By Christian Niegel – Arthur D. Little

Contributor: Joan Tapia Boil

Europe is experiencing an unparalleled wave of telecom mergers, but value creation is far from certain. Executives charged with telecom integration are facing pressure to meet expectations on synergies, which increasingly are expected to amount to over half of the purchase price. This Arthur D. Little viewpoint provides lessons learned, benchmarks and recommendations to help telecom executives successfully create value through the post-merger integration process.

Europe’s wave of telecom mergers is being driven by a double cash-flow squeeze, global Internet competition, record low interest rates and regulatory approvals

Europe is experiencing a record wave of telecom merger activity that may well be the beginning of a consolidation of the EU28 telecom market, which currently encompasses more than 200 operators and 40 groups.

Operators are experiencing a double cash-flow squeeze. On one hand, revenues continue to decline due to consumer-focused regulation and increasing competition from global Internet players, such as Google and WhatsApp, offering alternative services via OTT. At the same time, operators are investing record sums into their broadband networks to meet the exploding demand for data traffic. Telecom mergers are hence the logical next step to maintain profitability levels.

The approval of Telefonica Germany’s acquisition of E-Plus, the largest four-to-three market player merger ever in EU28, has been a catalyst for other telecom merger talks. Many consider this as a paradigm shift of European telecom regulation, away from a focus on affordable prices for consumers and toward enabling telecom operators to generate sufficient profits to bear record high investments. Record low interest rates have also made it easier to finance acquisitions.

Globally active telecom investors are eager to benefit from opportunities in the consolidation of the European telecom market. Examples include Mexican América Móvil’s acquisition of Telekom Austria or Russian Vimpelcom’s investment in Wind in Italy. Private Equity firms are also active, owning Sunrise and Orange in Switzerland, and acting as serious bidders for Telekom Slovenije, among others.

The telecom merger wave and the underlying logic of converging industry segments has resulted in an “everybody talks to everybody” situation, whether incumbent, mobile operator or PayTV satellite operator. Europe already experienced four mobile-mobile mergers and we are likely to see more. The challenge now is to maximize the value created from these mergers.

Synergy expectations account for more than 50 percent of the purchase price

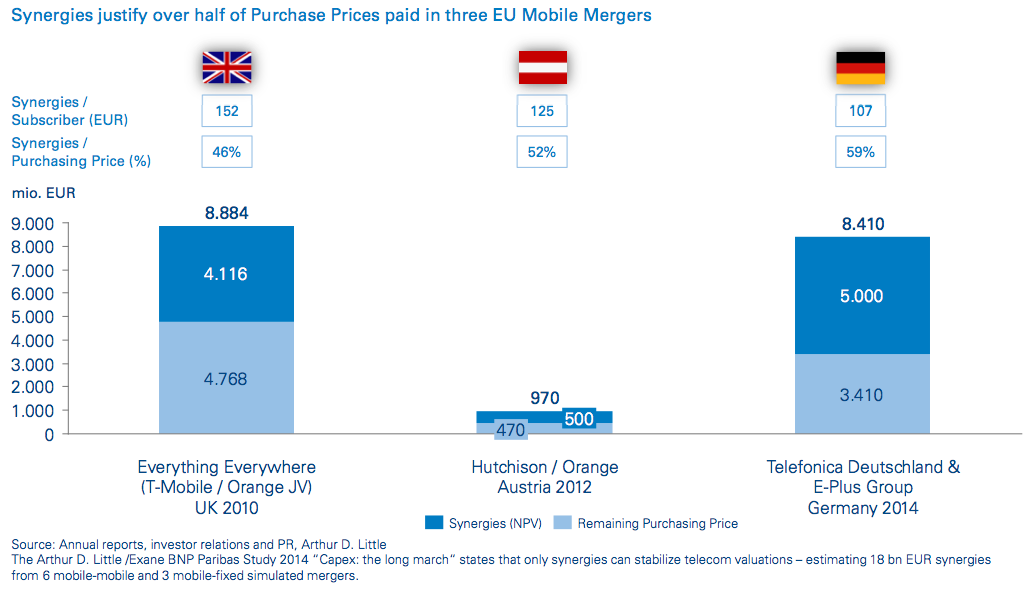

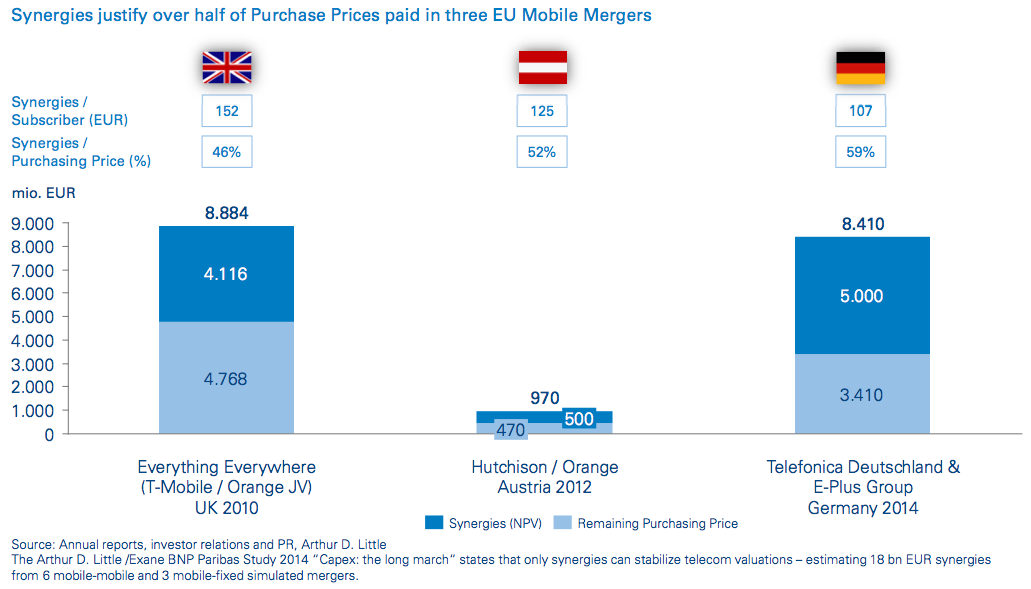

Market expectations typically require buyers to pay 20-30 percent premium over pre-announcement market capitalizations, and even more if there are several potential buyers. To create value, executives in the new entity need to realize synergies with a net present value well above the 20-30 percent. In fact, the mobile-mobile mergers of Everything Everywhere in 2010 and Telefonica Germany / E-Plus in 2014 indicate that the expected synergies from these mergers amounted to 46 percent and 59 percent, respectively. These transactions show that there is an increasing expectation that over half of the purchase price can be earned via rapid achievement of synergies!

Achieving these synergies is a very complex process of merging two disparate operators and their market positions, brand portfolios, distribution channels, employees, networks and IT-systems. To quote one executive, “this is like performing open heart surgery while being watched by numerous parties”.

Market communication, a year-long plan and decisive actions on the key synergy areas are key

The days of classic “100-day plans” for post-merger integration are long over. Management needs to take decisive action to establish a new leadership team, set cornerstones and communicate clear plans for integration work. “Low hanging fruit” can be rapidly achieved, but also provide low synergy value. Major items, such as network/IT integration, marketing and distribution take much longer. While rebranding can now often be achieved in under one year, sales channel integration takes rather two and network integration three years or longer in our experience.

Clear communication is critical to this integration marathon. Customers, staff, shareholders and lenders do not usually buy into initial synergy announcements; their trust rather needs to be won by regular communication of integration successes. At times it may even be wise to delay synergy creation measures to win this trust, as expressed by one CEO’s comment: “If I had another transaction, I would focus more on ensuring network quality and excellent customer experience and delay the realization of synergies.”

Post-merger integration executives need to focus on three major items and their challenges:

■ Network & IT integration: Network and IT Opex and Capex account for about 50 percent of synergy plans. Merging two legacy and packaged switched networks into one integrated network is a complex process. Customers expect stable and consistent service throughout the integration, as well as rapid coverage and capacity improvements. Shareholders also expect rapid and significant savings by decommissioning excess mobile base stations, but network integration can take 3 years or more.

■ Marketing, Distribution and Customer Care: These areas account for about 28 percent of synergy plans. But these customer-facing areas need to be integrated with due care, as customers expect improvements in integrated customer care and sales, and get easily irritated if they sense that changes are to their disadvantage. A good solution is to temporarily increase sales and customer care capacity to handle peaks of customer questions.

■ Marketing, Distribution and Customer Care: These areas account for about 28 percent of synergy plans. But these customer-facing areas need to be integrated with due care, as customers expect improvements in integrated customer care and sales, and get easily irritated if they sense that changes are to their disadvantage. A good solution is to temporarily increase sales and customer care capacity to handle peaks of customer questions.

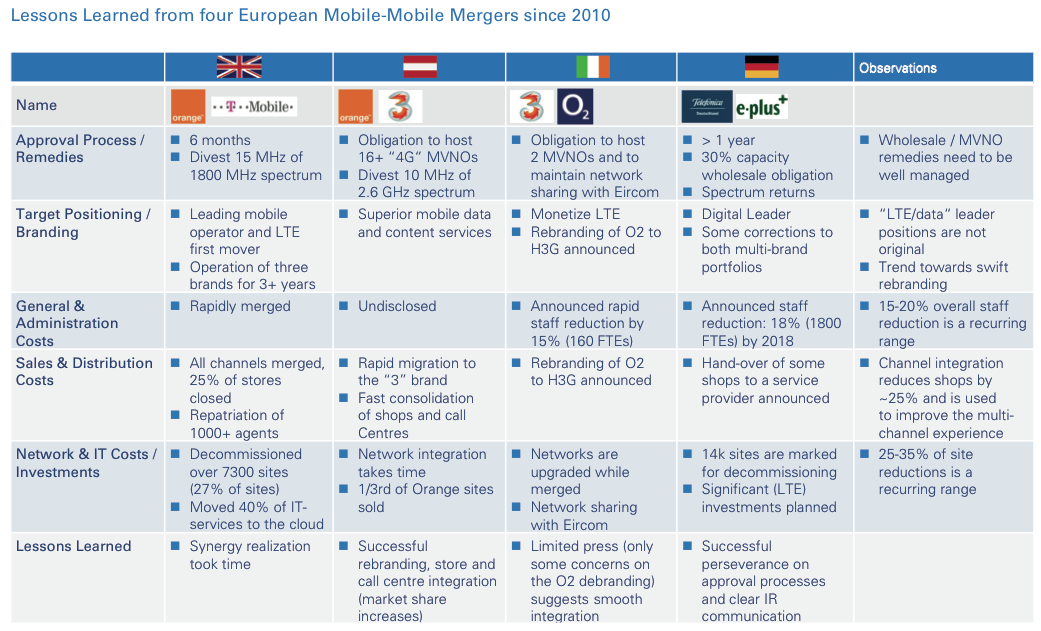

A close look at the four mobile-mobile mergers in the EU since 2010 (illustrated above) provides key lessons and benchmark ranges for synergy creation potential.

Mobile-mobile mergers provide lessons and benchmarks for post-merger integration and synergy realization

Based on recent mobile-mobile mergers, other telecom transactions and our numerous transaction and transformation projects, Arthur D. Little provides seven lessons learned and benchmarks for telecom post-merger integrations:

1. Managing approval processes and remedies professionally in a partnership mode with the national and EU anti-trust and regulatory authorities is best practice

2. Mergers should follow a clear strategy for the long run, a 2-3 year integration phase after the classic “100 days” and merger honeymoon. Customers need to know what shall be the new customer promise. All four newly merged mobile operators cited in our examples aspire to be an “LTE/Digital” leader, which is hardly a differentiator

3. Clear market and investor communication cannot be overdone. People know that realizing synergy plans is tricky, but expect clear communication and swift corrective actions, if necessary

4. Rebranding / brand portfolio changes should be completed rapidly rather than destabilizing customers through brand uncertainty

5. Staff reductions are typically in the range of 15-20 percent, often starting with administrative functions, followed by shop and call centre agents and, lastly, by network teams. For all functions, it may be prudent to initially reserve higher capacity to cover customer requests and the additional integration workload

6. Points of sale are not reduced by half – but rather by 25-30 percent. The effective sales presence of merged mobile operator actually increases with the launch of flagship stores and integrated offline and online sales processes

7. Network integration does not lead to cutting site numbers by half but rather by 25-35 percent as the newly merged mobile operators want to offer improved coverage and data capacity to the combined customer bases. We may see lower site reduction ratios as mobile networks become more dense also due to the installation of micro- and pico-cells (5G) across the world.

The current wave of telecom mergers will continue in Europe. The consolidation of the European telecom market has begun and pressure is on to maximize the value created for all stakeholders. Arthur D. Little hopes that the recommendations and benchmarks included in this Viewpoint will help all stakeholders achieve this goal.