By Mike Ostergard, Austin Corbett – Accenture

US hospitals have been consolidating with enthusiasm. Despite some pullback in 2014, deal volumes grew by 9 percent between 2010 and 2013.

Bigger, however, does not automatically equate to better.

Accenture research reveals that the synergies achieved from many of these deals have been disappointing. In fact, the average acquiring provider left nearly $25 million per target on the table in 2015: potential cost and revenue synergies that could have been invested in improving access and the total cost of care.

As health systems evolve, cost efficiencies become even more critical. But it’s not too late to achieve the full potential operational synergies of effective integration—even for acquisitions that closed some time ago. Our research shows that by relentlessly addressing key M&A value drivers, hospitals could boost margins by as much as 23 percent per target.

First, however, they need to recognize just why they may have been losing out.

Deal-making distractions

Capturing synergies through effective post-merger integration has not always been the highest priority for acquiring health systems.

Many (and especially the biggest) have tended to focus on scale, reach, and healthcare service mix, rather than on cost and efficiency. What’s more, they tend to be mission-driven rather than profit-driven, and are frequently saddled with static, multi-board governance structures. With too many fires to put out in existing operations, their preference has been to let the organizational and operational challenges of post-merger integration work themselves out—especially where local market sensitivities are an issue, or if they fear disrupting clinical performance.

In an increasingly complex healthcare environment, characterized by constant pressure on rates and shifting financial risk, that approach simply hasn’t worked. Patients are driving more and more of their own decisions and demanding a better experience at every level. In addition, regulations like the Affordable Care Act, which requires hospitals to deliver better healthcare, at lower cost, to more patients, are squeezing operating costs.

But although the need to be synergy-focused should be intensifying, even some of the biggest recent deals have struggled to deliver financially, post deal close. In fact, they’ve lost value (see Losing value).

Patients are driving more and more of their own decisions and demanding a better experience at every level. In addition, regulations like the Affordable Care Act, which requires hospitals to deliver better healthcare, at lower cost, to more patients, are squeezing operating costs.

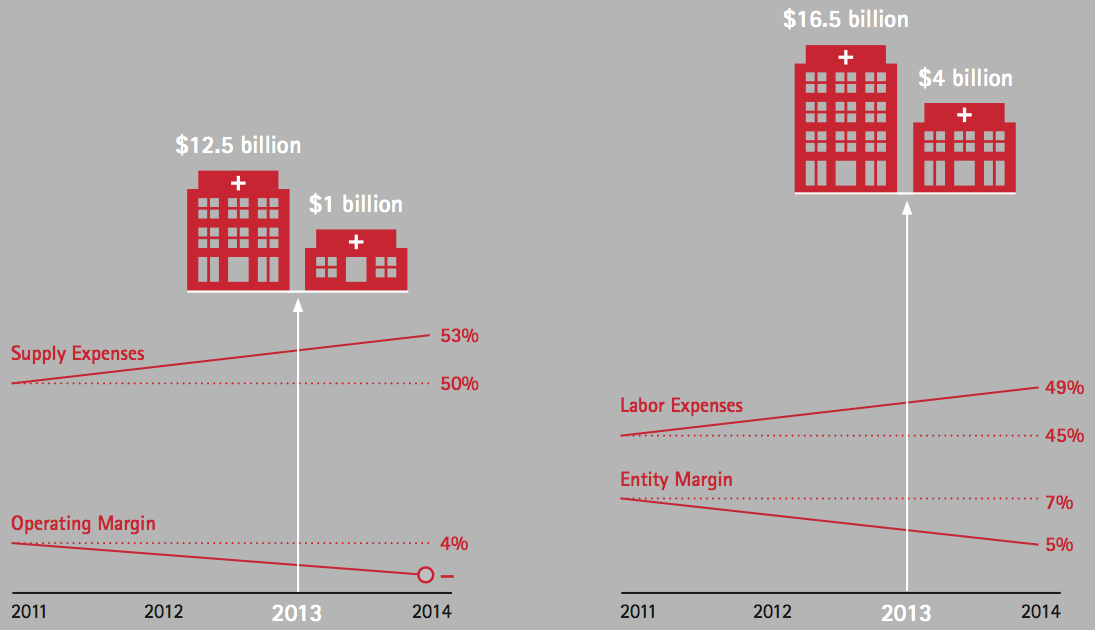

Losing value

In one transaction, completed in 2013, a $12.5 billion health system acquired another valued at more than $1 billion. Yet between 2011 and 2014, the combined organization’s operating margin declined from 4 percent to break-even, while supply expenses rose by 50 percent to 53 percent. In another 2013 deal, a $16.5 billion health system acquired a health system worth more than $4 billion; but between 2011 and 2014, the combined entity’s margins declined from 7 percent to 5 percent, while its labor expenses rose from 45 percent to 49 percent.

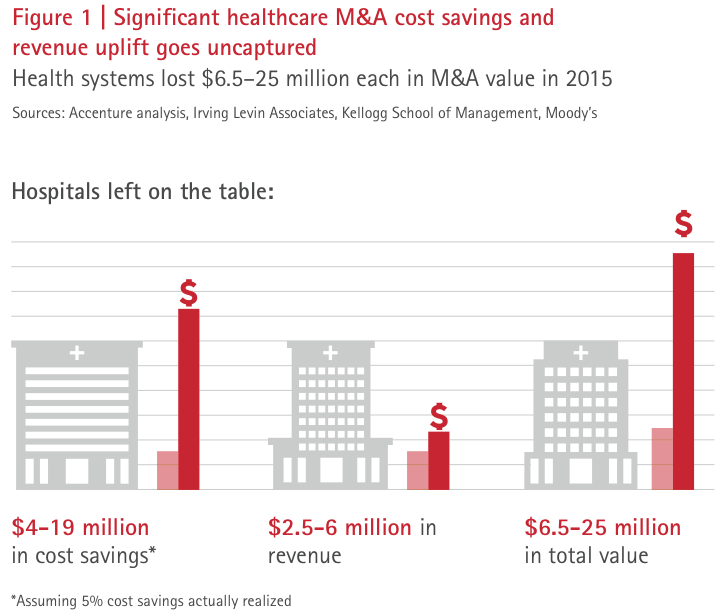

And health system M&A activity has been falling well short of maximum value potential for some years. In transactions completed between 2000 and 2010, US provider acquirers managed to deliver cost synergies of only 3 to 5 percent. Accenture analysis suggests that, overall, acquiring health systems may be missing out on $4-$19 million in annual cost savings per hospital and losing revenue uplift of $2.5-$6 million per hospital per year (see Figure 1).

Leakage on that scale—magnified for the biggest acquirers—is plainly untenable in today’s market. Health systems must intensify their focus on synergies, and move with purpose to capture more of them.

Steps to success

To achieve the latent benefits of M&A, acquiring hospitals need to do three key things:

- Prioritize the value drivers that will enable improved performance and profitability

- Reconfigure the combined health system’s operating model (organization, processes, systems and assets) so that it fully supports efficient and effective care delivery

- Develop a post-close integration plan that prioritizes value capture and supports the new operating model while managing risk

For larger systems, five areas of value, impacting both costs and revenues, are especially critical (see Figure 2.)

These value drivers can deliver returns in excess of what was once considered typical within two years of deal close. Indeed, health systems that apply a disciplined focus to systematic synergy capture may be able to achieve cost savings of between 9 and 23 percent of the acquisition target’s cost base. That’s no small consideration for hospitals struggling to adapt as healthcare moves from a fee-for-service to a fee-for-value model. The time to start implementing a far more rigorous approach to integration and value capture—both during acquisition and after—is now.