International Relations Conference on India and Development Partnerships in Asia and Africa: Towards a New Paradigm (IRC-2013)

Abstract

The African economy provides an investment opportunity for International players both in terms of procuring natural resources and opening up a potential one billion consumer market. Along with the vast investment potential, on the downside firms face challenges that come from investing into nations with corporate governance, infrastructure and regulatory environments that are not as conducive for investments as found in developed nations. In this paper, we study Foreign Direct Investments (FDI) in the form of cross border acquisitions made by Indian firms in Africa during the 2002 to 2010 time frame. We report on the growth of Indian investments into Africa, nature of investments during this period and short time cumulative abnormal returns (CARs). We select two large deals that were subsequently withdrawn, to understand the nature of issues that come up while Indian firms invest in Africa. The paper’s findings provide possible avenues of partnerships through investment in Africa and the challenges associated with the same.

1. Introduction

While economic growth has been slowing down around the globe, the outlook for African economies is very positive and expected to outpace the growth of other economies (Ernst & Young, 2013). Reflecting the growing importance of Africa as an investment destination, the value of Foreign Direct Investments (FDI) into Africa has grown from an annual figure of $ 9 billion in 2000 to $ 50 billion in 2012 (UNCTAD, 2013). Traditionally investments into Africa have been in the extractive mining, quarrying and petroleum sector. In the recent years there has also been a growing awareness of Africa’s potential 1 Billion consumer market and a positive demographic balance with about 60% of the population below 25, resulting in a growing interest in consumer related and infrastructure sectors such as financial services, food beverage, motor vehicle, telecommunication etc. In their annual attractiveness survey on Africa in 2013, Ernst & Young report that firms that have already established a business presence in Africa are very positive on further investments into Africa, and have ranked Africa as the second most attractive destination for investments, after Asia. Emerging market firms have been showing a rising interest in investing in Africa. With firms from Malaysia, China and India being the largest emerging market investors into Africa in 2012.

In recent years, Indian investment in other developing countries has become a major component of South-South co-operation. The development indicators have motivated Indian firms to invest in Africa through a growing number of Greenfield projects and cross border deals and helped in fostering d between the two nations. African economy provides an investment opportunity for International players both in terms of procuring natural resources and opening up a potential 1 billion consumer market. African markets provide substantial growth prospects for firms investing into Africa, however they also face challenges that come from investing into a country with different corporate governance and regulatory environment. For example, the Bharti MTNL deal could not be carried out due to regulatory hurdles.

In this paper, we study outward FDI in the form of cross border acquisitions made by Indian firms in Africa during the 2000 to 2010 time frame. We report on the nature of investments during this period. We report the 3 day and 11 day cumulative abnormal returns (CARs) using the event study methodology. We also use a case study approach to analyze the reasons behind two deals above $ 1 Billion that were withdrawn to understand the hurdles which lead to the deal withdrawal, to gain insights for further south-south co-operation with Africa.

2. Literature Review

We draw on literature on outward investments by developing market firms and also on investments into developing market firms. Sethi D, Guisinger, Phelan, Berg (2003) study trends in FDI into different regions and report that developing countries such as Asia and Africa followed a very restrictive policy and almost hostile stance towards inward investments in the 1980s, which prevented significant FDI inflows into these countries. Governments from these countries gradually opened up these economies during 1991-97 which lead to a growth of investments into these countries after this liberalization period. Panagiotis, Liargovas and Skandalis (2012) find a direct positive causality between trade openness and inflows of FDI in developing economies including Africa. Following opening up of African economies FDI into Africa has grown from an annual figure of $ 9 billion in 2000 to $ 50 billion in 2012.

Yiu, Lau and Bruton (2007), Elango and Patnaik (2007), Filatotchev, Strange, Piesse, Lien 2007, Hoskisson, Eden, Lau and Wright (2007) study outward investments by developing countries and argue that the strategy followed by these nations is not the same as that followed by developed countries and are more aggressive in their expansion strategy. They have expressed a need for theory development on outward investment strategy of developing nations. Pradhan, Abraham (2005_ examine the patterns and motivations behind cross border acquisitions by Indian firms during 1999 to 2001, which was soon after the liberalization of inward investment policy by developing nations. At that time they report that Indian investments at that time were directed largely towards developed nations. In a more recent study Gubbi S, Aulakh P, Ray S, Sarkar M, Chittoor R. 2010 argue that Indian firms were forced to expand internationally to survive in an increasingly competitive home environment. Like Pradhan & Abraham (2005), Gubbi et al(2010) also find that during their period of study from 2000 to 2007 a majority of investments by Indian firms were directed towards developed countries of Europe and North America. However, there has been a growth in south-south investments too. For examples firms from Malaysia, China and India were the largest emerging market investors into Africa in 2012. In this paper we explore outbound FDI in the form of cross border acquisitions by Indian firms into Africa.

3. Data and Methodology

We use SDC Thomson database to collect data on African acquisitions where the acquirers are Indian publicly listed firms and the targets are African firms. The time period for the study is 2002 to 2010. This time frame allows us to analyze the impact of reforms in the outward FDI policy of India which commenced in 2000 and also various measures taken by African nations to attract FDI including the The New Partnership for Africa’s Development launched in July 2001 which had as its main objective the increase of FDI into Africa. Around the same time, in March 2002, the United Nations Conference for Trade and Development (UNCTAD) brought together policy makers to deliberate upon strategies for increasing FDI flow to Africa. We expect to see an impact of these change in policies in the 2002 to 2010 time frame.

We use SDC Thomson data base to extract information on acquisitions by Indian acquirers during 2002 to 2010 where the target nation belongs to the African Continent. We find that during the 2002 to 2010 time frame Indian firms completed 68 acquisitions and withdrew 5 acquisition attempts in Africa. We filter out acquisitions by unlisted firms and finance firms from our list of deals. We are left with a data set of 42 completed deals and 5 withdrawn deals.

The first part of our analysis describes the characteristics of the completed deals. The number of deals used in this analysis is 42 out of a total of 661cross border deals completed by Indian firms in this period. In the second part of the analysis, we conduct an event study to understand whether the deal was beneficial to the Indian acquirers during the period of study. For this objective, we filter for completed deals by listed entities and investigate the deals to understand short term 3 day and 11 day cumulative abnormal returns using the methodology described by MacKinlay (1997) where in the normal returns for selected acquiring firms in relation to the market are estimated using the market model as described in equation 1.

Rit = αi + βiRmt + εit (Equation 1)

Rit is the expected return on the firm.

Rmt is the return on the market portfolio

αi is the intercept term

βi is the sensitivity of the return on the firm to market returns

εit is the zero mean disturbance term

We use an estimation window of -250 to -50 days before the event date to estimate normal returns for the firm. Then, we use a short term event window of 3 days (-1 to +1) and 11 days (-5 to +5) days around the announcement date to determine the short term market reaction to the deal. The event study methodology assumes market efficiency and that the market reaction is an indication of market perception of success or failure of a deal. Hence a significant negative cumulative abnormal return would indicate negative prospects as perceived by the market and positive abnormal returns would indicate to a successful deal.

The third part of our analysis follows an analysis of withdrawn deals using case study approach. The objective of doing this analysis is to gain a better understanding of hurdles that lead to withdrawal of a deal. We choose case study approach because of the unique characteristics and circumstances of the reasons of withdrawal which cannot be highlighted through an overall analysis. For this purpose, we choose the highest transaction value deals which were withdrawn. We hope to gain insights into causes for withdrawals which can provide inputs to policy makers in India and in African nations. This in turn could lead to better prospects for south-south co-operation.

4. Results

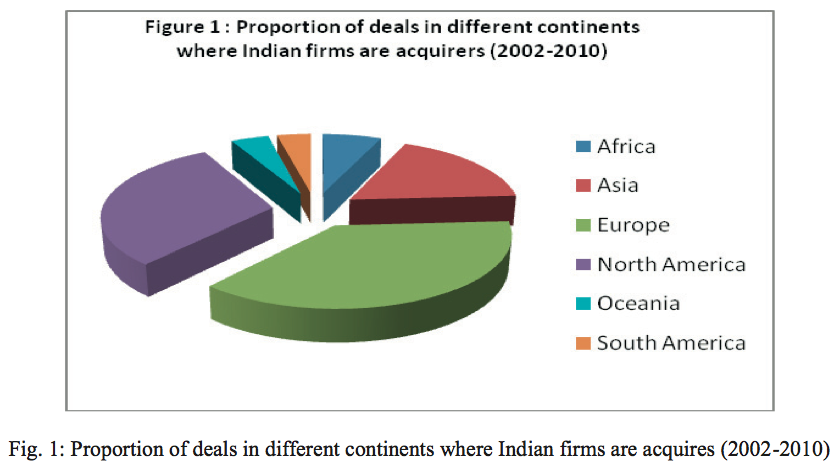

During the period of our study from 2002 to 2010, we obtain data from SDC on deals where in Indian listed firms are the ultimate acquirer, After filtering out acquisitions by unlisted firms and by finance firms we have a sample of 661 completed deals by Indian firms during this period. Figure 1 provides a geographical distribution by continent of cross border deals by Indian firms.

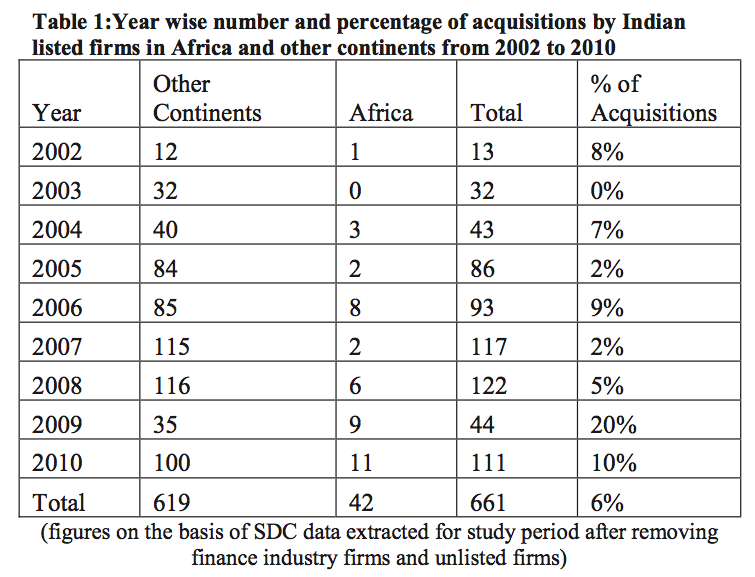

Our results match those by Pradhan & Abraham (2005), Gubbi et al(2010) who report that Indian cross border acquisitions have largely been directed towards the developed nations of North America and Europe. While 6% of the deals are directed toward Africa, 18% towards other Asian firms and 37% and 31% are directed towards Europe and North America respectively. Even though the percentage of Indian investments into Africa is small we explore the number of acquisitions each year into Africa by Indian firms to understand if there is any change in pattern during the period of our study. Table 1 provides a perspective of how many deals have been completed by Indian firms in Africa during the period 2002 to 2010 on the basis of our selected sample data.

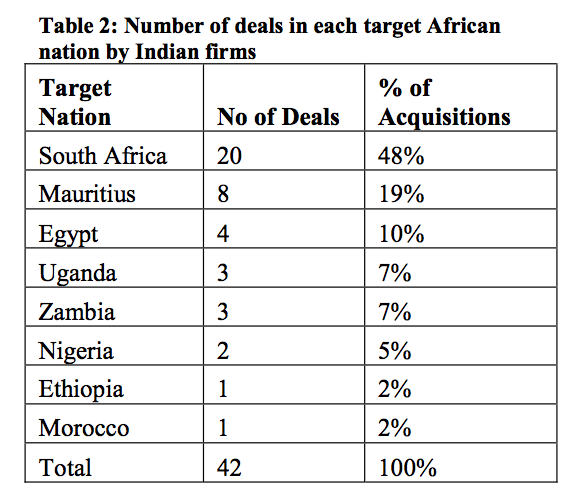

There has been a substantial increase in acquisitions targeting Africa by Indian firms during 2009 and 2010. This reflects the growing interest in south-south investments in the recent years. Within the destination nations we find that Indian firms have invested mainly in South Africa and Mauritius which is at an advanced stage of development in infrastructure and corporate governance as compared to other African nations. Table 2 lists the countries targeted by Indian acquirers in our sample of 42 deals. 48% of the deals are in South Africa followed by Mauritius and Egypt. South Africa has emerged as a highly favoured destination for FDI and has performed well on indicators of economic potential, infrastructure and business friendliness. Links between Mauritius and India originate from ethnic links and a friendly investment climate and favourable tax treaties.

Table 3 provides the industry classification of the acquisitions in Africa during the period of our study. It is interesting to note that Drugs and Pharmaceuticals firms have been large acquirers into Africa. Ranbaxy, Lupin, Glenmark have completed multiple deals in Africa. While there have been deals in the extractive and petroleum sectors these have been by private entities such as GAIL which are unlisted hence not in our sample.

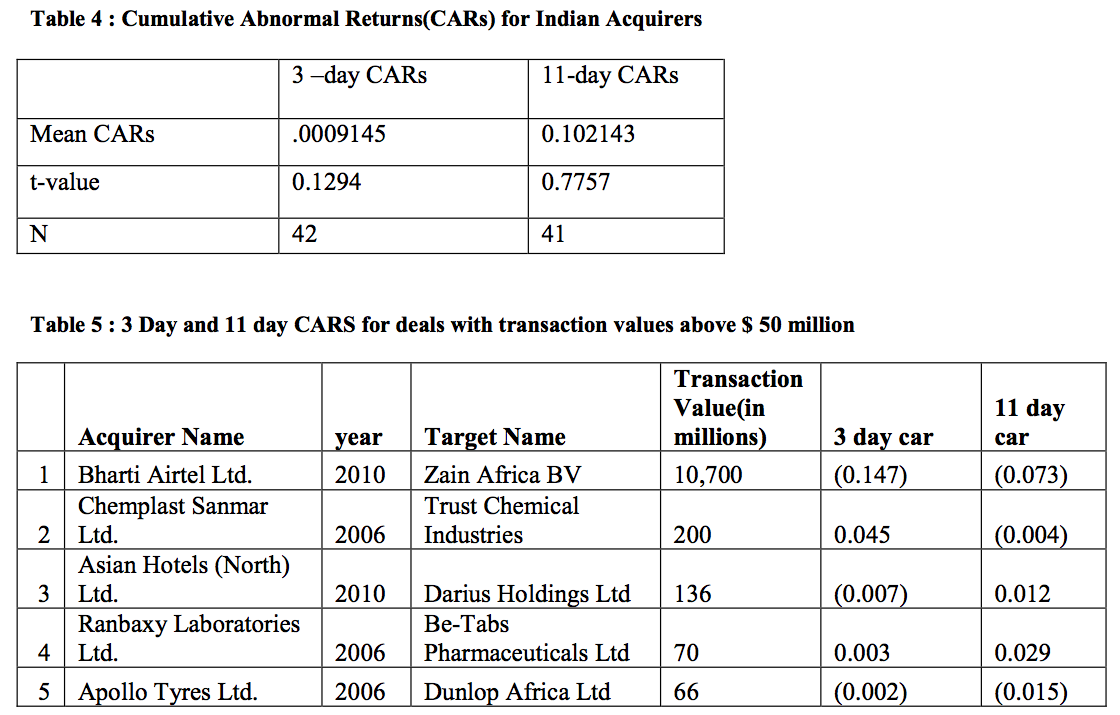

Announcement Effect: Next we conduct the event study to test the cumulative abnormal returns (CARs) for acquirers during a 3 day and 11 day window to test if these are significantly different than zero. Table 4 reports the results of our study. We find that the mean CARs are not significantly different from zero in either the short term announcement window of 3 days or 11 days. Hence, the market neither reacts positively or negatively on an average to a cross border deal announcements in Africa. Plotting individual deal announcement effects for deals above $50 million in Table 5, we find that the reaction of the market to deal announcements is mixed. While 3 day and 11 day CARS are negative for Bharti and Apollo deals. The 3 and 11 day CARs for the Ranbaxy deal are positive. The individual firm data does not point to a significant positive or negative reaction to deal announcements.

5. Analysis of withdrawn deals

To understand the challenges with respect to flow of FDI between India and Africa, we analyze two failed cross border acquisitions, which if would have completed would have added synergistic benefits to both the companies and added to FDI for the countries. We chose these cases on the basis of the transaction value of the deals. Bharti Airtel – MTN deal had a transaction value of USD 11.38 billion and ONGC Videsh Limited – AKPO had a value of USD 2 billion.

5.1. Case 1 : Bharti Airtel – MTN deal

Bharti Airtel commenced its mobile services in India in 1995, in Delhi and Himachal Pradesh, under the brand Airtel. By the year 2000, it became India’s largest private sector telecom operator post acquisitions of JT mobile and Skycell. It went public in the year 2001, after which it launched India’s first private sector national and international long distance service and by the year 2005, it became India’s largest integrated private operator with Pan India footprint in mobile services. After becoming the market leader in India, the company’s strategy shifted towards global expansion of its services. The expansion started with the launch of mobile services in Sri Lanka and Bangladesh. Bharti Airtel’s focus on global markets as its strategy for growth was very clear from Sunil Bharti Mittal, Chairman and Managing Director of the company’s message to the shareholders in the annual report of 2009, ‘After fifteen years of successful operation and an impressive presence across the South Asian region, Bharti Airtel is truly on the cusp of a huge transformation, and ready to move to the next level. As a conscious strategy, we have decided to focus on the emerging markets of Asia and Africa. We believe these markets will continue to be the growth engines of the telecom world. With its billion plus population, vast natural resources and a tele-density of less than 30%, I firmly believe, Africa is going to be a market for the future and the next growth engine of the global economy.’

The company’s strategy for the future was clear that it was looking for establishing its presence in Asia and Africa. It was looking for a possible alliance for this growth strategy.

MTN Group Limited, headquartered in South Africa, was launched in 1994 and soon became a multinational telecommunications group offering cellular network access and business solutions. It had mobile licences across 21 countries in Africa and the Middle East and as at the end of December 2009, had more than 116 million subscribers. The three main regions of business operations included South and East Africa (SEA), West and Central Africa (WECA) and Middle East and North Africa (MENA). In its 15 years of operations, MTN had established a truly global brand. MTN’s strategic agenda in the words of Group president and CEO, Mr. Phuthuma Nhleko in the 2009 annual report was, “it aims to be the leader in telecommunications in emerging markets. This strategy is built on three pillars – consolidation and diversification; leveraging MTN’s footprint and intellectual capacity; and convergence and operational evolution.”

MTN’s focus seemed to be to evolve operationally and become leader in emerging markets. It already was a leader in Africa. For Bharti Airtel, MTN would be a match made in heaven.

On May 25, 2009, the Indian daily newspaper Economic Times came out with the news about the possible acquisition by Bharti Airtel of MTN. It mentioned that Bharti Airtel was in talks with MTN to acquire 49% stake of the African company for an estimated $23 billion. In return, MTN would get a 36% economic interest in Bharti. This would lead to creation of a combined entity with presence in Africa and Asia. The combined entity would become one of the top five operators in the world. In a release to Bombay Stock Exchange (BSE), Bharti Airtel mentioned, “The broader strategic objective would be to achieve a full merger of MTN and Bharti as soon as it’s practicable to create a leading emerging telecom operator which today would have combined revenues of over $20 billion and a combined customer base of over 200 million customers.”

The synergistic benefits out of the deal were immense and both the companies’ looked forward to the deal for meeting their strategic objectives. They started their negotiations and deal structuring process with optimism and enthusiasm in 2009.

5.1.1. Failure of the deal

The two companies had negotiations twice in one year on the structuring of the deal. The deal needed approvals from regulators in both the countries. The firms had to face several challenges in India and Africa regarding decision on the deal terms. One of the challenges faced by the firms came in the form of complex FDI regime applicable to telecom sector in India. In anticipation of increased foreign investment, on 13 February, 2009, a lot of changes were made to the FDI norms. This led to the revision of definitions of company owned and controlled by Indians, calculation of direct investment, indirect investment, downstream investment etc. These changes were applicable from 2009 onwards when the Bharti-MTN deal was under negotiation. Another hurdle came in the form of amendment to the Securities and Exchange Board of India (SEBI) takeover rules which said that takeover rules on triggering an open offer would be applicable for entities acquiring global depositary receipts or American depositary receipts with voting rights in an Indian firm. Under this regulation, MTN would have needed to make a mandatory offer for another 20% of Bharti on top of the original 36%, pushing the foreign investment in Bharti over the 74% limit as there are other foreign investors on the Indian mobile operator’s share register. Hence, Bharti had to renegotiate the terms of the deal.

The final hurdle came in the form of approval from the South African government. South Africa’s Treasury, which is the authority to sign off cross-border transactions, raised objections that “the deal wouldn’t preserve the national character of MTN, one of the country’s largest wireless operators.” The South African government wanted the company to retain a South African identity after the deal and pressed for a structure called a “dual listing.” Securities and Exchange Board of India (SEBI) takeover rules which said that takeover rules on triggering an open offer would be applicable for entities acquiring global depositary receipts or American depositary receipts with voting rights in an Indian firm. Under this regulation, MTN would have needed to make a mandatory offer for another 20% of Bharti on top of the original 36%, pushing the foreign investment in Bharti over the 74% limit as there are other foreign investors on the Indian mobile operator’s share register. Hence, Bharti had to renegotiate the terms of the deal. “It would be sad if we saw this entity move into the hands and management of foreign nationals. Its management must remain South African,” South African Communications Minister Siphiwe Nyanda had told journalists. The proposed structure of dual listing is prohibited in Indian regulations.

With these hurdles, it was becoming very difficult for both the companies to seal the deal. Finally, the negotiations ended and Bharti Airtel withdrew the deal. If the deal would have been completed, this transaction would have been the single largest Foreign Direct Investment into South Africa and one of the largest outbound FDIs from India. The deal would have been a significant step in promoting South-South cooperation – a vision of the two countries.

5.1.2. Postscript

In 2010, Bharti Airtel could finally make its entry in the African markets by acquiring the African operations of Zain Telecom, Kuwait’s biggest mobile phone company for $10.7 billion. After this deal, Bharti Airtel became world’s fifth biggest cellphone company by subscribers. “We were fortunate that we got a second chance, and a better chance,” Sunil Mittal, chairman of Bharti Airtel, said.

A Bloomberg report suggested that MTN started exploring a potential acquisition in India, five years after it first tried to strike a deal with an Indian company. Reliance Communications was one of the potential targets but the deal did not come through. In 2013, the talks restarted and were halted again because of MTN’s skepticism about the industrial logic behind a deal at a time when India was revising its telecommunications mergers and acquisitions rules.

5.2. Case 2: ONGC Videsh Ltd. – Akpo Deal

ONGC Videsh Limited (OVL), a wholly owned subsidiary of Oil and Natural Gas Corporation Limited (ONGC), which is a Public Sector Enterprise/Undertaking of the Government of India, under the administrative control of the Ministry of Petroleum & Natural Gas (MoP&NG). OVL was incorporated as Hydrocarbons India Private Limited, on March 5, 1965 with registered office in New Delhi for the business of international exploration and production. The Company was rechristened as ONGC Videsh Limited w.e.f. 15th June, 1989. The primary business of the company is to prospect for oil and gas acreages abroad. These included acquisition of oil and gas fields in foreign countries as well as exploration, production, transportation and sale of oil and gas. In 2005, the chairman of the company, in his efforts to offset declining output from Indian fields, was looking for acquisition of reserves overseas. African fields which were rich in reserves, were potentially good investments and would help meet the rising energy demand. OVL was therefore identifying if any fields were available for acquisition in African subcontinent. The opportunity came in the form of AKPO field. AKPO was controlled by Nigerian firm South Atlantic Petroleum and its operations were managed by a French company called Total SA which held 24 precent stake in 2005. It had estimated reserves of 1.6 billion barrels of oil and oil equivalent gas reserves, which was 9% of Nigeria’s current production. The field was expected to yield 2,25,000 bpd beginning 2008. This made the field a very lucrative investment for oil companies across the globe. In early 2005, South Atlantic Petroleum had offered sale of stake in AKPO.

OVL planned to acquire 45 percent in AKPO and was willing to invest USD 2 billion in this acquisition for which central government clearance was awaited. OVL’s bid to acquire the block came close on the heels of its sister outfit ONGC Mittal Energy (OMEL) signing an MoU with the Nigerian government for operatorship of at least two blocks and assured supplies of 650,000 barrels of oil per day for 25 years. This could be a major victory for India if the deal goes through as Chinese oil companies had been lobbying hard to get a share in this field.

5.2.1. Failure of the Deal

The cabinet committee on economic affairs (CCEA) rejected ONGC’s USD 2 billion proposal to acquire the Akpo oilfield in Nigeria because of lack of clarity in ownership at South Atlantic Petroleum Ltd, the Nigerian firm that offered to sell a stake in the field. South Atlantic Petroleum was owned by former Nigerian Defence Minister Theophilus Danjuma and the CCEA felt dealing with him was ‘too risky.’ India’s decision to reject the investment plan ‘would appear to be on the grounds of high political risk given the government approved the purchase of some of Exxon Mobil‘s assets in Brazil,’ Peter Hitchens, an oil analyst at Teather & Greenwood in London, said in a report. ONGC was considered to be a serious competitor to the Chinese companies for oil and gas properties in the international market but with the Government shooting down a key proposal it lost considerable credibility in the market.

5.2.2. Postscript

After Indian government disallowed OVL to pursue the Akpo opportunity, China’s China National Offshore Oil Company Limited (CNOOC Ltd) acquired the 45 per cent stake for USD 2.268 billion. OVL undertook new acquisitions in the form of agreements signed for one project with Government of Sudan and another with Egyptian government. However, in 2011, OVL lost another bid to buy US energy major Exxon Mobil’s 25 per cent stake in a deep-sea oil block in Angola.

6. Conclusion

This study brings out interesting findings with respect to foreign direct investment in the form of cross border acquisitions for companies in both India and Africa. We find that out of the total outbound deals done by Indian companies; those in Africa are only 6% for the years 2002-2010. Indian stock markets are neutral about the deals. The potential that Africa has is still not evident from the stock returns. There are immense investment opportunities in Africa for Indian companies in the form of revenue potential and market access. Presently Indian investments have been targeted towards South Africa, Mauritius Egypt. There is a large untapped potential in other African nations such as Côte d’Ivoire, Ethiopia, Senegal and Sudan which we expect to see in the coming years.

After analyzing the two large withdrawn deals, we can identify a few challenges which come to the forefront for India-Africa foreign direct investments. Regulations with respect to FDI, mergers and acquisitions etc. need to be better aligned between the two countries which could encourage more value creating deals like Dunlop Africa Ltd with Apollo Tyres Ltd, Bharti Airtel with Zain Telecom and Trust Chemical Industries with Chemplast Sanmar Ltd. It requires firms to carry out due diligence with respect to the kind of partners they are looking for. The governments of both the countries need to work towards economic co-operation so that simpler methods could be employed in structuring any deal or agreement between companies of the two countries. From the case analysis of the two deals, Bharti Airtel-MTN and OVL-AKPO, we find that political concerns may acts as a hindrance in completion of deals. Political ties need to be strengthened between the two countries so that these act more as catalysts of growth. This has to be seen in terms of mutual cooperation between the two nations. Complexities in the procedures for flow of FDI also act as a challenge. Overall there has been a growth in investment by Indian firms into Africa. We believe that removal of regulatory hurdles could encourage further south-south cooperation which would be value enhancing to both Indian and African firms.