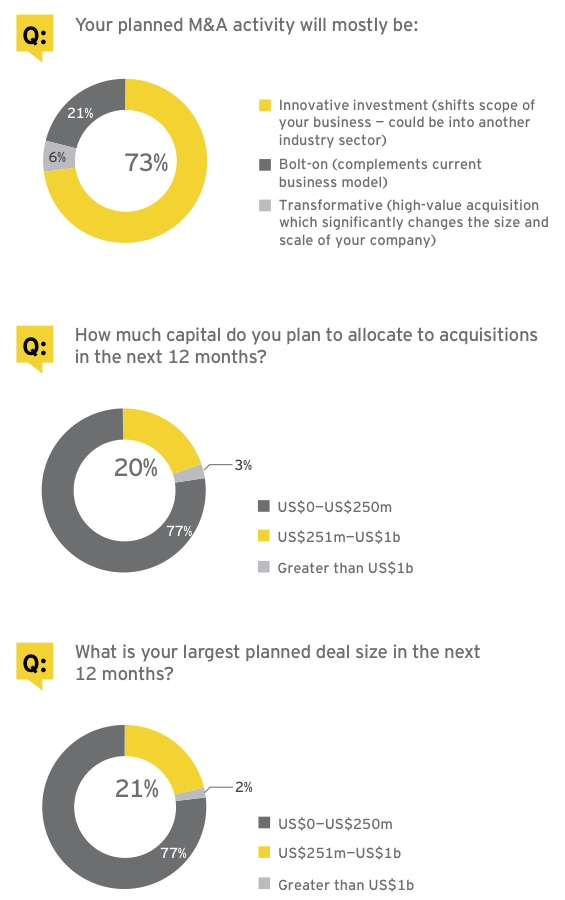

Innovation, disruptive forces, blurring of their own clear sector definitions and global megatrends are all combining to fuel M&A. In response, companies are making bolder moves to shift their business scope and maintain competitive advantage.

Accordingly, nearly three-quarters of executives who are considering deals are eyeing these innovative investments rather than bolt-on or transformative transactions. More and more, companies are learning to anticipate future challenges to their business models and using acquisitions as a vehicle to accelerate their response.

• Upper-middle-market M&A to accelerate

Looking at expected deal size, the smaller middle-market deals — those under US$250m in size — continue to dominate executives’ plans. Contributing to the continued strength in this category is a large number of smaller, more innovative acquirers entering the market. However, since our last Barometer, the most significant growth has been in upper-middle-market deals, those above US$250m and under US$1b in size. This category has increased by 50%.

While blockbuster megadeals — the dominant category in 2013 and early 2014 — have not exited the market entirely, our respondents confirm that deals over US$1b in size are now only a small focus of their activity.

Deals under US$250m continue to dominate executives’ plans. But the most significant growth since our last Barometer has been in upper-middle-market deals — those between US$250m and US$1b.

Sector outlook: Strong deal sentiment across many sectors

Many established companies are making deals involving “moonshots” — technologies that may drive dramatic change and commensurate returns, such as the Internet of Things and virtual reality.

Search for intellectual property and strong brands driving top industry sectors, which are transacting vigorously

Percentage reflects those who intend to actively pursue acquisitions in the next 12 months.

67% Technology

Increasing competition for assets related to smart mobility, cloud computing, social networking, big data analytics and accelerated adaptation are powering tech M&A. Furthermore, some established companies are making deals involving “moonshots” — technologies that may drive dramatic change and commensurate returns, such as the Internet of Things and augmented or virtual reality.

58% Consumer products and retail

Consumer products companies have sharpened their focus on developed-market businesses. In the absence of ample growth avenues, companies are targeting operational efficiency by making strategic divestments. Portfolio optimization is emerging as a critical theme, driving strategic transactions amid increasing investor pressure on companies to deliver shareholder value. Large consumer product players are optimizing their brand portfolios and market exposure by disposing of non-core and lower-growth businesses and rechanneling investments into acquiring or expanding in faster-growth or higher-margin businesses.

49% Financial services

Compressed interest-rate margins and regulatory capital pressure in the banking and capital markets sector may result in further industry consolidation and asset sales. We also expect to see continued interest in the specialty-finance and fintech segments.

Insurance companies are looking to enhance the overall structure of their operations and balance sheets in anticipation of Solvency II. Meanwhile, reinsurers are looking to grow and enhance investor value. The current environment makes acquisitions an attractive option.

International presence has become an increasingly important priority for wealth and asset managers. With global markets in different economic cycles, investors expect asset managers to access investment returns wherever the opportunity exists.

59% Automotive

Renewed optimism in the automotive sector — brought about by increasing sales in both developed and emerging markets and a sector-wide drive to decrease costs and improve efficiencies — is motivating increased M&A. A significant number of deals focus on acquiring emergent technologies, such as driverless cars and advanced materials.

53% Diversified industrials

As growth in industrials is typically tied to GDP, M&A is necessary to achieve above-market returns. In particular, the decline in the euro will likely boost the attractiveness of high-quality, IP-rich Northern European assets, especially Mittelstand companies in Germany, Switzerland and Austria, with demand coming from the US, China and Japan.

Given the low-growth environment, portfolio management will continue to be a large focus, especially for those affected by recent volatility in energy prices. Cost reduction remains an imperative for these companies, because of pressure on topline growth.

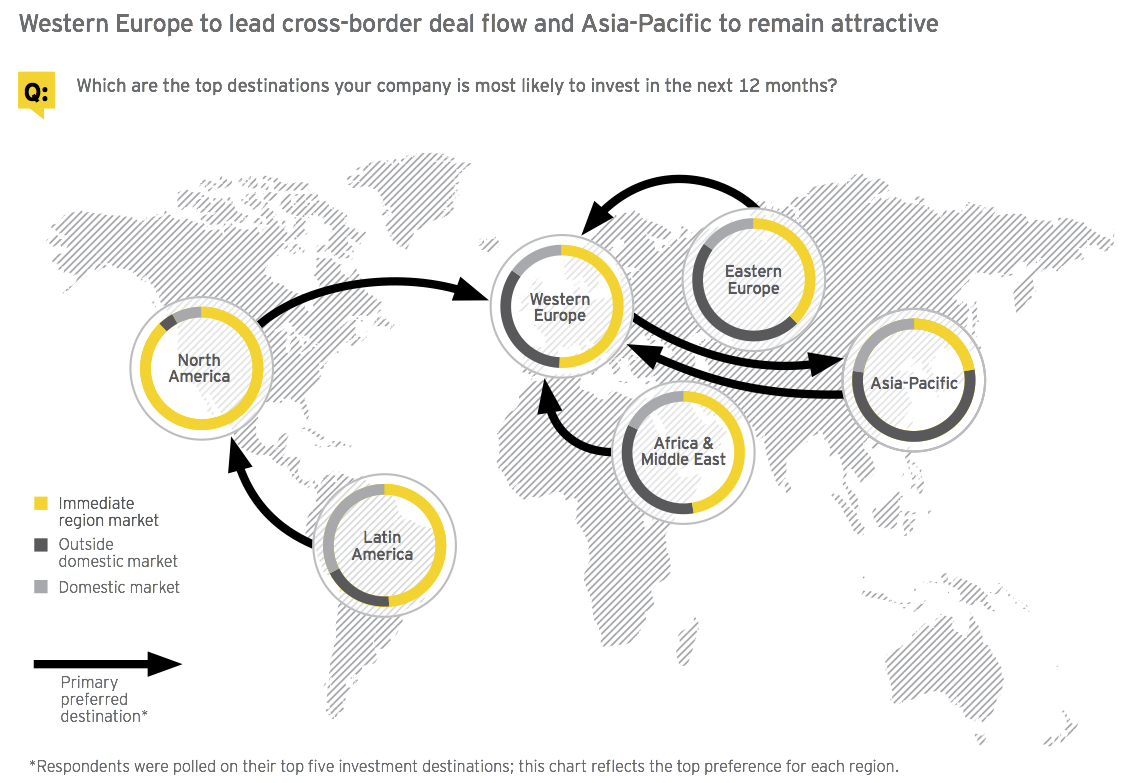

Dealmakers looking across borders, but relatively close to home

Executives report rather low expectations for their own domestic M&A. At just 16% of planned deals, this response is well below the historic average. More than four-fifths of our respondents are seeking deals outside of their home country.

A major driver of this search for cross-border opportunities is companies exploiting divergent economic performance between countries and regions. Where a company operates is now as important as the segments or sectors in which

it operates. Enterprises that undertake a robust portfolio review often move toward geographies that fill gaps or are ripe for disruption.

The largest category of executives — more than half — are focusing their M&A strategies on cross-border transactions in their immediate region, driven by the ease of acquiring in common economic trading areas. This intention to acquire close to home is also boosted by the familiarity of investing in adjacent countries, which eases the path to cross-border M&A. However, a very sizable minority — almost one-third — are planning to acquire further afield, which highlights the increasing interconnectedness within the global economy.

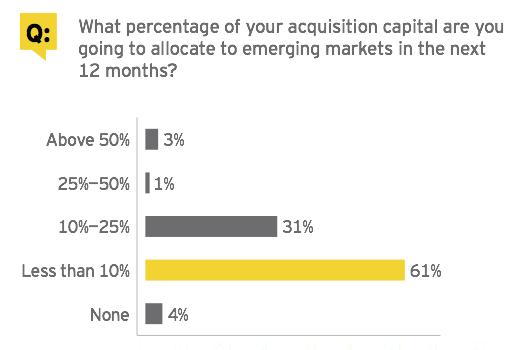

Acquisition capital targeted primarily to developed and top-tier emerging markets

Companies are planning to invest the majority of their acquisition capital in developed markets, which will provide more near-term growth. Emerging markets remain important for the long term, but inbound acquisition activity into these markets will likely remain unchanged for the next 12 months. The potential upturn in major developed markets, particularly the Eurozone, is also affecting M&A strategy.

The popularity of Western Europe as a destination for cross-border M&A should persist as the European Central Bank begins its QE program, which aims to inject more than €1.1t of liquidity into the area. This is already helping lower the relative value of the euro. We would expect to see an acceleration of deals involving European companies, especially from acquirers in China, Japan and the US.

Our survey also finds companies across the globe with strong intentions to buy into the Asian growth story, with particular interest coming from Western Europe. A corresponding trend is the intention of companies from the Asia-Pacific region to buy outside of both their domestic market and immediate region — assets in Western Europe are a particularly strong focus for Asia-Pacific companies, led by respondents from South Korea and China.

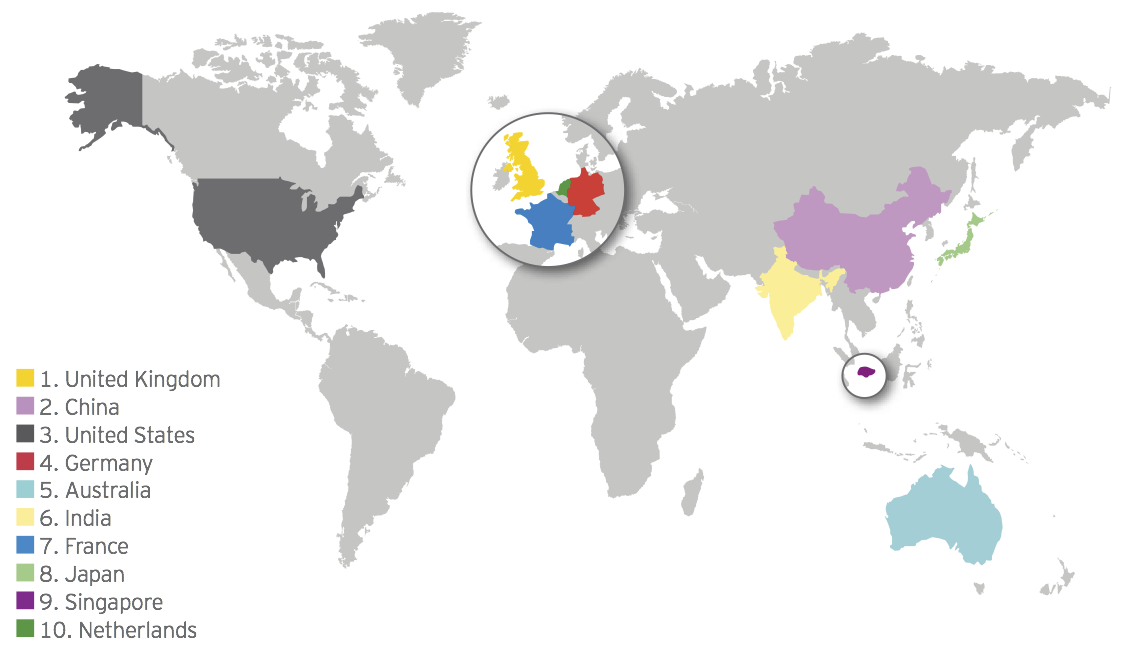

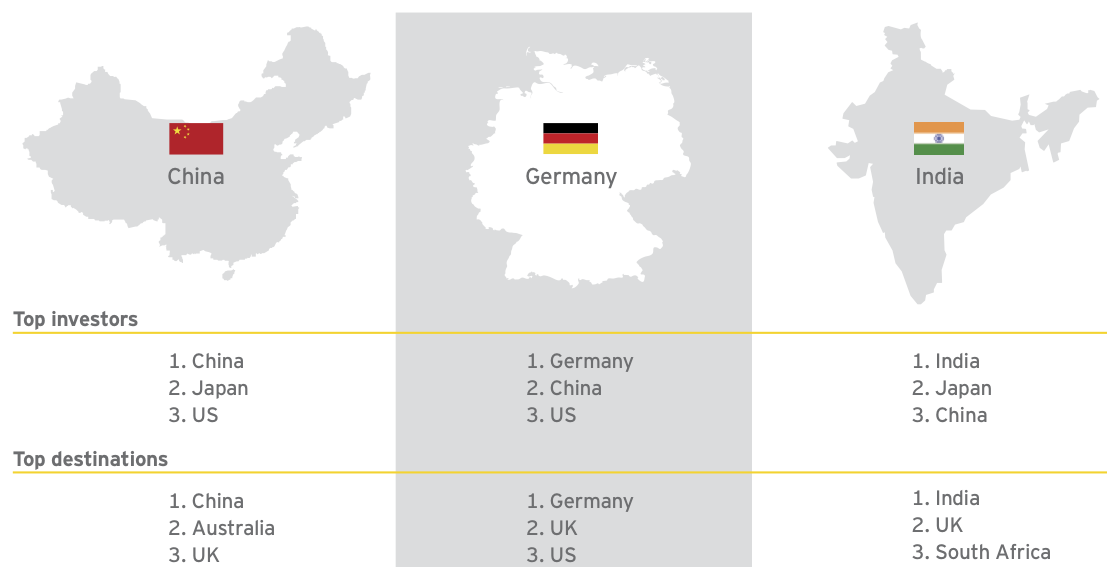

Top M&A markets and their key characteristics

Even amid headlines over its recent economic slowdown, mainland China remains a very attractive destination due to levels of growth that remain very strong relative to the global economy. The Chinese Government now targets annual growth at 7%, down from previous growth rates that ranged as high as 10%. However, there is no expectation of a hard landing or significantly greater deceleration. With economic rebalancing a stated Chinese policy, further investment opportunities should arise for inbound investors. The central bank has yet again lowered interest rates to stimulate the economy, providing a more favorable environment for M&A. The Government has also introduced a range of measures to encourage outbound acquisitions by Chinese companies, particularly targeting companies with intellectual property assets in the industrial and technology sectors.

Top sectors:

Media and entertainment

Automotive

Telecommunications

Germany has been the main bright spot within an otherwise depressed Eurozone. Recent economic releases and Purchasing Managers Index surveys point to an acceleration of growth, though it is still relatively low compared with historic averages. Germany’s high-quality corporate assets, especially in the industrials, chemicals and automotive sectors, are already attractive to foreign acquirers, and a weakening euro promises to make these assets relatively less expensive. The main competition for these assets is likely to come from China, Japan and the US. As for M&A within Germany, acquisitions by German companies have historically been focused on the domestic market, but we are beginning to see cross-border acquisitions strengthening, especially those focused on the US.

Top sectors:

Financial services

Diversified industrial products

Consumer products and retail

With investor sentiment in India seeing a significant recovery and stock markets hitting all-time highs, the country’s deal market is expected to improve. The new Indian Government’s pro-business stance should foster a more benign investment landscape for inbound investment — the recently announced annual budget focuses on increased infrastructure spending and lower corporate taxes to boost growth — and the economic outlook is increasingly promising. The outlook is further driven by a number of positive economic developments. Low oil prices will help shrink the country’s import bill and narrow its current account deficit. Easing inflation and looser monetary policy are expected to encourage consumer spending and investment. Looking from the outside, global investor sentiment toward India is currently very positive, especially compared with other emerging markets, which should also help boost growth.

Top sectors:

Automotive

Consumer products and retail

Financial services

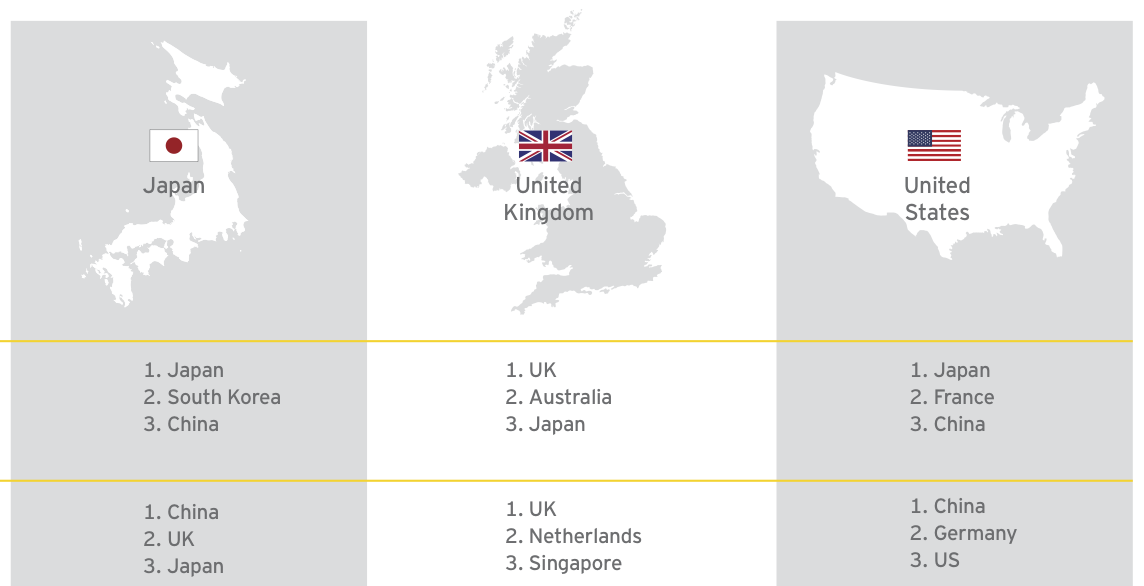

More than 20 years into its “Lost Decade” economic struggles, Japan continues to suffer from weak domestic economic growth combined with persistently low inflation. However, recent policy decisions by the Japanese Government and the Bank of Japan have reinforced policymakers’ determination to resolve this issue. The recent combination of lower oil prices and slow but steady improvements in consumer confidence and spending could steer the Japanese economy toward easing this cycle. In the deal markets, Japanese companies have increasingly shifted toward outbound acquisitions, especially in the industrials and consumer products sectors. This has been coupled with a small increase in inbound acquisitions into Japan, mainly by private equity investors but also in combinations involving US and Japanese companies in the technology and real estate sectors.

Top sectors

Automotive

Diversified industrial products

Life sciences

The United Kingdom has long been a favored destination for foreign firms accessing the wider EU market. With strong domestic growth in 2014, similar levels forecast through 2015 and a focus on reducing red tape, the UK should

be able to maintain its unique status as a global M&A hub. Among leading UK sectors likely to engage in M&A, life sciences and technology companies are strong innovators, the financial services sector is robust and consumer products companies are globally recognized. All should be looking to make acquisitions both domestically and abroad and will be attractive to foreign acquirers. As for downside risks, the impending UK elections and uncertainty regarding the timing of an expected interest-rate increase — which may raise the value of the pound, especially against the euro — may check the deal markets.

Top sectors

Technology

Diversified industrial products

Media and entertainment

The M&A market in the United States is expected to maintain its upward momentum and continues to be attractive to foreign investors. Positive US economic fundamentals, record stock markets and a low-interest-rate environment are all strengthening boardroom confidence.

US companies continue to perform exceptionally — the majority of the S&P 500 beat 2014 earnings and sales estimates — keeping investor morale up and driving M&A. The dollar’s increasing value should also make outbound deals appealing, especially those focused

on the Eurozone, where valuation and currency differentials are most apparent. The main potential downside for dealmakers in the US concerns the timing of the Federal Reserve’s first anticipated rate hike following the end of quantitative easing and the overall pace of the return to normalized interest rates; however, recent Fed announcements have helped allay these concerns.

Top sectors

Oil and gas

Technology

Consumer products and retail

About this survey

The Global Capital Confidence Barometer gauges corporate confidence in the economic outlook and identifies boardroom trends and practices in the way companies manage their Capital Agendas — EY’s framework for strategically managing capital.

It is a regular survey of senior executives from large companies around the world, conducted by the Economist Intelligence Unit (EIU). Our panel comprises select global EY clients and contacts and regular EIU contributors.

• In February and March, we surveyed a panel of more than 1,600 executives in 54 countries; more than 850 were CEOs, CFOs and other C-level executives.

• Respondents represented 18 sectors, including financial services, consumer products and retail, technology, life sciences, automotive and transportation, oil and gas, power and utilities, mining and metals, diversified industrial products, construction and real estate.

• Global companies’ annual global revenues ranged from less than US$500m (16%); US$500m– US$999.9m (24%); US$1b–US$2.9b (26%); US$3b-US$4.9b (15%) and greater than US$5b (19%).

• Global company ownership was publicly listed (67%), privately owned (28%), family-owned (3%) and government/state-owned (2%).

US highlights

Our latest Capital Confidence Barometer finds US companies are still several steps ahead of the global comeback in dealmaking. US executives are already transacting while their overseas counterparts are in preparation mode. They are looking at more innovative opportunities. And they are managing their Capital Agendas with rigor and discipline.

More than three-fifths of US companies plan to execute a deal in the next 12 months. That’s the highest percentage of US executives planning deals we have recorded since we launched the Barometer. It’s also higher than the number of global respondents currently planning deals. We titled our last US Barometer, in October 2014, “Ahead of the curve,” to acknowledge US dealmakers leading the M&A market as it emerged from its post–financial crisis doldrums. That trendline continues in this Barometer, as US companies plan to execute deals that, in many cases, may have long been in the works.

On the other hand, since deal activity in the United States has been stronger in recent years, it’s not surprising that US executives are staying ahead of any sign of an overheating market. More than half of them expect US M&A to decline. They are less optimistic about the prospects for deals closing, and about the number and quality of opportunities. Following months or even years of pipeline growth, many US companies expect their pipelines to decrease after pulling the trigger on their anticipated deals.

Some of the disparity between deal plans and market sentiment may reflect the kinds of acquisitions, and acquirers, now flooding the market. Most acquirers say they are focused on more innovative investments, largely deals under US$250m, rather than transformative megadeals. In large part, this is because a significant proportion of our respondents are middle-market acquirers, many of whom have not transacted in years — and most are planning just one or two deals. Whereas our respondents with revenues above $5b are more focused on deals above US$250m, and those with four or more deals in the works overwhelmingly plan to grow their pipelines in the next year. As always, M&A begets more M&A.

Famously, in the 1990s, as the deal markets were heating up, then—Federal Reserve Chairman Alan Greenspan warned about “irrational exuberance” in a widely reported speech. What is often forgotten is that Greenspan coined this phrase in 1996, nearly half a decade before the IPO market peaked. Similarly, these current deal markets have room to grow, even as dealmakers have long memories and more rigorous deal processes in place. In this Barometer, we find US companies pursuing a sensible approach we would call rational exuberance: acknowledging that M&A is back and now is the time to transact, but that this time, they will be driving the market, not allowing the market to drive them. (Richard M. Jeanneret, EY Americas Vice Chair, Transaction Advisory Services)

Key findings

US vs Global

61% and 56% expect to pursue acquisitions in the next 12 months

95% and 47% expect to complete more deals than in the prior year

89% and 77% say their largest deal in the next 12 months will be $250m or less

92% and 84% are focused on cross-border M&A in the next 12 months