Status of the marketplace

Over the past couple of years, regulatory guidelines, requirements and processes that stemmed from the Dodd–Frank Wall Street Reform and Consumer Protection Act (Dodd-Frank) adversely impacted the banking mergers and acquisitions (M&A) market, and transaction activity fell.

As the understanding of regulatory guidelines has improved and banking institutions have matured their ability to respond, a new deal environment has begun to emerge, albeit with a tempered degree of enthusiasm.

This new deal environment will have vastly different strategic implications across the banking landscape based on the size of individual institutions. In addition, the level of involvement, focus and attention that divesting and acquiring institutions must devote to risk and regulatory matters is heightened and can make or break a deal. Additionally, the areas of focus of different regulatory bodies such as the Consumer Financial Protection Bureau, Office of the Comptroller of the Currency and Federal Reserve differ, but each has the ability to greatly impact the pace of deal progress. In turn, a much higher pre-approval bar exists that must be considered in advance to determine the areas where something could make a deal go awry. This inherently increases the complexity of approval and the overhead burden required to move the deal process forward.

Recognizing the emergence of this new banking deal paradigm, and the implications for individual institutions, will enable banks to better determine how acquisitions or divestitures should fit into their broader strategic plans. Furthermore, understanding the new normal around the involvement of risk/regulation in deal execution will require an adjusted approach to completing deals effectively.

Using the landscape to your advantage

Institutions that recognize and accept their specific placement in the new banking deal paradigm will have an improved ability to strategically maneuver and to be forward looking in how they prepare to execute on their capital/transaction strategies.

Fighting upstream against regulatory demands and staying on the sidelines are rapidly becoming losing strategies for several institutions that do not have a differentiated market position.

Three consistent themes that all institutions should consider as they pursue strategic alternatives are described below.

An institution’s ability to provide a sense of comfort and clear messaging across its applicable regulatory stakeholders and around how each of the items above is being addressed as part of the broader transaction will be highly correlated with deal approval and success.

Why size matters

The introduction of enhanced prudential standards (EPS) has created definitive thresholds among (1) financial institutions having greater than US$50b but less than US$250b in assets and (2) financial institutions having greater than US$250b in assets. These thresholds have created distinct and different implications for banks depending on their present asset size.

The implications around these defined EPS thresholds extend beyond the institutions that must meet the regulatory bar and have dramatically shifted the strategic landscape within which banks must continue to find ways to grow and/or optimize their deployed capital.

Over the course of the past year, we have seen institutions react in very different ways to this new environment, including: (1) a full exit of the US banking industry, (2) seeking to move non-core activities by product or geography and (3) initial movement in M&A as regulators have approved a few deals after a period of extended approvals.

The heightened regulatory requirements and oversight have forced banking institutions’ hand and pushed them toward an ever more apparent set of strategic paths.

The apparent strategic paths are defined by the equilibrium between shareholder return and regulatory compliance; this is the point where size matters.

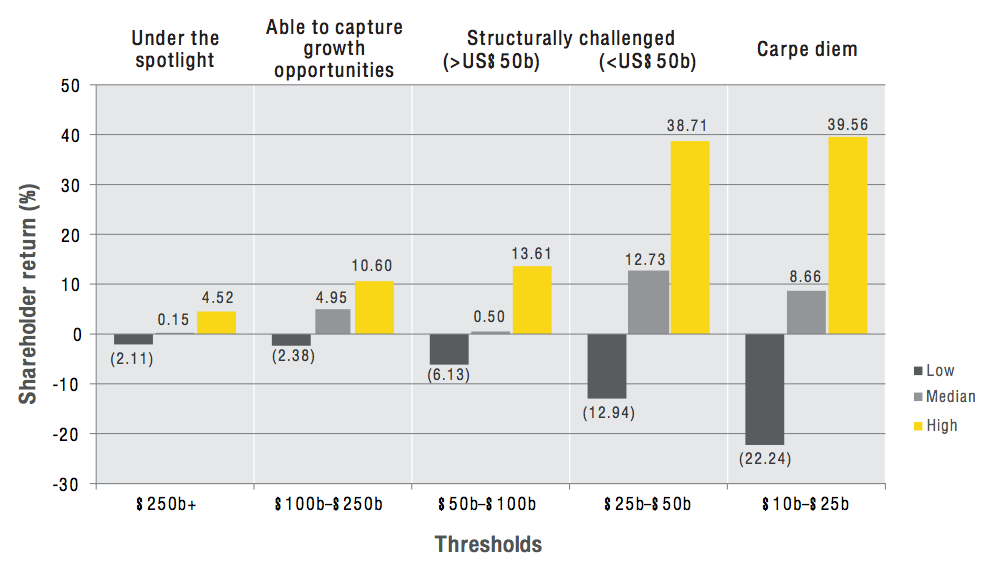

Shareholder returns by threshold

In the recent past, a review of shareholder return indicated size across the categories of banks outlined does matter. However, larger size does not directly correlate with improved shareholder returns.

Banks that are able to effectively balance regulatory considerations and develop differentiated strategies that drive growth, reward their shareholders while creating competitive separation from their peers.

Observations

• In the recent past, institutions above US$250b in assets have, on average, made a marginal return to shareholders that is not sustainable.

• Banks that fall below the critical US$250b threshold but above the US$50b mark show an ability to recapture their potential to generate shareholder return as they expand. The increase in shareholder return for institutions that grow well beyond the US$50b threshold is not only a reflection of scale and scope economies, but also indicates an increased knowledge and ability of management teams to run a highly complex institution.

• Contrarily, banks that fall within the “Structurally challenged” categories show a significant drop in the ability to return shareholder return on average as they grow beyond US$50b in assets.

• Banks that are less than US$50b in assets reflect the greatest ability to generate shareholder return on average; however, there is a great degree of deviation in the returns generated across individual banks.

• The deviation across smaller institutions not only reflects that the number of competitors is creating clear winners and losers in overlapping regional markets, but it also reflects that institutions that are able to clearly differentiate their business models are being rewarded, and shareholders reap the benefits.

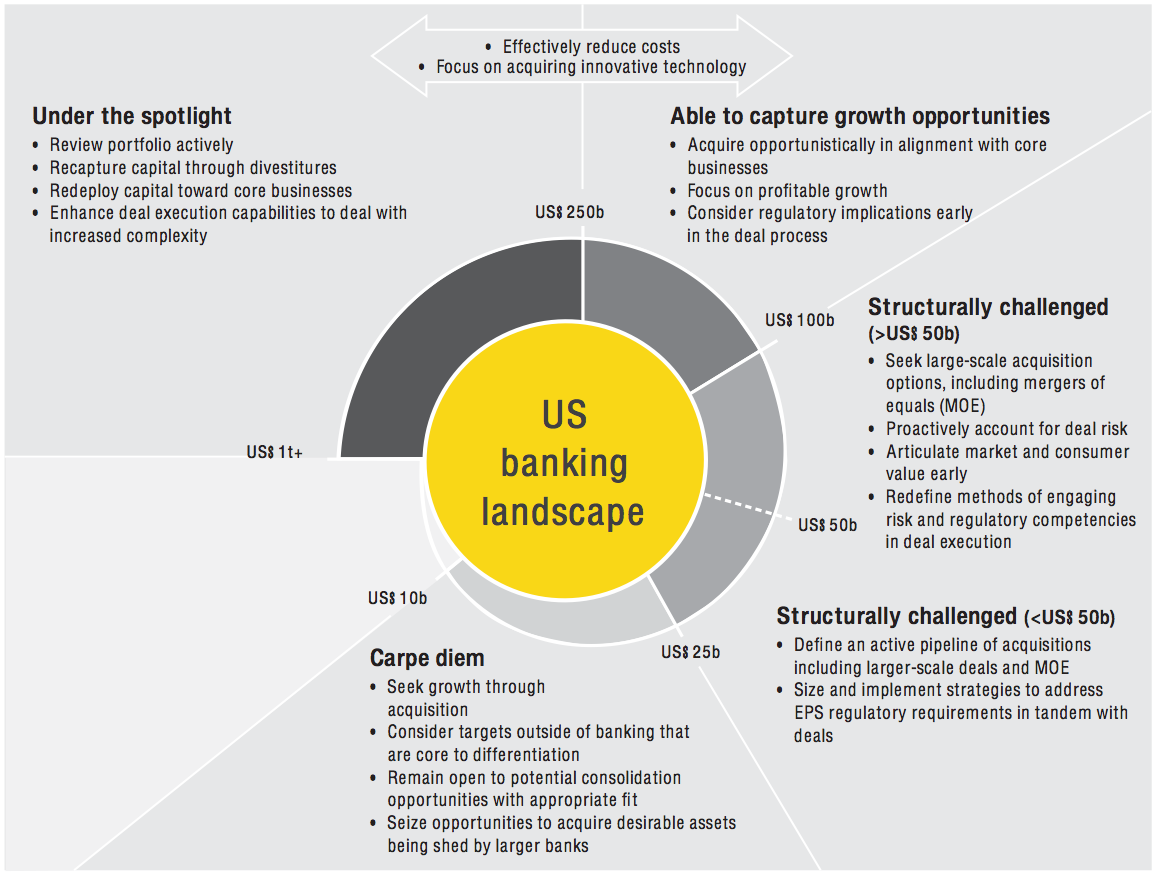

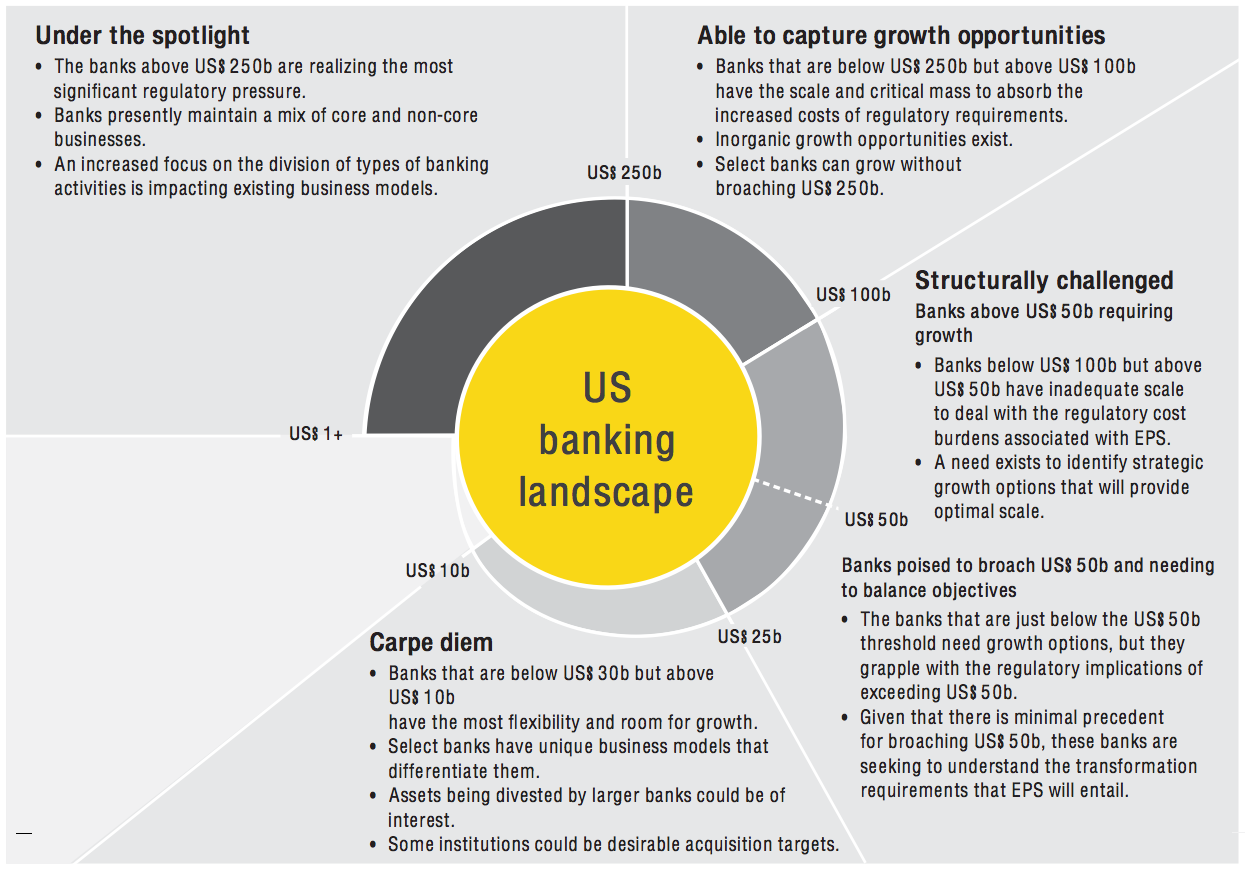

Under the spotlight

Banks with greater than US$250b in assets are confronted by regulatory and shareholder pressures that have forced them to reevaluate the value of businesses within their respective portfolios. The regulatory capital burden, or scrutiny associated with holding certain businesses, has made it challenging to achieve the necessary return on invested capital. In the present bank regulatory environment, this dynamic is unlikely to change, and the nation’s largest banks will continue to be strategically challenged.

As this environment perpetuates, sizeable divestitures will continue to be executed among the banks with balance sheet assets exceeding US$250b. Furthermore, wind-downs, which were once considered to be palatable only as a last-resort strategy for failing business, will be considered an optimal exit strategy when a market exit is the end goal.

In select instances where the divestitures or wind-downs are spanning multiple business lines or geographies, the previous deal execution capabilities of these mature and highly capable banking organizations will need to evolve. This will require new thinking so that the inherent complexities of these multi-faceted deal programs are well thought through and not handled as independent, one-off divestiture programs. Executing a suite of divestitures, which only in aggregate will result in the bank realizing its desired outcome, will create risks of lost value, cost overruns, unintended client impacts, and extended timelines to exit, all of which are highly undesirable.

Strategic impact

• These institutions will maintain active strategies focused on rigorous portfolio reviews, and capital optimization across businesses will be central to continually enhancing focus on the core.

• Development of effective approaches for harvesting and redeploying capital from divestitures will become a strategic advantage.

• Firms expecting large-scale transactions will need to upscale their operational execution competencies in order to deal with the complexities/challenges they will encounter.

• A laser focus on cost efficiency and rapidly acquiring or building advantages through innovative technology will also be a focus as new and disruptive competitors increasingly apply pressure on the business models of incumbent institutions.

Able to capture growth opportunities

Banks that fall just below the US$250b asset mark but exceed US$100b are in an optimal position among the largest banks within the current environment. These banks have achieved enough critical mass to not only weather the cost impacts of the EPS requirements for banks above the US$50b threshold, but they also have additional growth runway before they breach the US$250b threshold. This position offers these banks near-term opportunities, particularly as the banks with more than US$250b in assets shed desirable assets, and some banks in the range below US$25b are open to strategically aligned suitors.

Up until mid-2015, this group would have not been considered in an optimal position as regulatory reluctance to approve deals set the tone across the banking deal market. In the second half of 2015, several institutions within this size bracket have successfully received approval for deals, and that shift is beginning to open up new dialogues around how deals can get done effectively.

As a new but tempered optimism around closing deals has emerged, these institutions are going to continue to seek ways to acquire. Doing so will not be devoid of regulatory scrutiny from various directions; however, an institution’s ability to demonstrate its strategic rationale and focus on actively managing risk and regulatory challenges in tandem with acquisitions will allow for deals to progress. Although these banks may not be as focused on divestitures, there is a unique opportunity for a combined acquisition and divestiture approach to be utilized in order to continually refresh the portfolio while capturing aligned growth opportunities.

Strategic impact

• These institutions will be able to use a combined strategy of opportunistic inorganic growth combined with a strong core/non-core capability review that could generate sustained growth.

• As growth options are pursued, focus should be maintained on profitable growth options that maintain a balance between balance sheet expansion and achieved margin.

• Although the ability to get acquisitions done exists for these institutions, capitalizing on the availability of desirable assets will require an inclusion of regulatory considerations early and in tandem with deal strategy.

• Similar to the institutions above US$250b in assets, these banks will require a focus on cost efficiency and technology innovation.

• There is a unique opportunity for these institutions to also strive to differentiate their business models as well as increasing focus on select business lines and geographies.

Structurally challenged

Banks above US$50b requiring growth

Banks that are above US$50b but have not achieved the necessary scale or critical mass that would permit them to absorb the cost burdens that become inherent above the defined regulatory threshold for EPS are in a suboptimal strategic position. These banks have been held to regulatory standards that require internal reporting, infrastructure and programs that are identical to those required for an institution of up to US$250b in assets. The associated cost burden of these requirements for smaller institutions has a differential impact on their financials and operating structure, and in tandem they face inefficiencies of a ramp-up period when they first take on EPS efforts.

Adding further complication, size reduction is not an option, as moving down in asset size is not desirable from a management or shareholder perspective. In turn, these banks will need to grow organically or inorganically out of this suboptimal positioning. Pursuing inorganic options presents immediacy and speed that cannot be replicated through organic growth.

Similar to the banks that are able to harvest opportunities, those in the undesirable “Structurally challenged” category will need to become increasingly active in identifying acquisitions that are a strategic fit and will also need to focus on actively managing risk and regulatory challenges in tandem with acquisitions. Although divesting non-core is always an alternative, it is anticipated to be a lesser strategy in the near term for banks within this size range.

Strategic impact (>US$50b)

• This institution group will need to actively seek logical acquisition targets that fit well with their broader enterprise strategy and portfolio; however, adjacent deals will not be sufficient enough to drive the growth needed, and they will need to begin looking at mergers of equals and/or acquisitions of institutions in the range below US$50b.

• The articulation of the deal strategy will be very important for these institutions as they will have to make it evident to regulators why an acquisition is good for the market and account for the inherent risks as a central part of the deal execution.

• Recent successful acquisitions (approved by the regulators) have utilized an approach of placing a risk committee at the top of the overall integration (potentially an emerging best practice), or at a minimum have given risk groups a critical role in the steering committee.

Banks poised to broach US$50b and needing to balance objectives

Banks that are below US$50b in assets but above US$25b are not subject to EPS. However, their positioning in the market and need for growth will force them to act or be acted upon. Stagnancy will not be a viable option, and shareholders’ expectations will drive them to consider making acquisitions that would grow them toward and above US$50b. Alternatively, they will consider, or be influenced to consider, full-enterprise sales.

The banks that do brave the path of growing through acquisition in a manner that will place them at or above the US$50b threshold will continue to be pioneers in the near term. Thus far, only one institution has taken this on. Pursuing this strategic path will require institutions to take on and manage transformation initiatives aligned to areas of regulatory scrutiny and requirements in conjunction with managing integration activities. Placing equal weight on these two items is prudent and should be considered when a bank has a target acquisition that will require more than US$50b in assets in the pre-signing phase. Carefully planning deal milestones, such as the transaction close, in alignment with the effective date for EPS regulatory requirements can optimize time and allow for a more measured absorption of the changes that will be required.

The acquisition strategies of banks that are within this group will require a balance between immediate growth and forward strategy. As banks move above US$50b and shift from one area of “Structurally challenged” category to the next, they should already be thinking about (1) what steps and actions they will need to take to leapfrog the inherent learning curve of being subject to EPS for the first time; (2) building a sound platform that can allow for further growth and stand up to regulatory expectation and (3) the next acquisition that will allow them to achieve necessary scale.

Strategic impact (<US$50b)

• As these institutions consider acquisitions they should evaluate a longer-term pipeline of deals that could move them fully out of the “Structurally challenged” category.

• Considering a transaction will require additional and simultaneous evolution of EPS requirements and the related implications; i.e., institutions will need to begin considering broader platform impacts of breaching US$50b, and it will be a necessity to begin building a future operating model at a much quicker pace than in typical acquisition scenarios.

• The overall deal strategy will have to incorporate the impact of regulatory timelines and expectations as well as a focused regulatory communication strategy.

• Strategically and protectively involving risk and regulatory groups in the deal oversight and the development of regulatory programs that align with deal strategies is becoming a differentiating capability.

Carpe diem

Banks that are less than US$25b in assets but greater than US$10b in assets maintain the greatest flexibility and prospects in the new deal environment. The challenges and hurdles faced across other banks larger in size across the sector will open up growth deal opportunities for these firms. Additionally, these banks have no concern about breaching critical regulatory thresholds in the near term.

As a result, growth prospects are more bountiful for these banks in a way that they weren’t in the periods prior to Dodd-Frank. Larger institutions are now held to a very high standard of proof that an acquisition is beneficial before they proceed with a deal, and that prevents larger institutions from acting as quickly as they might have in the past on deals that become available.

Additionally, as larger institutions shed assets through divestitures, this group of banks will have an ability to move quickly to capture deals that are aligned to their overall strategies. Alternatively, they will have the ability to double down on adjacent acquisitions that are aligned with their core businesses. Furthermore, this group of banks continues to be ripe for consolidation and will also be attractive to institutions that are in the “Structurally challenged” and “Able to capture growth opportunities” categories.

These banks will begin to realize increased deal flow internally and externally. Depending on the individual bank’s strategy, there are many strategic paths that can be pursued, so one of the greatest challenges will be staying true to defined strategic vision and not getting distracted by available assets that are off-strategy but potentially near-term accretive.

Strategic impact

• These institutions will have the greatest latitude in their strategic growth options, and they should be opportunistic and relatively aggressive in seeking growth.

• A successful portfolio growth strategy and composition will manage short-term growth objectives with a long-term vision that accounts for the challenges and hurdles the bank will face as it grows.

• Select institutions in this size range presently have unique and differentiated value propositions that they can continue to build on through organic growth or through adjacent acquisitions outside of the traditional banking realm that remain tightly aligned to their core business strategy.

• Mergers of equals and consolidations may also be an optimal way for some banks in this group to expand their market footprint; and there is the potential for the long-awaited mid-market consolidations to occur among this class of banks.

• This group will also have the opportunity to benefit from assets that the larger institutions (>US$250b) begin to shed; the challenge in acquiring assets being divested by the larger banks will be making certain that the strategic fit and alignment with the bank’s broader business portfolio exist and that opportunistic transactions don’t lead toward a heterogeneous portfolio of misaligned businesses.

Beneficiaries

“Shadow banking” — broad lending activities outside the banking system

• The new deal environment has strengthened and deepened the presence and involvement of shadow banking institutions in lending activities (e.g., unsecured lending, business loans, student loans, mortgages).

• Shadow banking institutions presently have greater flexibility to act on assets that may come available given they are not subject to the regulatory requirements banks face.

• Additionally, their business models allow them to act faster and take more risks than traditional and mature banking organizations.

• Shadow banks should remain aggressiveness in acquiring target assets out of banking institutions while carefully assessing the balance sheet composition they form.

• The lack of regulation in this space is not likely to remain forever, especially as the segment grows; but in the near term, it remains a very beneficial position to be in and is likely to see continued inorganic growth prospects.

What strategies will define your bank?

There is no “one size fits all” strategy or set of strategic actions that will work across institutions of a specific size. However, each bank’s ability to create the appropriate balance and composition of strategies going forward will define its ability to not only survive but also to build a differentiated and sustainable business model that can weather the challenges posed by an environment that is disrupting business models that haven’t changed dramatically in the last century.