By Pip McCrostie – Ernst & Young

Growth mandates — driven by increased confidence and credit availability — will spur M&A activity across mature and emerging markets.

Our latest Capital Confidence Barometer suggests a return of deal activity after a five-year period of falling M&A globally. The fundamentals are in place to foster M&A: confidence in the global economy is at its highest for two years; cash is in abundance, and credit is readily available.

This does not mean we will see a return to boom-time dealmaking. That was unsustainable, but so is the scarcity of deals we have been experiencing since 2009. Strategies to improve operational efficiencies have been largely implemented — organic measures alone may no longer meet growth mandates. Many may now consider inorganic options in order to grow. Sectors such as telecommunications, life sciences, automotive, oil and gas, technology and consumer products are likely to be at the forefront of deal activity.

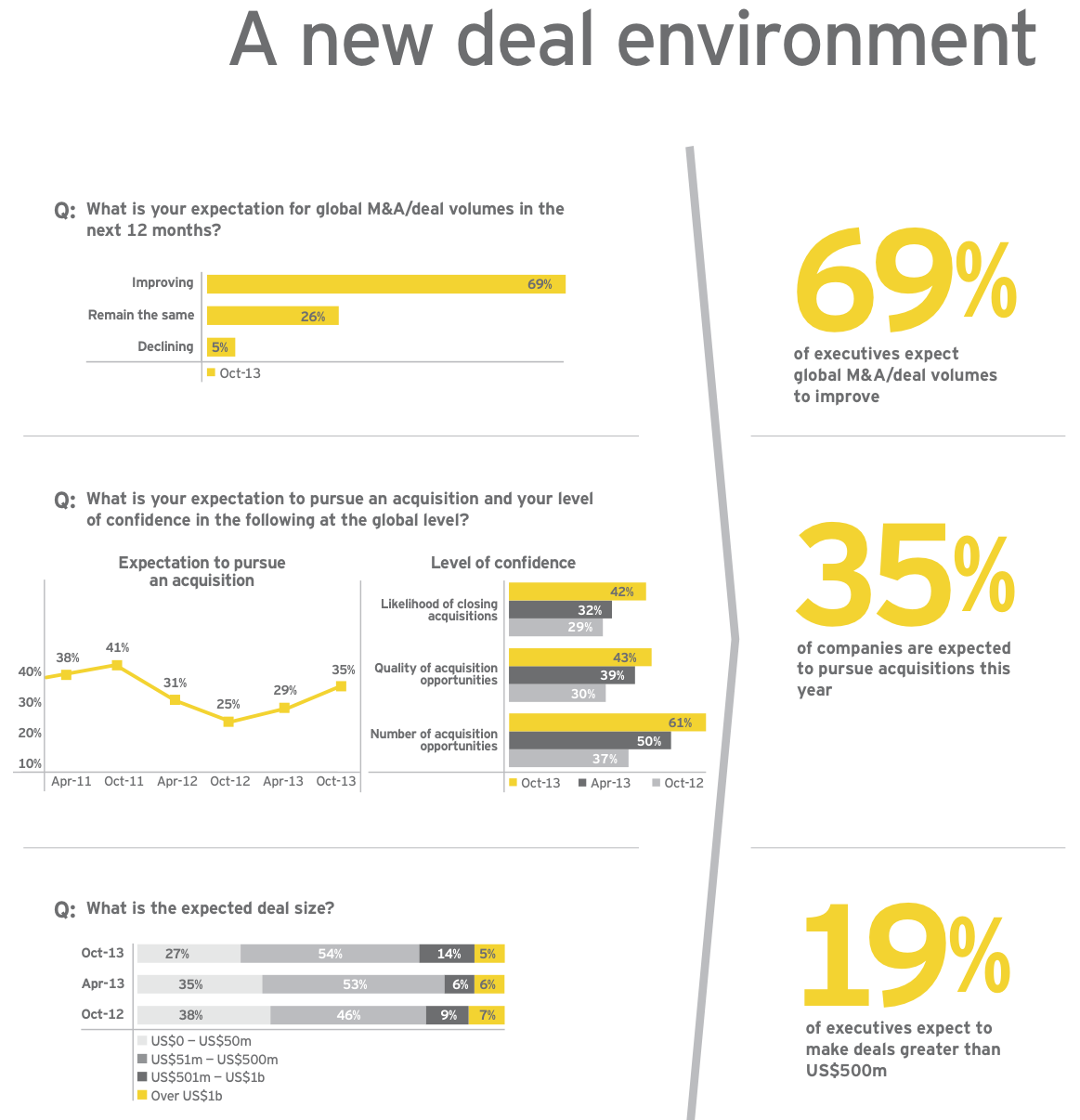

Confidence in closing deals has significantly increased, as have the number and quality of M&A opportunities — this is strengthening buying intentions. An overwhelming majority — 69% of executives expect an increase in deal activity in the market. Critically, more than a third plan to act themselves and the acquisitions they are considering are of a size to create real momentum in the global M&A market.

The culture of M&A caution has been understandable given the unprecedented economic turmoil we have experienced. The market is also very sensitive to geopolitical issues — continued volatility could subdue deal flow. However, with organic growth measures providing finite returns, M&A could once again be a preferred route to meaningful growth.

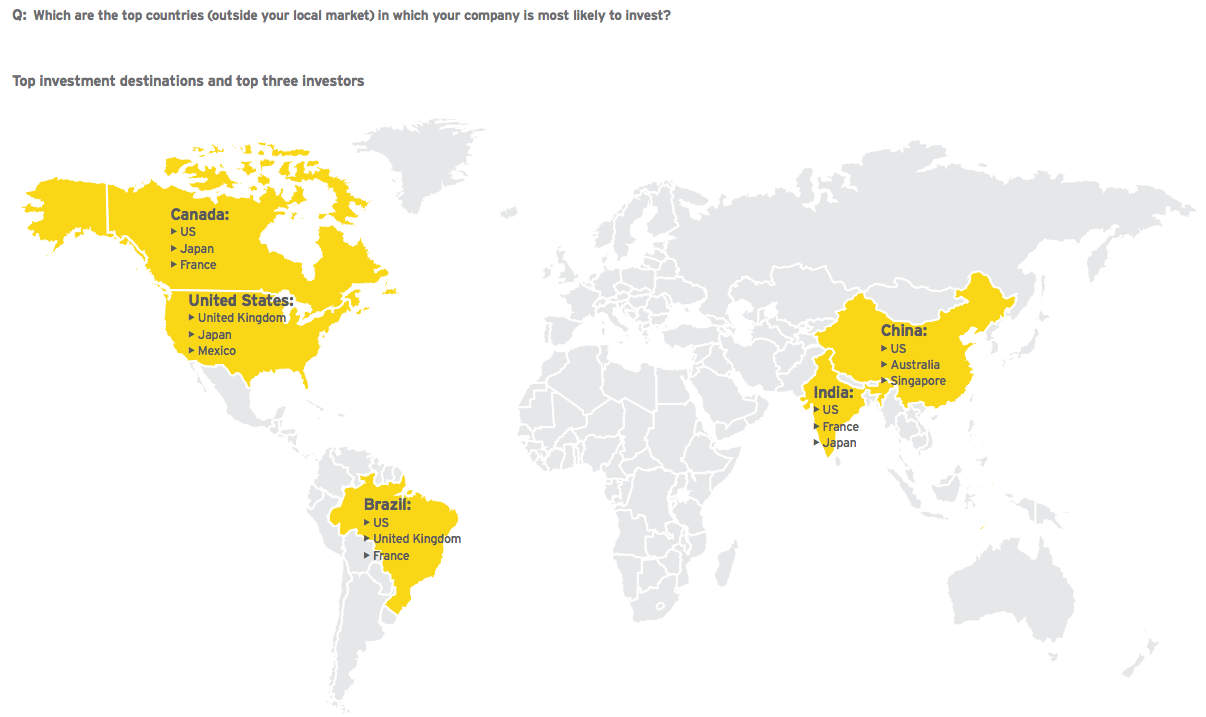

So, barring further major shocks, M&A and investing will return to prominence on the capital agenda. With companies again allocating more acquisition capital to developed markets such as the UK, US, Japan and Germany — as well as China — these economies are expected to lead the return of M&A. Simultaneously, companies will continue to pursue emerging markets — such as India and Brazil — and frontier markets — such as Vietnam and Indonesia — as growth mandates take hold.

Key findings

69% expect global deal volumes to improve

65% see the global economy improving, pushing economic confidence to a two-year high

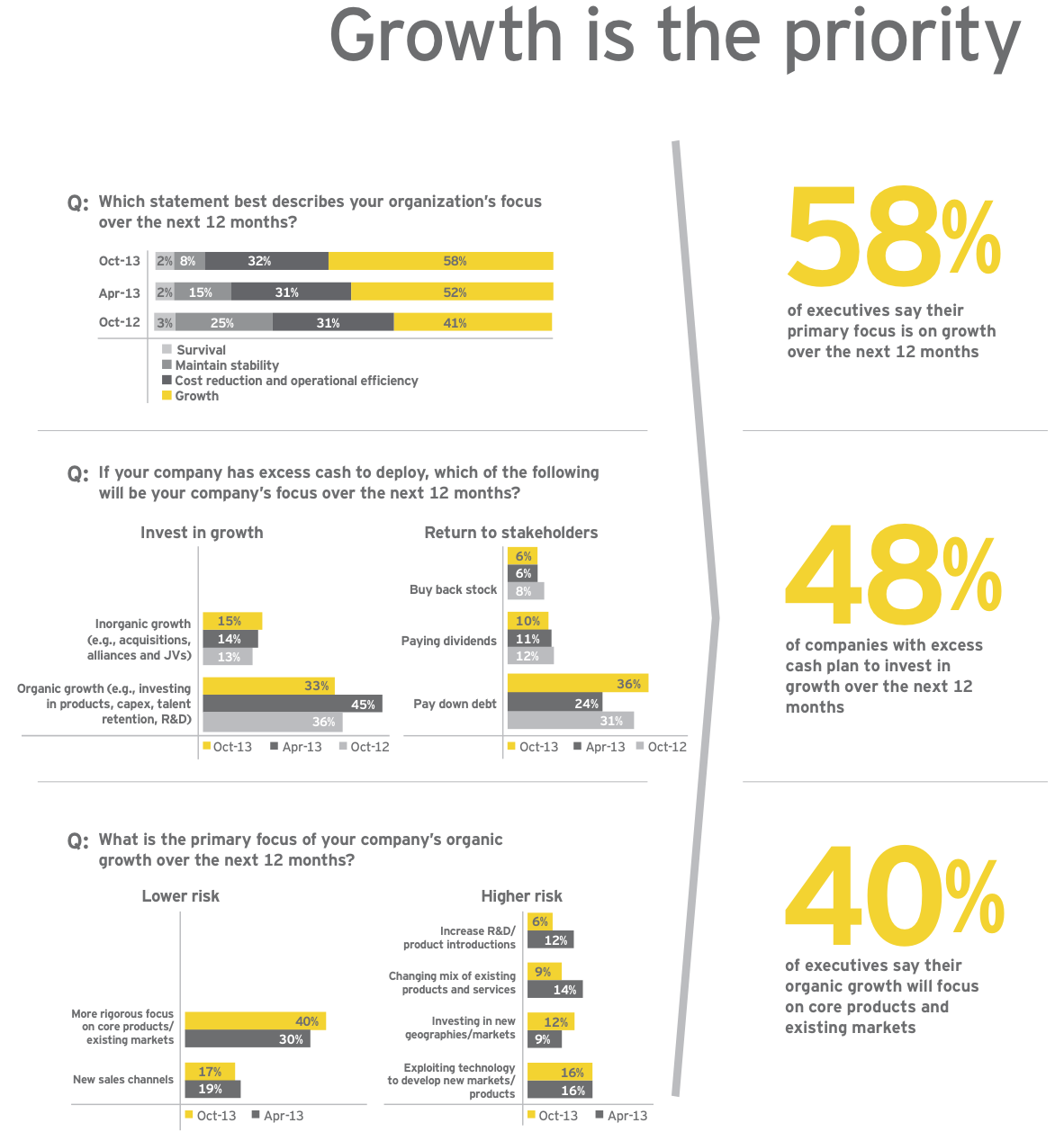

58% consider growth their primary focus

35% plan to pursue an acquisition

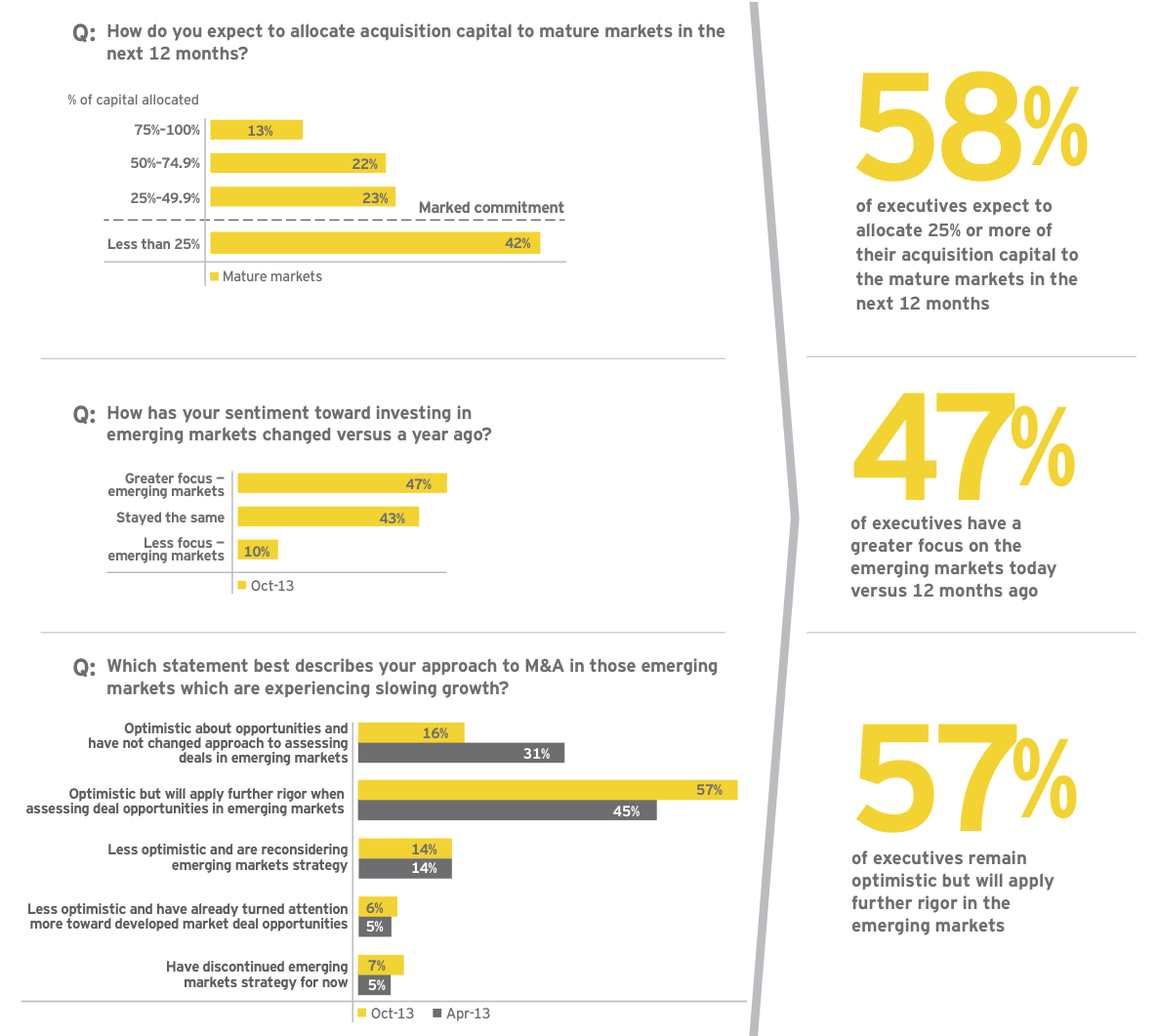

47% have a greater focus on investing in emerging markets

87% view credit availability as stable or improving

53% plan to use debt and equity as their primary source of deal funding

“With companies again allocating more acquisition capital to developed markets, these mature economies are expected to lead the return of global M&A.”

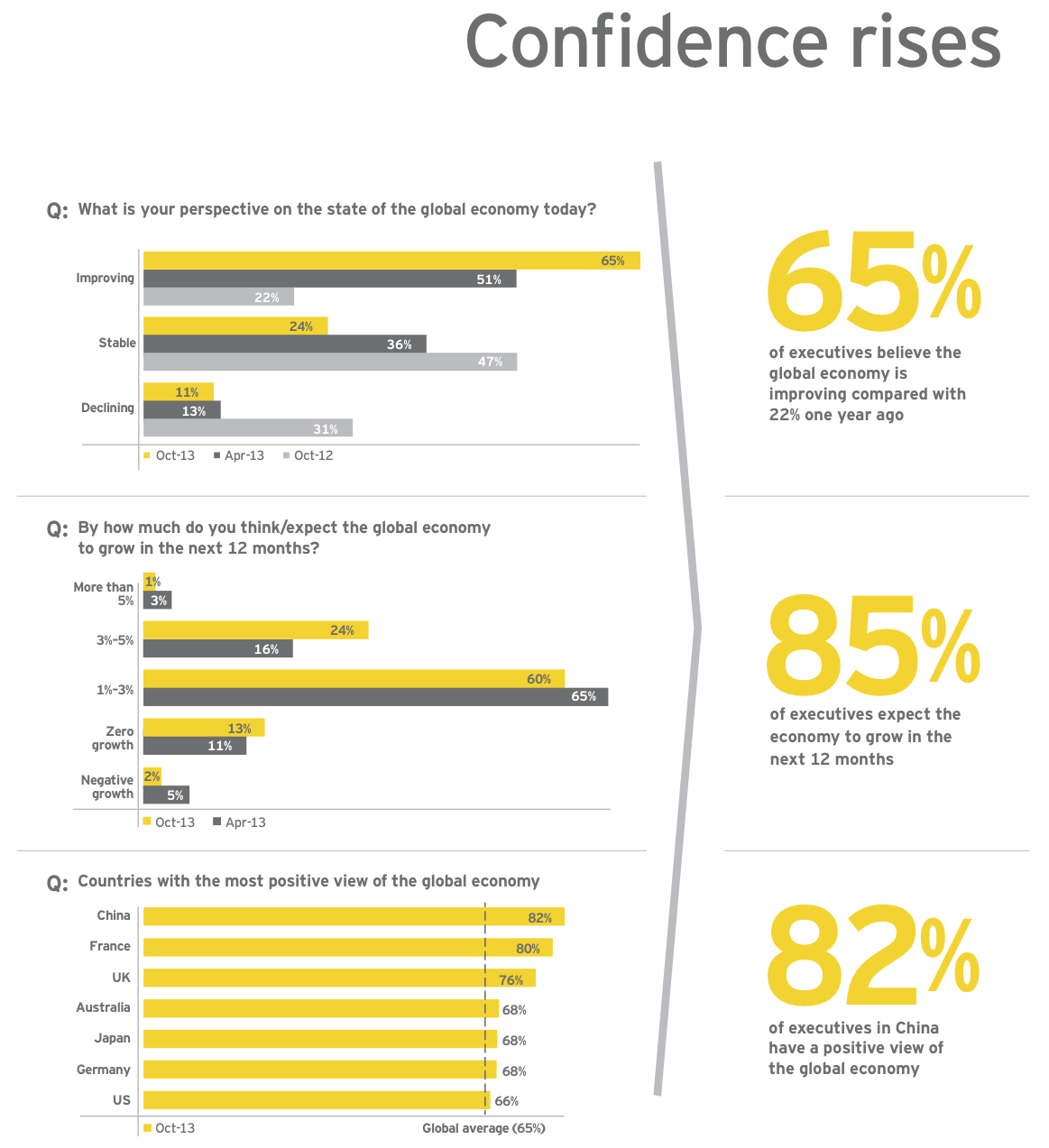

Economic outlook — confidence at two-year high

Executives are more optimistic about the global economy than at any point in the last two years.

Almost 90% of all executives are confident the economy is stable, and two-thirds believe it will improve at an accelerating rate. Informing this confidence is a global economy on sounder footing — improvement in economic conditions in mature economies and more stabilization in the major emerging markets.

The outlook for Europe has brightened in the last six months. Higher levels of employment, rising GDP and more access to capital provide evidence that the region’s economic downturn is subsiding. In the United States, corporate earnings, employment growth and credit availability are also improving.

This growing confidence may drive dealmaking globally and across multiple industries as short-term market stability returns.

• Economic confidence reaches two-year high

Confidence levels have risen dramatically over the last 12 months — a clear indication the economy is improving at an increasing rate. This confidence resonates from stable underlying economic fundamentals, particularly in mature markets: growing GDP, credit availability and increased job creation. Those who see the economy declining fell to 11%, the lowest level in two years.

• Growth expectations continue to rise

Substantially all respondents anticipate economic growth, and those expecting growth in the 3%-5% range increased significantly. This correlates with companies’ increasing ability to invest and stakeholder demand for meaningful growth.

• Developed economies will prompt global dealmaking

Some of the world’s most mature and influential markets are increasingly confident in the strength of the global economy. They believe the economic fundamentals are sound, and the recurring ebbs and flows have largely been eliminated. Chinese respondents are the most confident, but mature markets such as the UK, US, Germany and Japan also have high confidence.

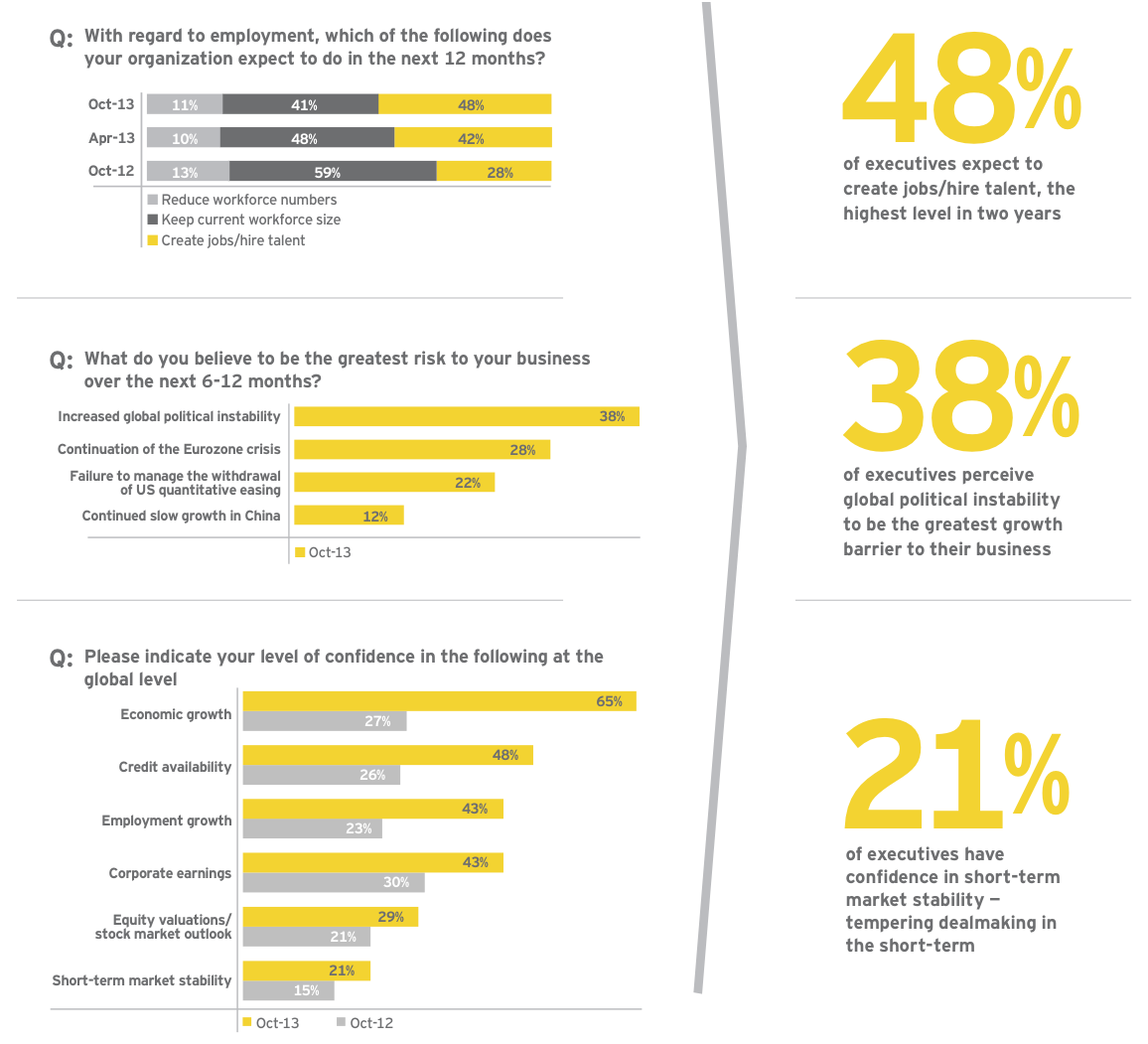

Cautious optimism will increase dealmaking

• Commitment to job creation underscores plans for investment

Our respondents’ commitment to job creation is at its highest level in two years and highlights that companies need to hire as they prepare for the coming wave of growth. The sectors where most jobs will be created are oil and gas, automotive, and technology, which are also among the sectors most likely to pursue acquisitions.

• Political instability outweighs economic concerns

While global political instability is believed to pose the greatest near-term risk, it is unlikely to derail the fundamental push for growth. Similar to the Eurozone or US crises, the recent unrest in Syria and Egypt pose challenges; however, these challenges should not be detrimental to the recovery of the global economy over the long term.

• Ongoing market volatility tempers growth and investment mandates

Although confidence in leading economic indicators has improved significantly over the last 12 months, only 21% of respondents have confidence in short-term market stability — which is not yet aligned with their confidence in other leading economic indicators. Consequently, companies are carefully managing the rate at which they implement their growth and investment strategies. As such, the dealmaking comeback will be measured.

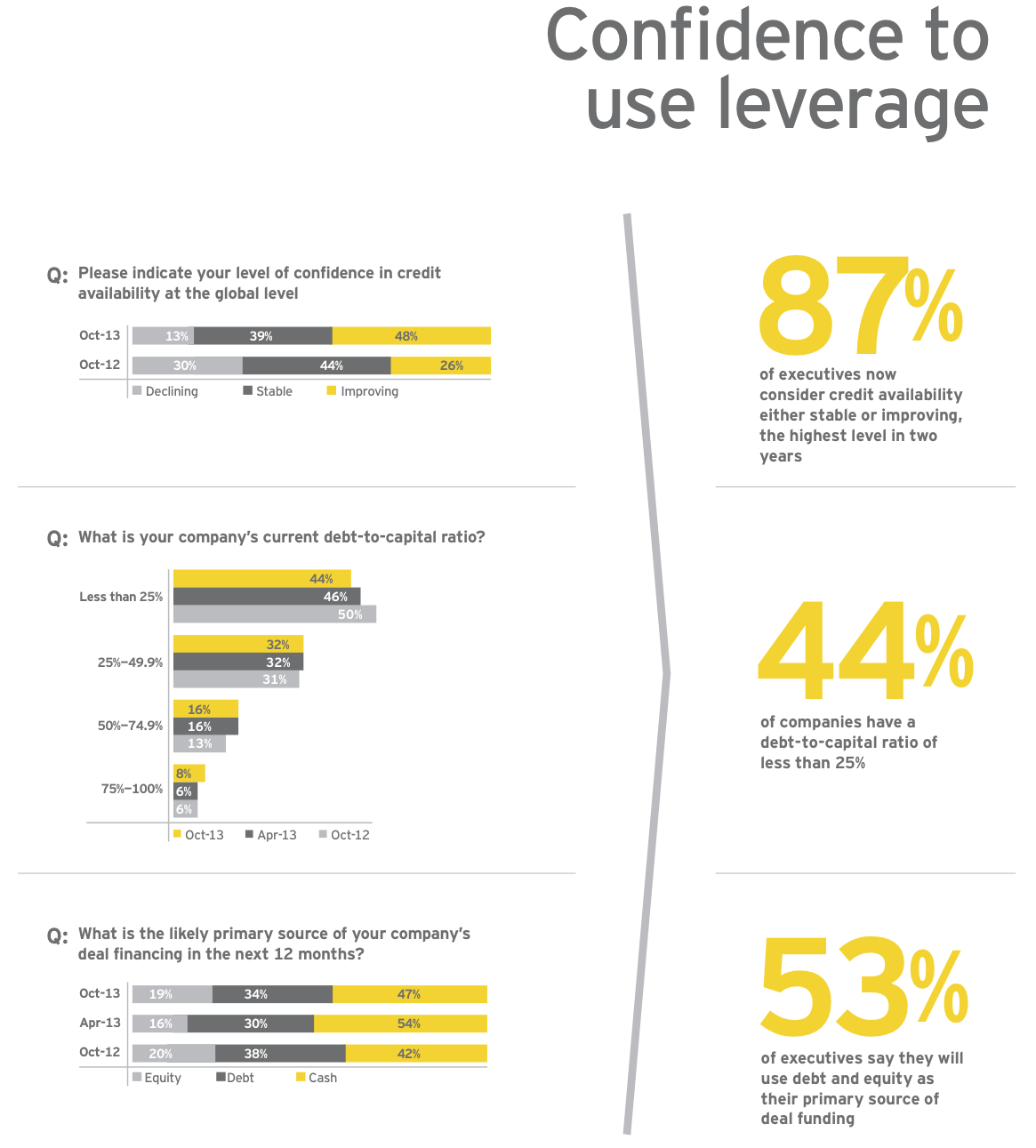

Access to capital — credit availability drives momentum

To advance their strategic imperatives, companies will take advantage of improving credit conditions.

A willingness to use leverage and the view that credit availability is at the highest point in two years signal a growing confidence in the long-term economic outlook.

The returning use of leverage also indicates a fundamental shift in the dealmaking environment, which was previously dominated by conservatism and the reliance on cash for financing.

The overall optimism, expectations for growth and the use of greater leverage will lead the way to more and larger deals, which will create M&A momentum globally.

• Credit availability inspires growth

The vast majority of executives consider access to credit as stable or improving. Furthermore, the sentiment on improving credit is almost double what it was 12 months ago. This confidence, coupled with positive views on the global economy and sound economic fundamentals, will accelerate dealmaking.

• Debt-to-capital ratios have been carefully managed

Over the last six months, debt-to-capital ratios remained largely constant while access to credit continued to improve. This disciplined use of leverage ensures companies have the capacity to access the credit markets as they undertake larger transactions.

• Planned use of more debt and equity signals shift to larger deals

The confidence to use more debt and equity to finance deals represents a shift away from risk aversion and smaller, cash-based transactions. The use of more leverage also highlights the need for larger deals to address growth mandates — and signals the return to a more active M&A environment and larger transactions.

Growth strategies — investment intent tops Capital Agenda

Growth is now a global imperative as almost 60% of executives say they plan to accelerate their growth strategies over the next 12 months.

Companies have weathered a prolonged period of uncertainty. During this time, they have strengthened their balance sheets and largely optimized their capital structures. Companies are now ready to capitalize on the improving global economy and credit markets to implement their growth agendas.

Growth strategies are shifting from organic to inorganic strategies. Coupled with positive leading indicators, the greater focus on growth points to a return of increased M&A activity and larger deals, globally.

• Focus on growth is at two-year high

Over the next 12 months, growth is the primary focus for almost 60% of companies. Continued operational efficiency and cost control measures have largely eliminated concerns about stability and survival.

• Excess cash is used to pay down debt and fund growth

In the near term, 36% of companies will use excess cash to pay down debt, which is one of the remaining ways to optimize their capital structures. And 48% of companies plan to use excess cash to fund growth — starting with lower-risk organic strategies. As companies find organic strategies no longer sufficient to achieve desired growth rates, they may look to M&A.

• Organic growth strategies will center on core products and existing markets

To address their need for growth, companies will initially focus on lower risk organic platforms: existing products, channels and markets. This strategy allows them to pursue low risk growth while maintaining financial discipline and governance objectives. As they exhaust those lower-risk organic options, companies will pursue higher-risk organic strategies: new products, channels and geographies.

Investment tops companies’ Capital Agendas

Mergers & acquisitions — more and larger deals expected

“True intent” to make larger deals is now visible — as expectations for deals greater than US$500m and up to US$1b have more than doubled in the last six months.

These expectations, along with increased deal volumes, are clear indicators that a more robust dealmaking environment is on the horizon. They signal companies have confidence in their capital structures, in deal fundamentals and in a sustainable economic recovery.

As companies begin to act on their intentions for dealmaking and their imperative to grow, it will trigger deals of varying size across the global marketplace.

Sectors with the highest level of anticipated dealmaking are telecommunications, life sciences, oil and gas, automotive, consumer products and technology.

• Global deal volumes expected to improve

Almost 70% of executives expect deal volumes to improve over the next 12 months. Deal volumes resonate from the alignment of core fundamentals: positive economic sentiment, enhanced credit availability, the imperative for growth and the expectation to create jobs. Growth in volume will also come from the returning strength of mature markets, which brings incremental growth in the BRICs and new frontier economies.

• M&A expectations rise — driven by increased quality, number of opportunities and likelihood of deal closing

With core fundamentals in place to support M&A, over one-third of companies will pursue acquisitions in the next 12 months vs. just one-quarter a year ago. This 40% improvement in the number of companies expecting to pursue acquisitions resonates from the notable increase in the last 12 months in the number and quality of acquisition opportunities, as well as significant improvement in the likelihood of deal closing.

• Clear focus on larger deals

Executives who expressed the intent to engage in larger deals (i.e., US$501m to US$1b range) more than doubled from six months ago. And those focused on smaller transactions (<US$51m) fell to just 27%. These are significant shifts that clearly indicate a more robust dealmaking environment is on the horizon.

Top cross-border investment destinations

Increased dealmaking globally will be driven by mature markets

• Although acquisition capital will be allocated globally — the primary share is designated for mature markets

Mature economies will attract the majority of acquisition capital over the next 12 months. The returning desire to invest in the mature markets is attributable to a rebound in their economies, as well as the perceived safety and quality of underlying opportunities.

• Emerging markets interest grows

Over the last 12 months, 47% of executives indicate they have placed greater focus on investing in the BRIC (27%) and non-BRIC (20%) emerging markets as they search for new strategic opportunities. However, the mature markets continue to be an important investment destination.

• M&A in slowing-growth emerging markets requires more transaction rigor

While certain emerging markets have experienced slowing growth, executives remain largely optimistic about the opportunities they present, provided greater rigor is applied to dealmaking. Unlike their mature counterparts, emerging markets continue to rapidly evolve and transaction risk must be managed.

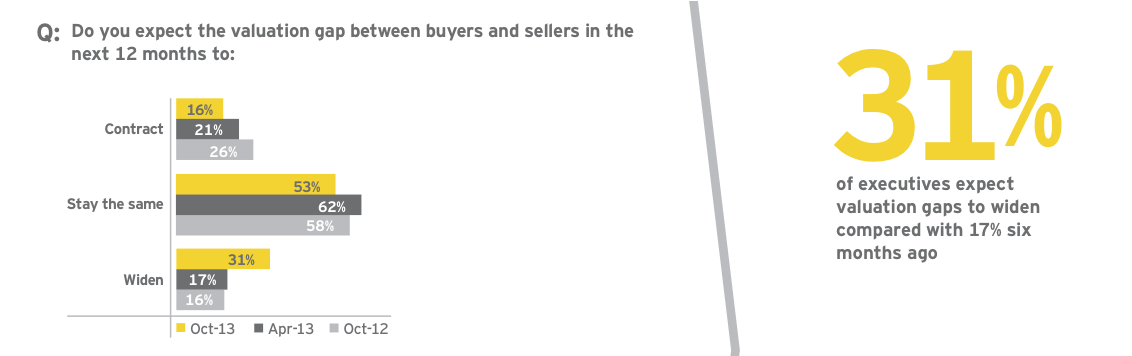

Valuation gaps are expected to widen as dealmaking accelerates

Valuation gaps expected to widen

As transaction volumes accelerate, there is a natural divergence between buyers’ and sellers’ expectations on pricing. Thirty-one percent of executives expect valuation gaps to widen over the next 12 months vs. 17% six months ago. This widening gap results from buyers and sellers adjusting their expectations at different rates.

Pricing gaps aside, the market fundamentals are falling into place to support transactions that make strategic sense

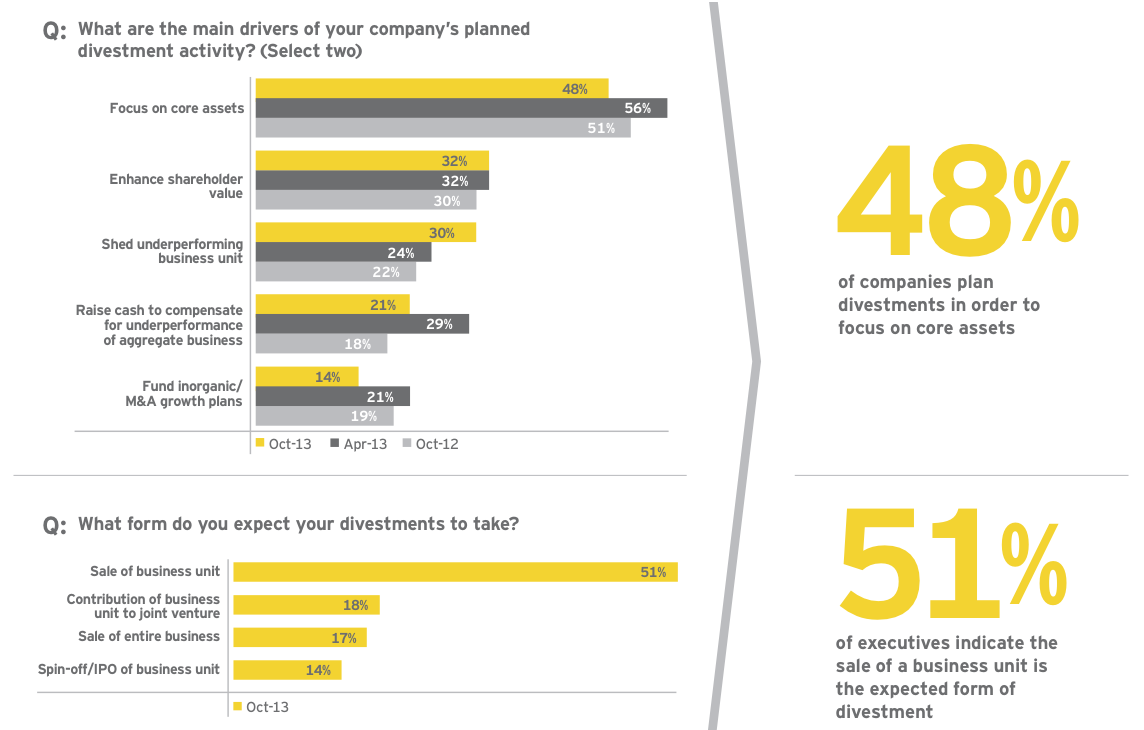

Divestments are fundamental to driving strategic value

• Divestments enable corporate objectives

Recognized for their strategic value, divestments are an effective tool to address a variety of corporate objectives. Companies will continue to shed nonstrategic and underperforming assets as they optimize their capital structures and focus on their core business. Fewer plan to use divestments to raise capital since credit is now more readily available.

• Business unit sales are the preferred structure for divestments

At 51%, sales of non-core business units will dominate the divestment environment, as companies continue to strengthen their corporate structure.

About this survey

The Global Capital Confidence Barometer gauges corporate confidence in the economic outlook, and identifies boardroom trends and practices in the way companies manage their Capital Agendas — EY’s framework for strategically managing capital.

It is a regular survey of senior executives from large companies around the world, conducted by the Economist Intelligence Unit (EIU). Our panel comprises select global EY clients and contacts and regular EIU contributors.

• In September we surveyed a panel of over 1,600 executives in 72 countries; half were CEOs, CFOs and other C-level executives.

• Respondents represented more than 20 sectors including financial services, consumer products, technology, life sciences, automotive, oil and gas, power and utilities, mining and metals, diversified industrial products, and construction.

• Companies’ annual global revenues ranged from less than US$500m to greater than US$5b: <US$500m (19%); US$500m — US$999.9m (24%); US$1b — US$4.9b (30%); and >US$5b (27%).

• More than 900 companies would have qualified for the Fortune 1000 based on revenue.

• Company ownership was publicly listed (65%), privately owned (20%), family owned (7%), government/state-owned (5%), and PE/portfolio owned (3%).